In this class, we discuss Chinese bike-sharing company Ofo. And their spectacular rise and fall.

You can listen here or at iTunes here.

The exercise for this class is:

What should Ofo have done?

1) Partner with a major digital platform ASAP. No matter what it takes.

2) Copy Hellobike. Avoid the competition. Go to markets or segments with little competition and try to get to operating break-even.

3) Split the company into a good co and bad co. Fund the good company and don’t tie it to the cash drain of the bad co.

4) Carl Icahn option. Go activist investor and try to split the company, replace management or other.

What would you recommend to the CEO?

- Write 3 paragraphs with your answer. Do it on your smartphone. Or a PC. Or a piece of paper (take a picture and save it).

- Think about bundling and the emergence of greater ecosystems.

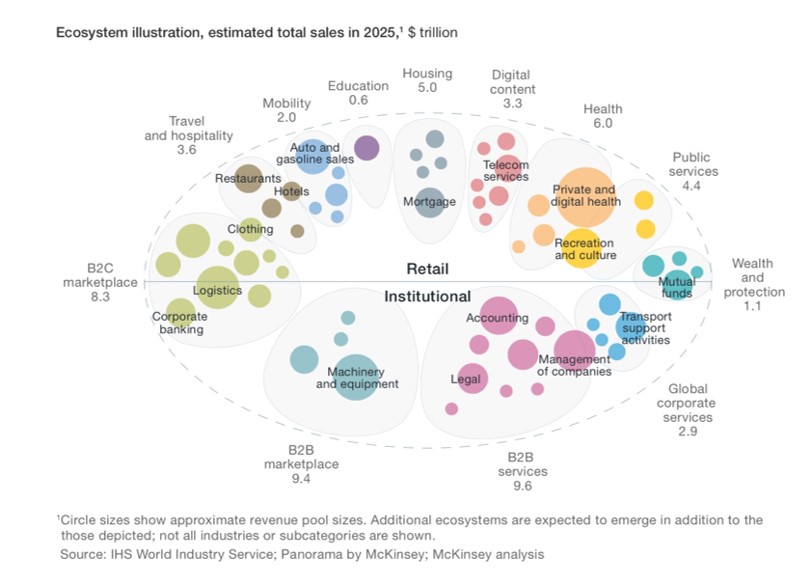

Here is the McKinsey & Co slide cited:

Articles / podcasts cited in this class:

- What Should Giant Bicycles Have Done About Mobike and Ofo?

- How Bundling Benefits Sellers and Buyers (Chris Dixon)

Concepts for this class:

- Money Wars

- Ecosystems

- Bundling

- Willingness to Pay and Consumer Surplus

Companies for this class:

- Ofo

- Mobike / Meituan

- Hellobike / Alibaba

———-

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.

——transcription below

:

