Singapore-based Sea Limited, which runs Garena, Shopee and AirPay, is one of the biggest tech investment stories of 2020. In the first quarter of 2020, the company was trading in the $40 price range. It is now around $180, with a market capitalization approaching $100B. It has been a rocketship for investors this year.

But Sea’s rise has actually been going on for a while. Just one year prior (January 2019), the stock was around $15. And it rose to $45 by late 2019. There was already a strong price increase – before the massive surge in mid-2020.

What we are seeing is the result of some really good strategy that was put in place starting in 2015. You could see the leading indicators of this strategy working back in 2017-2018. And then, finally, the financials (usually lagging indicators) started to move. The spectacular rise of Sea Ltd. is about great strategy, which is the point of this class.

So I went back to look at the 10-K from 2018, to see what was visible. What should we have noticed prior to the big share price increase?

And I think 4 big strategy lessons jump out.

Lesson 1: Sea built an outstanding innovation / audience-builder platform for localized, immersive gaming.

Sea is a platform company. Like Alibaba, everything they do is a platform building model. And they are really good at it. What comes across in their annual reports is how thoughtful and subtle they are at platform strategy. The crispness of their language and thinking jumped out at me the first time I read it. I can spot top tier digital strategy thinking a mile away. This set off my radar almost immediately.

Their gaming platform is Garena, which is an innovation & audience-builder platform (one of my five platform types). So it is a platform with three user groups – consumers, advertisers / merchants and game developers. On the innovation aspect, it connects consumers with video game developers. So it’s not unlike the App store in that regard.

But most of the action is on the consumer and advertiser sides (i.e., the audience-builder). Video games command tremendous consumer engagement. They spend ridiculous amounts of time playing. They can be really passionate and loyal to their games. Note: China was the first country to classify gaming as an addiction.

Additionally, there are tons of interactions between players. There are multiplayer modes like battle royale and World of Warcraft. There are social communications. There is content sharing. There are leagues and competitions (both online and in person). There are live streamers. There are even fan communities and armies of content creators who make videos about news and how to play various games. It’s hard to find a product with higher levels of consumer engagement than multiplayer and social gaming. So player-to-player interactions are important on the platform.

And all of this engagement also creates opportunities for advertisers and brands, who do everything from in-game signage to branded skins. It’s getting harder to see much difference between billboards and ads in the real and virtual worlds.

Overall, multiplayer gaming is a powerful platform business model. And it has long been Tencent’s core economic and engagement engine.

If there is a downside, it is on the developer side. There are only a few popular games. So a small number of game developers have a lot of power in this business. Everyone is pretty much dependent on what companies like Riot and Epic Games do. In its 2018 10K, Garena mentions that 5 games generated 80% of their gaming revenue.

***

Ok. All of the above is basic theory about gaming platforms. But within this, Garena has three impressive aspects to its strategy:

- They are focused on “immersive games”.

I loved this part of the annual report. Management clearly argues that multiplayer, immersive gaming is their focus. Specifically, they are focused on in-depth games that are battle royale, multiplayer online battle arena, massive multiplayer online action games (MMOAG), massive multiplayer online role playing game (MMORPG) and esports. And they are not doing casual gaming.

If you are in the platform business, that is exactly the right approach for gaming. Players in “immersive games” and in multiplayer play more frequently. They play longer. They spend more. While casual gaming might get you more users, immersive and multiplayer gaming means greater engagement and data. It means more interactions between players. It means greater ability to monetize via advertising, gifting, and digital goods. It is a more robust platform.

- They are focused on localizing country-by-country in SE Asia.

Localizing the gaming experience country-by-country in SE Asia is one of Garena’s strengths as a distributor. Garena operates across Taiwan, Indonesia, Philippines, Thailand, Vietnam, Singapore and Malaysia. So they need to adapt the games, languages, content and advertising country-by-country. This makes the experience better for players. It taps into local advertisers. It requires meeting local regulations (which can be significant). It also means getting the payment and hosting set up. In the earlier days of Garena, they had to do a lot of work with local gaming cafes, as people didn’t have PCs and smartphones.

