For those of you reading the Moats and Marathons books, I have been slowly laying out the key competitive advantages for digital businesses. And this is really my area of expertise. Here is the list I keep showing.

I think it’s the best list of competitive advantages out there. At least, I haven’t found anything better. And most lists and books on this are not too good.

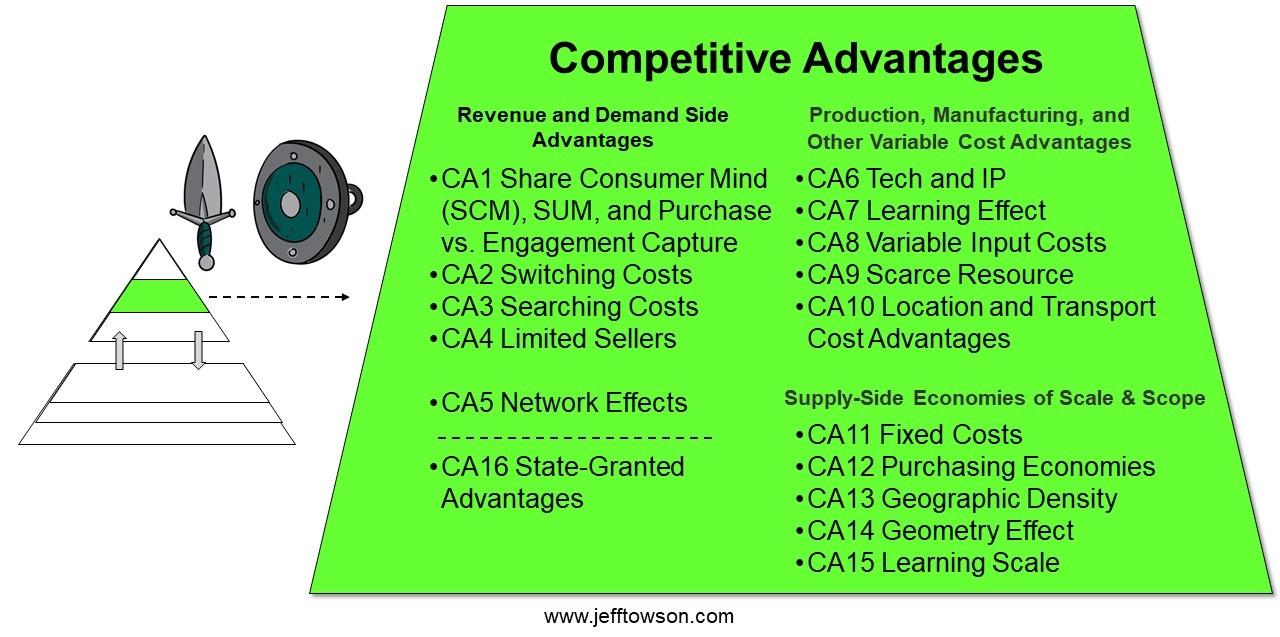

- On the left of the graphic are the demand and revenue based competitive advantages. These give you demand side power that lets you premium price and get repeat business.

- Then there is government and state granted advantages. Sort of stuck at the bottom.

- On the right side, there are the supply and cost side competitive advantages.

- The top five are “Production, Manufacturing and Other Variable Cost Advantages”.

- The bottom five are “Economies of Scale and Scope“.

The cost side is basically broken into variable vs. fixed costs (sort of).

So how do technology and intellectual property fit within this?

Technology and Intellectual Property Can Sometimes Create Advantages in Production Costs.

First off, technology is rarely a source of competitive advantage. It transfers too easily. It gets copied. It goes obsolete quickly. And most of the value gets passed on to customers.

When it does become a competitive advantage, it usually shows up on the cost and supply side. A company can just do things cheaper or better than its rivals. And others can’t seem to replicate it. Tech as a competitive advantage usually shows up in production costs.

This is why I listed it under “Production, Manufacturing and Other Variable Cost Advantages”. You can see it as Proprietary Tech and IP Cost and Supply Advantages (CA6) in the graphic above.

This is actually pretty frustrating.