Welcome, welcome everybody. My name is Jeffrey Towson. I teach at Peking University and this is Jeff’s Asia Tech class. Now the question for this episode is what should Ofo have done? Ofo, the famous bike sharing company out of China rocketed way up and rocketed way down. And the question we’re gonna ask is what should they have done? There’s some obvious answers to this and I think there are actually some pretty important strategic questions issues underneath that so that’s what we’re going to take apart. But first if you haven’t subscribed please do so at jefftowson.com there’s a 30 day trial membership very easy to do and you can also go to itunes and follow there which is where all the podcast lectures are hosted. Okay, on to our question. What should bike sharing giant OFO have done? Okay, let’s get right into this case because I think it’s kind of a fun one. And it was, you know, in the news a lot, this whole idea of bike sharing coming out of China, kind of like, you know, amazing surge of activity, venture capital, company formation, a lot of consumer adoption, all really impressive. And then, you know, of the 30 plus companies that got founded. You know, but three or four pretty much cratered within the year and the the main leaders Mobike definitely being one hello bike which people don’t talk about very much very important and then blue gogo DD bikes, you know Those two are still doing quite well and there have been incorporated into the larger companies now and then awful which ended up Really was the market leader for a long time ended up sort of on its own. Pretty much closed down at this point. I’m not sure their legal status, but I think it’s pretty close to that. You know, the question here is what should they have done? Because they were clearly the market leader and they were in great shape and they had done everything. You know, they were really good position by a couple reasons. Number one, they were the market leader. They had beaten the surge. the sort of frantic rush into the space. They had done that. They’d gotten a lot of consumer adoption. That’s incredibly important. They had partnered up with the right people, like their venture capital backers were pretty much the who’s who of China venture capital. And they had also partnered with Didi and Alibaba, so well, and financials. So, you know, they had kind of all the pieces in place and then things really cratered. So we’ll talk about kind of why that is, but also what they should have done. It’s easy to point fingers and say, ah, see, you know, they, they screwed up and they did this. Okay. Whatever. The more interesting question is what would you have done? If you had gotten the phone call, please come down. We want to talk to you about this. We hear you kind of know this stuff. What would you have told them to do? And I would argue to you that is a much better skill set to have in life. Uh, I spend, you know, it’s funny. I spend, uh, probably 30 to 40% of my time studying great companies, like the Warren Buffett type great companies. And some of those are the digital giants of China, Asia, like Alibaba and those. And that’s very instructive. You can learn a lot with those. But in terms of doing business and having an impact and really making money, you’re far better off focusing on sort of screwed up companies, not too screwed up, but moderately screwed up. where there’s issues and problems. And if you can come into that sort of gray area and do something that’s a pretty lucrative space. So the person I actually study in that regard is Carl Icahn, who is sort of famed raiders turned activist investor has been doing this for 30, 40 years now. And he studies the messed up companies. He comes in as an activist or a raider and he knows how to make money as an investor on. mediocre slash messed up companies. And it turns out there’s a heck of a lot more of those. It turns out the problem with the Warren Buffett strategy, I’m gonna invest in great companies with great management, is there’s not very many of them. And that’s a problem. And then on top of that, they’re rarely selling at a discount or they rarely need anything because they’re great. They don’t need capital usually. They’re usually not cheap if you’re gonna buy the stock. They don’t have problems because they’re kind of great. But if you can make money or be an effective manager or turnaround person in mediocre or screwed up scenarios, you can actually do very, very well. I was talking to a colleague recently who has been involved in Disney in Asia for a long, long time. People don’t talk about Disney China too much, but they weren’t doing well for a long time. But in the last three to four years, they have really turned that around. And I kind of know the guy who did that. You know, they’re even done things like that have really taken off. You know, that’s the kind of manager you wanna be, the kind of exec you wanna be, or the type of investor you wanna be. Someone who can come into a muddy, struggling, frustrating situation and make it happen. Now, to do that well, you also have to know, like which are the ones that are too hard? Like this is the Warren Buffettism. On his desk, there’s a little plaque or a little, you know, placard that says too hard. You gotta know when it’s too hard and not worth your time. You’re looking for the sweet spot between, okay, it’s not perfect such that there’s no opportunity to do anything as a manager or