This is all good from a consumer perspective. But it also strengthens the company’s position relative to the large, international game developers who don’t want to deal with this stuff in every country. Epic Games doesn’t want to figure out marketing, payment and regulations in Malaysia vs. Vietnam. Game developers have a lot of power in controlling the titles globally. But Garena has a lot of power in localization and capturing local consumers.

This puts them in a much better position than video game distributors in the US, where there is a common market, language and regulations.

- Tencent is their partner.

Plus, Tencent is a major shareholder. And let’s not underestimate how much this strengthens the company’s position relative to game developers. Tencent is the mothership of gaming. It is like the Hollywood of gaming.

So having a strategic partnership, and major ownership by, Tencent is another massive strength for the company.

***

Overall, their platform strategy for gaming in SE Asia is outstanding. And this is what they have been building since 2009.

Lesson 2: Sea successfully launched a marketplace platform for SE Asia ecommerce.

In 2015, Sea launched an ecommerce marketplace. Think of what a big strategic move that was. To jump from gaming, a mostly digital business, into the real world business of selling physical products was a big move. It meant getting into logistics, inventory and trying to sell and deliver goods across +6 different countries, most of which happen to have tons of islands. It was a major strategic move.

And it was super smart.

Because not all platform business models are equal. Some are really difficult (i.e., Uber). Some are ok (i.e., food delivery). Some are profitable but limited (i.e., hotel bookings). And a rare few can really create long-term dominance, tons of cash flow and a strategic position for future growth. This select list of truly great platforms includes messenger, payment platforms, gaming and ecommerce marketplaces. Sea targeted an ecommerce marketplace, arguably the best platform opportunity. They chose to go after the same opportunity that created Alibaba in China and Amazon in the USA.

Sea launched with a Taobao-type C2C marketplace in 2015. So lots of small merchants selling to lots of consumers. A Tmall B2C type marketplace followed in 2017, focusing on larger brands. And they really spent heavily. It hurt their overall gross profits. It wiped out their overall operating profits. It was a major risk and they spent heavily.

In 2015:

- Gaming revenue: $282M

- Ecommerce revenue: $10M

- Cost of revenue: $184M (63% of total revenue)

- Sales & marketing expense: $89M (30% of total revenue)

In 2017:

- Gaming revenue: $365M

- Ecommerce revenue: $49M

- Cost of revenue: $327M (79% of total revenue)

- Sales & marketing expense: $426M (103% of total revenue)

The 2015 numbers show the picture prior to ecommerce. A nice profitable gaming platform with solid growth (10-20%).

Then look at how much the sales & marketing expense skyrocketed. The management really opened up the cash spigots. They cratered their profitability – and revenue only grew about 41% total during this two year period. This was the period when a good understanding of digital strategy should have set off your alarm.

Because in 2018 and 2019, the platform really started to move. Their ecommerce revenue really started to grow.

- Total revenue in 2017: $414M

- Total revenue in 2018: $827M

- Total revenue in 2019: $2,175M

By 2018, it was clear their big strategic move in ecommerce was going to work.

Note 1: Their strategy for ecommerce was pretty standard. They began by building basic marketplace platforms with C2C and B2C. They did lots of spending on marketing. They started building a lot of logistics across a big, difficult geography. This is really phase 1 of SE Asia ecommerce.

Note 2: One of things I really like about both gaming and marketplace platforms is their negative working capital. It’s just a nice aspect of the business. In both, consumers pay first. And the company later pays the merchants and advertisers. So you get negative working capital, which makes growth cheaper.

Note 3: Marketplaces, unlike gaming, don’t have powerful game developers. Most merchants selling on marketplaces are quite small (with little leverage). And while the logistics are very expensive to build, this later becomes a great moat against competitors. It is quite difficult to catch up with an established marketplace with tons of built out logistics. You either need big spending by venture backers (which Jet did to take on Amazon) or you need another business that generates cash flow and a big backer (Sea has both).