Because more and more, production costs are being determined by software, hardware, and other data technology. This means that the most important assets on balance sheets are increasingly buried under the general category of “Other Intangible Assets”. It’s getting ridiculous. We can see breakdowns of equipment, site renovations and inventory in process. But all the IP, software, algorithms, and tech are hidden under a generic “intangible assets” term. The accounting system needs to be redone for the information age.

But, as mentioned, most digital and technological advancements spread out across an industry rapidly. Venture capitalist valuation models are always based on technology adoption rates in industry. Most software, hardware, and other data technology don’t create meaningful and sustained advantages in production costs and supply for any specific company. It’s really rare. But that is what we are looking for.

What we are looking for is technology that impacts production costs and that rivals “can’t or don’t want to build”. And we need this to be long-lasting. I am looking for technologies that have a significant and sustained impact on the cost of production for only a few company.

Venture capitalist and tech guru Marc Andreesen looks for “meaningfully differentiated technology”. So, think about hardware, software, and data that has all been specialized over many years for very unique functions. It is highly developed for specific situations. And ideally, this is at every level of the tech stack.

Value investors often look for “proprietary technology”. Which is not necessarily differentiated, but it is protected in a serious way. Either by secrecy or patents. Or just by being difficult to copy.

Those are pretty much the two things I look for:

- Meaningfully differentiated technology

- Proprietary technology

And when looking for meaningfully differentiated and/or proprietary technology, everyone likes to point to the frontiers of technology. To the newest and coolest stuff. Such as AI models driving cars. And the Boston Robotics’ robots doing backflips. But you generally want to avoid the technology frontier for this. Those technologies are still emerging and are still in the roll-out phase in industry. We don’t know how commoditized they will become, which is usually the case.

We are looking for technologies that have already spread throughout the industry. But only certain companies ultimately have them. They have been meaningfully differentiated or locked up (i.e., proprietary) in certain firms. Examples of this are:

- Antivirus companies, like Norton Antivirus, have highly specialized technology for detecting and filtering constantly emerging computer viruses around the world. Very few companies have spent decades developing this highly specialized technology. It is not really proprietary, but it is so specialized that few companies have that much research in this area. Or interest in doing so.

- Hedge funds spend years building trading models and specialized software and hardware. Renaissance Capital is an example. This is under the category of proprietary tech. Lots of companies want to do this. But the tech is closely guarded.

- Logistics companies have AI algorithms that have been trained (and are continually being retrained) with difficult to obtain data. This has an immediate impact on the cost structure of the company.

- Automotive supply companies can have specialized technology for things like the advanced braking systems used in large trucks. These are highly specialized systems that must never fail. It’s not that it is that difficult to copy. It’s just that the risk for not being perfect is very high. So most companies avoid this space. These braking systems are also increasingly going digital and integrating with the truck control systems. WABCO, originally called the Westinghouse Air Brake Company, has been focusing on this technology since its founding in 1869. Buffett has invested.

- Epic Games has its 3D computer graphics gaming engines (the Unreal Engine). This is used for high performance, immersive games and Unreal has been developing this technology since 1998. It’s only significant competitor today is the Unity Engine, which was launched in 2005.

None of the above examples are really cutting-edge technology. They are mostly technologies where lots of time and money were spent by certain companies to develop something very specialized (i.e., meaningfully differentiated). Or they are technologies that are closely guarded (i.e., proprietary). Or that are just not attractive to try to copy.

Example: Adobe’s Meaningfully Differentiated Technology

Adobe was founded in a garage in Los Altos, California in December 1982 – by John Warnock and Charles Geschke. Geschke was a ten-year veteran of Xerox’s Palo Alto Research Park and Warnock had worked for him since 1978.

At Xerox Park, they developed a “postscript page description language” that could describe forms as typefaces. Basically, it was software that let you print what you saw on the screen. Unable to convince management of its value, they left and founded Adobe, which was named after the Adobe creek behind Warnock’s home.