investor, but it’s also not so screwed up that it’s just too difficult. You know, don’t get overconfident. Don’t think you’re gonna fix miracles. You know, be a miracle worker. So you gotta find that kind of sweet spot in there of the not too hard bucket. Okay, OFO, I think, was in an interesting situation in 2018. In the first podcast I did, well number two was about what should giant bicycles have done in 2016-ish when Mobike and Ofo burst onto the scene and rocketed upward. Now I don’t remember the problem with that podcast. It was the first one of these I did and the audio quality is awful and well it’s not awful but it’s bad. So anyways I’m going to put the link to that one in the show notes for this one. I think that’s an important question of what do you do if you’re an established company and this sort of digital attacker pops up. And I think the right answer in that scenario was, you know, to basically do nothing. That giant bicycles best strategy was to wait a year, two years, and then see what’s going to happen and maybe buy a straggler or a struggler at that point. And the sort of concepts I put forward in that class were really three. I put forward the idea of Clayton Christensen jobs to be done. And that led into this idea of access versus ownership businesses. And that was really, I think, the big takeaway for that class was if you stop talking about sharing economy, which I don’t think is a useful concept, and you start thinking about businesses that you access, I’m going to rent a bike, I’m going to take a taxi, I’m going to rent a hotel room versus ownership business, I’m going to buy a car. I’m gonna buy a bicycle, I’m gonna buy a moped, I’m gonna buy an apartment. What consumers want is actually very, very different within those. And how you compete as a business really is very different depending which of those two you’re in. If you’re in the selling bicycles or car businesses, you’re gonna win by building very different capabilities than if you’re in the rental car or rental bike business. And I would put taxis in there as well, ride hailing, things like that. So that was kind of, I think, the key dynamic there. And based on that, I sort of argued that, look, you can probably, Giant Bicycles is very good at selling bikes for ownership. They’re very good at design, manufacturing, retail, go to market, shelf space, that sort of stuff. And they should stay with ownership as a strategy for now. and this access business model, which was bike sharing, you’re really not competing on any of those factors. You’re competing on mostly convenience and low price. So let them do that game, let all the craziness, the animal spirits sort of work themselves out and wait a year. And there doesn’t appear to be a competitive advantage in bike sharing. So… you have the flexibility to wait. Now, if this was a business where there was a very powerful network effect or other competitive advantage, sometimes you have no choice but to jump in because if you wait a year or two years, it’s too late. The market is closed up, you can’t get in. But in bike sharing, I think, look, I didn’t see a competitive advantage, so you could jump in later if you wanted to. And I think the sort of ownership versus access business model tells you that you’re probably not gonna be in that business yourself. but you could have a partnership, start a second company, buy somebody, and that’s fine. You can kind of wait and see on that, which was sort of how I came down on that one. The other idea, I put sort of three main ideas for the first, that episode. The other one was demand purification. That what digital tools let you do is take a business like buying a bike or renting a bike and purifying. what you’re offering to consumers. It turns out software is pretty good at that. And by adding a little bit of smarts and digital to a traditional business, bike rentals, you were able to sort of purify demand and give people just what they never knew they always wanted, which was the ability to rent bicycles anytime you want, whenever you want, leave them wherever you want and pay very little money. So it was demand plus low price was the offering. Okay, that was kind of the first episode. I’ll put the show notes in there. You can link to it and listen or, you know, forgive me the bad audio quality for that one. I still, still bugs me, but I was just getting started. Okay. So that was kind of the early bike sharing story. Then we fast forward to 2018. Then we get to sort of, okay, later stage bike sharing, which I think is a different question. And at that point, a couple of things had happened. late 2017, Blue Go Go, who was the number three player, they had the blue bikes, Ofo had the yellow bikes, Mobike had the gray and orange bikes. Blue Go Go had basically gone bust, you know, quite suddenly they announced we’re closing our doors. And okay, that was one sort of phenomenon. Hello Bike, people weren’t really talking about them back then. They were kind of, they were sort of the dark horse. Everyone else was fighting for Beijing, Shenzhen, Shanghai. Hello Bike was sort of in second and third tier cities, moving sort of quietly up the outside lane. Mobike at that point was number one or number two, depending how you measure such things. And Ofo was on its own, but Ofo had ties with Didi, and Ofo had ties with Ant Financial slash Alibaba. Okay then a couple things happened in sort of mid 2018. Basically what