Lesson 3: Sea is going for a complementary platform strategy, which is a “Winner Take All” scenario.

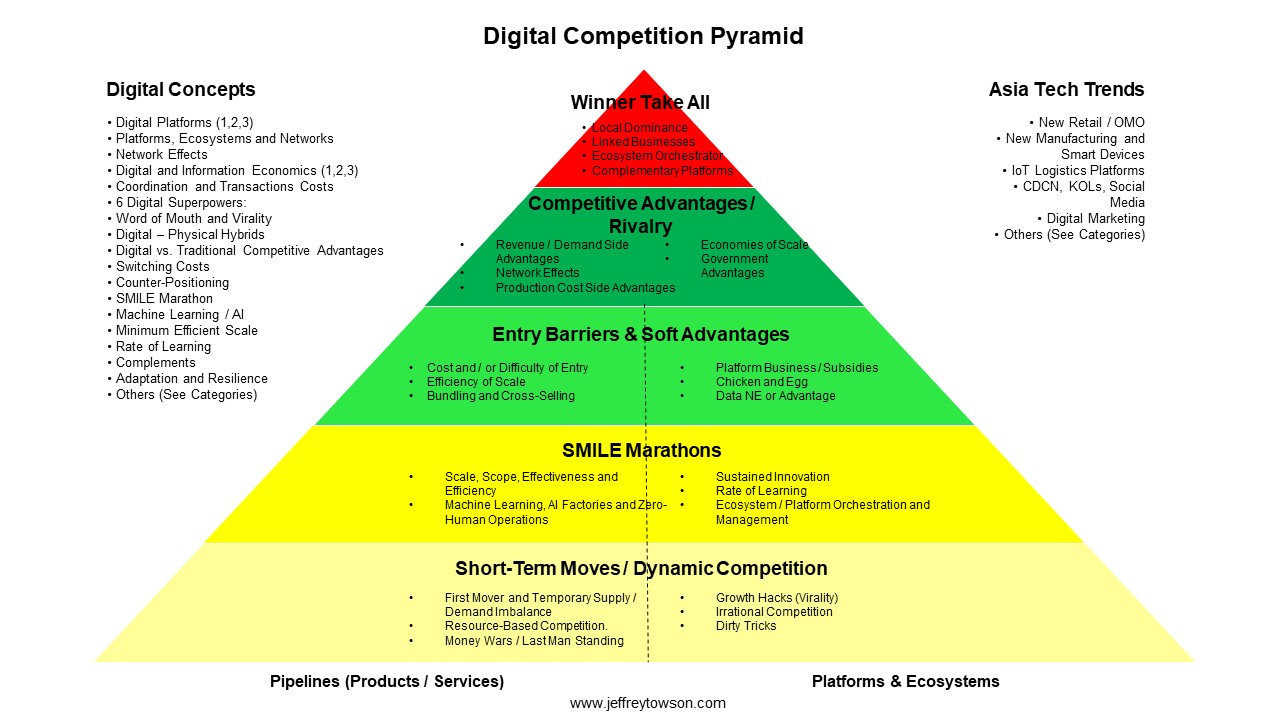

At the top of my digital strategy pyramid, I have placed “Winner Take All“.

The bottom of the pyramid is difficult. And you need a SMILE marathon as a competitive dimension. The goal, if possible, is to build competitive advantages that make you hard to compete with (the green level). You want to move up the pyramid.

But there is a level at the top where virtually nobody can do what you do. This is winner take all. This is Alibaba, Tencent, Amazon, Google and Apple. I have detailed four types of Winner Take All scenarios:

- Local dominance

- Linked businesses

- Ecosystem orchestrator

- Complementary platforms

My argument for why these scenarios are so hard to compete with is similar to my argument for product bundles, like Microsoft Office. It is one thing to be a word processor product and to compete against Microsoft Word. But once they bundled Word, Powerpoint and Excel into Office, these companies had to create all three products just to compete. That bundling by Microsoft had great economics. And it also eliminated most of the competition.