Laser printers and desktop publishing were just taking off at the time. Adobe was profitable almost immediately. And shortly after founding, Steve Jobs tried to acquire Adobe for Apple. Eventually, Apple made an investment and used their postscript language for Apple’s laser printers. Adobe’s postscript eventually became the industry standard for printing and it was licensed to hundreds of third-party software companies and printer companies.

From there, Adobe launched software product after product. It made digital fonts. It made Adobe Illustrator. In 1989, it launched Adobe Photoshop, which became its flagship product. In 1991, it launched Premier Pro. In 1993, Adobe Acrobat and Reader. And on and on.

Today, Adobe is a software company that provides a full suite of +20 tools for creativity. That is their technology specialization. Everything they have built and refined over decades are tools for creativity. These include graphic design software, web design programs, video editing / animation / visual effects programs and audio editing software. Their main creative tools are:

- Adobe Reader, Pro and Sign – for document publishing and sharing.

- Photoshop – for editing images, graphics, and art.

- Premiere Pro – for video and film editing.

- InDesign – for designing and publishing layouts for print and digital.

- Illustrator – for creating art and illustrations.

- After Effects – for creating visual effects and motion graphics.

- Lightroom – for editing, organizing, and sharing photos.

- Premiere Rush – for editing, organizing, and sharing videos.

- Stock – a library of photos, graphics, and videos.

Adobe is currently expanding from creativity tools into what they call “experience products”. These are tools that let creative professionals take their created media and utilize it in a user experience. This includes distribution, monetization, social aspects, and such. I put all their software into two buckets:

- Creative tools and infrastructure

- Operating tools and infrastructure

So…

- Is Adobe meaningfully differentiated technology?

- Does it create a production cost and supply advantage?

- It is too hard or just not worth it to replicate?

- Is this situation going to last?

Adobe has been building this software for over 40 years. It’s not terribly advanced. But it is highly specialized and meaningfully differentiated. This clearly plays out in many ways versus their competitors. It’s a unique offering. There is bundling. There are network effects and economies of scale. But we can also definitely see it as a competitive advantage in their costs of production. Any company that wanted to replicate this technology would have to spend more in production over a long time. It just doesn’t take Adobe as much time and money make the newest version of Adobe Acrobat. And this will happen regardless of how many sold (so it is a variable cost advantage, not a fixed cost advantage). Although trying to separate out the fixed and variable production costs becomes impossible beyond a certain point.

Intellectual Property Is Also About Production Cost and Supply (Mostly)

I named this competitive advantage CA6: Tech and IP Cost and Supply Advantages. You could break it down other ways, but these are the three most common types I see.

- Meaningfully differentiated technology

- Propriety technology

- Intellectual property

And intellectual property is pretty easy to understand as a competitive advantage. Disney is in a lot of businesses. But it’s mostly about developing, acquiring and licensing intellectual property. They’ve been licensing Snow White for +70 years. Go into their offices in Shanghai and its just one big licensing department. That’s how you end up with Iron Man backpacks and Darth Vader electric razors.

So it’s copyright, patents, trade secrets and all the other mechanisms to make an idea protected property. And this can happen even when there are no actual government filings. For example, it wasn’t until 2017 that China was finally able to replicate the technology for making the rolling ball in the tip of the pen. Despite manufacturing +40 billion ballpoint pens per year.

All of these are clearly a production advantage. But are these competitive advantages based on being cheaper?

Not really.

You’ll notice I titled CA6 “Cost and Supply Advantages”. Often the advantage is not about being cheaper. It is about having access to supply that others don’t. Like using Iron Man in movies or backpacks. Or maybe they can get access to the supply but it costs them a lot more. So it’s sort of a mix of cost and supply. But it definitely plays out in production.

That’s it for today. Cheers, jeff

——–

Related articles:

- Ant Financial Is 3 Platform Business Models Combined. (Jeff’s Asia Tech Class – Daily Lesson / Update)

- Ant Financial’s Big Money is in Asset-Light Credit Tech (Jeff’s Asia Tech Class – Daily Lesson / Update)

From the Concept Library, concepts for this article are:

- Competitive Advantage: Tech and IP Cost and Supply Advantages

From the Company Library, companies for this article are:

- Adobe

——

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.