happened mid to late 2018 was the money war started to end. And we had basically seen a money war. This is another one of the concepts we’ve talked about or I’ve talked about is that in China in general in digital especially but in lots of spaces you get these money wars where people use money not for blitz scaling. which is something we’ve talked about, not for sort of fast scaling, but just as a weapon to put your competitor out of business. That’s really what you’re doing. You’re taking their business. It’s not like you’re flooding money into the space in order to grow really quick. That could be fast scaling versus split scaling. No, no, no. You’re using your money. You’re turning that gun directly on your competitor to take their business or force them to spend and match you. And you’re hopefully thinking that they don’t have enough money or they can’t raise as much because they’re not a market leader like you are. And you can bleed longer than they can bleed before one of you collapses on the floor. So that’s kind of money war. So we were kind of seeing the end of that as a phenomenon. It was getting harder to raise money. You know, this idea is you put money into these businesses, the market leaders try and grow as fast as they can. by spending a lot of money, which gets you scaling, but it also, it’s a weapon against your competitor. Because you’re a little bit bigger than your competitor, you’re the market leader, it’s easier for you to raise money at a higher valuation. So you do that and then you spend that money. And the middle and sort of the middle of the pack and the laggards, they can’t match you on your fundraising or your spending and you basically put them under. Okay, so there was a lot of that happening, but that was kind of coming to an end, more or less. Alright so what happens now mid 2018 I start hearing kind of a lot of rumors about OFO. OFO is based in Jonggwon Sun which is you know it’s a 10 minute walk from Peking University. I walk down there to get coffee all the time. There’s also a good car for right there. And so I hear a lot of rumors going around and then DD is actually. just to the north of campus. This is all northwestern Beijing. Just to the north of campus is a new sort of digital business park, and Didi is up there now. So both these companies are kind of in the same spot. And I start hearing lots and lots of rumors about OFO management problems, lots of spending, huge amounts of spending, international expansion that doesn’t necessarily make sense. And who knows, they’re rumors, you never know what’s true, but I’m hearing a lot of them. And then something happened, and I hear one rumor in particular that got my attention, which was Didi was unhappy with the management at OFO and what they were doing and how they were spending. And they had some managers that were deployed from Didi to work at OFO. Now, I don’t know if that’s true, I’ve never been able to confirm it. And sometime in that period, The rumor goes around town that those managers have basically been shown the door and told the leave and go back to DD. Again, I don’t know if that’s true, but I heard it from enough people that I don’t know all the room. I don’t know if the rumors are true, but they were all in one direction, which gave me the indication something was going on. Okay, then something does happen that gets my attention. November, I think it was December 2017. there’s an announcement that DD has purchased Blue Go Go, which was the number three player that had gone into some sort of bust slash bankruptcy, they buy them. Okay, that’s a real move. That’s, you know, that’s the real thing. If you are business partners with someone and you’re their bike sharing company and they’re the mothership, because keep in mind, bike sharing is a relatively small business, one to $2 billion. Mobility, DD, you know, you’re talking 50. 40, 50, 60 billion, who knows? But that’s a much bigger company. When your big parent partner invests or buys your competitor, that’s basically like your wife telling you she wants to date other people. That’s a big, huge deal. And then around the same time, Didi announced that they were launching their own bike sharing, which was called Didi Bikes. So they have sort of two. different types of bike sharing, which they eventually collapsed into one. Up until then, if you wanna go on DD and you get a car fine, you get a taxi fine, but if you press the bike button, you could get Ofo or a DD bike as they were starting to be done. Now, if you press that button, you can get a Blue GoGo or a DD. I think they finally collapsed them. So that struck me as, okay, something really big has happened here. And that was kind of… Thing number one. Thing number two was in early 2018, Mobike basically sold itself to Meituan. Okay, that’s a big deal. I think this was, I don’t have the exact date, March 2018. And then also along the way, Alibaba buys Hello Bike. So we see a couple things happening here. We see the money war is maybe coming to an end, and we see bike sharing as a service starting to become lumped into larger platforms. Larger services, suddenly. Bike sharing is not a standalone company. Bike sharing is just one service within mobility. You go to one app, you can get a taxi, a car, a bike, a metro ticket, whatever. So sort of two things happened at that time. Okay, now OFO, what basically happens over the next year, 2000, you know, really 18, is just cash