It is the same for complementary platforms and linked businesses. These can eliminate most competitors because they would need to replicate not just one, but multiple businesses to compete. That’s why it tends to be a winner-take-all scenario.

It looks to me like Sea is getting close to having 2-3 complementary platforms. They are going for the top of the pyramid. That is fantastic.

Plus there are other benefits for having complementary platforms and linked businesses. First, it can dramatically reduce customer acquisition costs. It means the platforms can share financial and IT resources. They bundle various services. They can subsidize different user groups. They can share data. And they are well positioned for new initiatives and horizontal attacks into other businesses (Alibaba does this like every month).

Basically, Sea is steadily moving to the top of my digital strategy pyramid.

Lesson 4: Sea has great management with a “capacity to suffer”.

My first three lessons are strategy. They are about structure and business models. But you need both great management and great strategy. If the business model is the horse, management is the jockey.

All indications are that Sea has top tier management. As I said in Podcast 40, Lazada definitely has structural advantages in logistics. But Sea appears to have better management.

When it comes to Sea’s management, there are four things that really jump out at me:

- They nailed the timing and execution of their jump into ecommerce. If they had tried to enter SE Asia ecommerce in 2009, it would have been very slow, difficult and expensive. If they had waited until 2020, it would have been too late to take on Lazada (probably). They got the timing right. And they pulled it off. The numbers are in and they are executing well.

- They are now on their their platform business model. They did Garena, Shopee and now AirPay. We have a good track record to look at.

- Along the way, they also launched Free Fire. In a surprising move, they became a game developer (sort of) and launched of the top games in SE Asia. That is impressive.

- They have what Thomas Russo calls the “capacity to suffer” (more on this below).

Tom Russo (Gardner, Russo & Gardner) is a famous US value investor with a Warren Buffett-type strategy. But he focuses mostly on food and beverage – and mostly in developing economies. He typically buys highly branded European and American family-owned CPG companies (like Swatch and Diageo) that have ownership and governance in the West but capture their value in developing economies. This is not unlike buying a Singapore-based company that makes it’s money in less developed environments around Asia.

The challenge (and opportunity) of this investment strategy is building in developing economies often means steep upfront costs for later returns. You have to invest in developing economies for years to build out distribution and operations before the revenue happens. This means taking near-term losses for long-term gains, which many big company management teams avoid.

But Russo talks a lot about how he looks for is management with a “capacity to suffer”. Management (and investors) who can take operating losses now for bigger profits later. It’s about delayed gratification, another big Warren Buffett idea. As he says:

“Someone’s sitting in the shade today because someone planted a tree a long time ago.” – Warren Buffett

This type of “capacity to suffer” means management is behaving like long-term thinkers and like owners.

And this is exactly what we see in Sea’s numbers in 2016-2018. Their healthy gross profits and operating profits from gaming were cratered by their move into ecommerce. Yet, they accepted it. And 4-5 years later, it has paid off. Their revenue is now 10x what it was in 2015 with just gaming.

***

Those are my 4 strategy lessons. I hope that was helpful.

Sea Ltd seems pretty stable right now. Their gaming and ecommerce platforms both have a long runway of growth going forward. But the company is now also well-positioned for more strategic moves. Here are four larger strategic moves I am watching for.

- They will expand their payment business into financial services (i.e., Ant Financial)

- They will spin-off an integrated local and cross-border logistics business (i.e., Cainiao and JD Logistics)

- They will expand into merchant services (like Square? Meituan?)

- They will move into social and interactive ecommerce or C2M (i.e., Pinduoduo)

And none of these are theoretical. We can see Alibaba and Tencent doing all of them. #1 and #2 look the most interesting.

That’s it. Cheers, jeff

—————-

From the Concept Library, concepts for this article are:

- Audience-Builder and Innovation Platforms

- Marketplace Platforms

- Winner-Take-All: Complementary Platforms

From the Company Library, companies for this article are:

- Sea Ltd / Garena / Shopee / AirPay

- #20: Basics of Shopee / Garena / Sea Ltd, Lazada and Platforms in SE Asia

Photo by Japheth Mast on Unsplash

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.