problems. I mean, it’s suddenly… There’s these rumors that they’re meeting with DD. They’re going to merge up with DD. Doesn’t seem to happen. People say there was like three or four different attempts to do this. At some point they all fell apart, but they’re finding it harder and harder to raise money. And because of apparently the board structure, certain people have vetoes. So it’s not clear if they even can raise money or not. I’ve been trying to get sort of the right story on that. I’ve never really gotten the true story. Okay. Now what happened with Opho? I think there’s a couple takeaways here and then we’ll get into some theory. One, definitely they didn’t preserve their capital. If you’re gonna be in a money war, and there’s a lot of these in China and Asia, really a lot of places, you’ve gotta preserve your cash for the longterm. There’s great stories of Wan Xing, the founder of Meituan. This is like his third. Internet digital company he’s founded and in the past before Maituan he had troubles with running out of money halfway through the money war. He didn’t preserve his dry powder He ran out of money. So When he launched Maituan is sort of a copy of Groupon. This is back 2011 2012 One of the reasons he won that is because he preserved his money. Okay, so the argument is like OFO spent but They spent too lavishly and they ran out of dry powder before the fight was over. Okay, I don’t really know their balance sheets so I don’t know, but yeah, that’s a good message. There’s lots of stories like this. The one I really like is actually Ctrip versus Elon, which is something people don’t really talk about. Ctrip is the market leader, Xiatong, and their big competitor for a long time was Elon.net. which was owned by Expedia out of the US. And Expedia actually did very, very well in China about 15 years ago. They came into China early, they invested, they got one of the local champions, Yilong, and the market collapsed to a couple players. You know, C-Trip and Yilong are the ones that people talk a lot about. Choonar is another one. But then the money war didn’t end, even though the market consolidated, the money war kept going for like 10 years. And eventually Expedia sold their stake and went home, because they were losing like $100 million a quarter still 10 years later. Basically, this is kind of a strategy in China, is you believe the foreigners long enough and they usually go home. So you kind of gotta think about that. Anyways, definitely OFO didn’t, keep their capital, they didn’t have enough, they ran out and the money war wasn’t quite over so then you get into cash problems, that’s a problem. If you want to put your competitor out of business, you have to go after their cash. I mean that’s it. I mean you can steal customers, that’s one thing. You can steal market share but if you’re going to put them down, you have to hit them in the cash. Okay. Another thing I think OFO had an issue with was they went international before they had really won in China. Usually companies go international out of China after the China fight is mostly over. So Didi did that. Alibaba did that. Tencent tried to do that. TikTok is kind of doing that. But they were pretty well established at home before they did that. And they had a pretty good cash machine often at home. OFO and Mobike really went international quite early on. Europe, Manchester, Milan, Brazil, Thailand. I went to the opening of Mobike in Thailand, which was quite cool. Now that’s not terrible. I think it can make sense. It increases your valuation, which is helpful if you’re raising money. In retrospect, it was probably not totally necessary. But I don’t think it was a major one. And, you know, a lot of stuff is obvious in retrospect. So fine, not a huge deal. Third thing I think they did was, that was not great, was they stayed a standalone bike sharing company. And it was pretty clear really back in 2017 that that wasn’t gonna be viable. That bike sharing doesn’t make sense. One, as just a stand-alone company, this is kind of one of the different things about China and the US. In the US companies, digital companies tend to stay in their lane. Like Uber does transportation, Facebook does social media, Amazon does e-commerce. In China, people move into each other’s lanes all the time. Tencent is tied in with e-commerce. Alibaba has gone with Ding Talk into some social media aspects. They’re all doing video and music sharing, streaming. So people tend to jump into each other’s lanes a lot more. Part of that is does the service make sense, which I’m gonna talk about. The other part is like, you just have to be a bigger animal. That, you know, this is the jungle and if you’re gonna be in the jungle, you can’t be the bunny rabbit. Like, you don’t have to do anything wrong to get into trouble as the bunny rabbit in the jungle. Just being the bunny rabbit is enough that you’re gonna attract predators. You have to be a lion or you have to be a pretty big animal. And it was. And it pretty clear that bike sharing, it was just too small of an animal to compete in the digital B2C space. And the cash flow being thrown off was not enough. You know, Alibaba is a cash machine. Tencent, especially their online gaming, is a cash machine. Matewan is still working on it. They’re getting closer. You’ve got to be a certain size of animal. And it was pretty clear that bike sharing was going to be a small business. No, it’s a good business. There’s nothing wrong with being a smaller business. I kind of think about bike sharing as like a big vending machine business. And there’s absolutely nothing wrong with that. But you got to know that you’re kind of the smaller animal in the jungle. And that was one that it was sort of too small. And then two, bike sharing was probably going to be a type of a bigger service like mobility. that like it really doesn’t matter. I don’t really care if it’s a bicycle or a scooter or a taxi or a car. I just need to get from here to there. That’s all I care about. On my phone, it’s one app. So it’s pretty obvious this was gonna collapse into one sort of mobility app and you couldn’t be standalone. And Opho was very adamant, at least publicly, about we’re gonna be a standalone company no matter what. Now maybe that was posturing because they were negotiating. I don’t know, but. Definitely that turned out no. I mean it was pretty clear that was not gonna work and Then maybe the last thing I think they did wrong They didn’t kiss the ring of Didi and Alibaba And this goes back to the lion analogy. You have to know who you are in the jungle any given day of the week the CEO of Didi You know Jin Liu or Chung Wei Or you know at alibaba would be daniel john or pony ma i mean any of these people any given day of the week could get up and say i wanna crush and take that business bike sharing and they could do it and there’s nothing you could do to stop them. They have the money they have the resources they have the tech they have the consumer base they could take your business any day of the week so you gotta gotta you’re not the you’re not the lion. You’re kinda the bunny rabbit or something so you. Look, if you can’t be a lion, you gotta be good friends with the lion. So, you know, when there were these rumors about, oh, Dee Dee’s unhappy with Opho, man, you gotta get yourself across town, you gotta kiss the ring, and whatever. You know, you want them to personally like you. Like, I don’t care what it takes. Be their favorite person. But you, you know, that’s your ideal solution. And if you can’t do that, for God’s sakes, don’t have them be mad at you. You know, that’s just. You can’t do it. I mean, literally all it would take is, let’s say a Didi, Chung We or Geneville, just to randomly turn to one of their vice presidents, any random Tuesday and say, you know what, let’s just take over bike sharing, do it. Okay. What’s next on the agenda and you’re dead. That’s all it would take. So anyways. Now why didn’t they you know why did they act the way I don’t know why they acted the way they did people talk about management and board issues at all. I don’t really know what’s going on. Who knows. Okay so that’s kind of where I put it for you know what should have done that’s a scenario let’s say early to 2018 there they’re running out of cash but they’re not in a crisis yet you can see the market consolidating you know you’re a smaller animal. What do you do? And that was really the window of time to do something. So that, I think, takes us up to a little bit of theory. Now, I tend to repeat myself quite a lot when it comes to the theory, the concepts, that sort of stuff. And that’s actually on purpose. My approach here is, it’s almost like the anti… news strategy you know the news is all about here’s what happened this week usually it’s about here’s what happened today. I think that is like ninety nine percent of that turns out to be not useful and or important and if you go back think in your head like all the news you read of whatever sector you’re in let’s say two thousand sixteen how much of that ended up being important. I’d be surprised if it’s more than two or three percent. It turns out most stuff that happens on a daily basis is not that big a deal when it comes to business and strategy and what companies are doing. And in addition, the stuff that is really important is often stuff that happens quite slowly that doesn’t happen in a way that would ever be covered by the news, changing consumer behavior, longer economic trends, urbanization. Those things are incredibly important and they don’t get captured by that at all. So what I tend to do is I tend to focus on a relatively short list of important ideas and sort of variables related to companies. You know, it’s not thousands, it’s probably a hundred. And I spend a lot of time watching them. And if those move, then I’m very concerned. If whatever’s happening in the news doesn’t impact one of those. I really don’t care that much. So what I do when I’m talking about this stuff, especially the kind of the big ideas is I will repeat the same ones over and over and over. Because I think if you get those right, all the small stuff usually doesn’t matter. And, you know, anyways. So one of the ideas that I’ve been sort of thinking about a lot is this idea of sort of consumer ecosystems sort of… what I call digital physical consumer ecosystems, where when you start to merge online with offline, which I’ve talked about in a previous lecture, for regards to retail, what you’re doing is you’re combining the physical assets with the digital aspects, the e-commerce site with the hum-a supermarket down the street. And as you do that, the physical world is sort of starting to behave like the online world. On the online world, things are all sort of collapsed. You go on to an amazon or alibaba and you can buy something you can watch a video you can chat with your friend it’s all kind of the same thing on the same screen at the same time. That is very different than if you walk down the street and the hospitals the building on the left and the furniture stores the building on the right and the movie theaters down around the corner you know the. The physical cost structure tends to create industry barriers that maybe are becoming less relevant. So as you start to combine digital with physical, are the industry barriers we are so, or not industry barriers, industry demarcations that we are so comfortable with, are those starting to shift, to fall? And we can definitely see this between like e-commerce and entertainment, that it turns out it’s kind of the same thing. It’s just a consumer experience. And we’re starting to see this phenomenon happen and this is why traditional players are getting surprised so often because someone they didn’t think was their competitor is suddenly in their business. Okay, now a couple years ago, McKinsey and Co. came out with a fairly cool little paper arguing that by 2025 there’s going to be probably one, two, three, four, about 12 to 15 ecosystems that are going to emerge. And these ecosystems will combine our online and physical lives and businesses into sort of one thing. And some examples of this would be mobility, which is what we’re talking about. The argument is, look, you don’t need a bike sharing app and a scooter app and a taxi app and a metro app. That’s just one huge mobility service that integrates the online and the physical aspects in one button, because that’s all consumers care about. So I press my one button, and that gets me from here to there, and it recommends how you do this. It could be a metro ticket plus a bike plus a car. And I was at the DD headquarters, must have been a year ago, and that’s basically what they were talking about, that you’d have one button, and it would give you three recommendations for how to get from here to there. One would be the fastest route, one would be the cheapest route, and one would be their recommendation. So three options, and it would just pull all these services together, online, physical, all of it. Now within mobility, we could call this a greater ecosystem. You could also see things like car purchases. You could see car rentals. Driver services, which is something DeeDee’s focused a lot on, which I think is really cool. Uber just announced this that they’re going to do car financing and stuff. So you could see mobility as sort of a greater ecosystem. You could see education as a greater ecosystem where you get your certifications, your college, your high school, your online, your homework, your support, your supplies, your books, your paper, your pens. The software, that could all be one thing. Digital content could be one. Health could be another one, your insurance, recreation, wellness, hospital visits, get your teeth fixed, beauty treatments, public services. Definitely wealth and finance and insurance could be one. And there’s one that they call the B2C marketplace, which is, that’s kind of everything consumers buy, like soap, clothes. You know, you could say buying a movie ticket could be in there, buying dinner. whether you have it delivered or whether you go to, you know, go down to the restaurant. So there’s a lot of logistics in that one. And that’s kind of what Alibaba looks like to me, that, you know, they are building what I’ve been calling a digital conglomerate. You know, I would say Tencent is kind of similar, but this idea that this becomes this greater sort of digital Orlando, Florida. That’s all B2B, if you, I’m sorry, B2C. If you go to the B2B side, you can do things like B2B services, which might be management, accounting, legal. There could be a B2P marketplace where you buy machinery, equipment, retail, you know, kitchens, stoves, things like that. And then there could be sort of transport legitimacy. You can kind of see that maybe there’s, they say 10 to 12, I’m sorry, say 12 to 15 of these greater ecosystems that are coming as a result of the integration of digital and the physical world. the industry barriers, boundaries are moving and or falling. Everything is becoming much more data driven because you have data within an ecosystem that lets you integrate these things, but also lets you innovate fairly quickly. And you can see these surprising events where people are jumping from one industry to another, like basically like Mobike jumped into the bike business. And you know, the the giant bicycles didn’t see it coming. They didn’t see the idea that Alibaba, Didi and Meituan would all be doing bike rentals. OK, so a lot of interesting aspects of that. So I think within that, the question is, how do you compete in that space? And I’ve talked a lot about digital platforms. Well, not a lot, but I’m starting to. Digital platforms are a business model. They’re a network centric business model. where your primary goal is not to buy and sell something, but to enable interactions within a ecosystem. So I think of them as ecosystem orchestrators. Okay, so if the McKinsey argument is right that we’re seeing these greater ecosystems emerging, then platform business models within that could have a fairly powerful role orchestrating parts of those ecosystems. Okay, that gets me back to my sort of lion and the bunny rabbit analogy. If you’re Mobike standing alone, and if you’re OVO standing alone early 2018, I mean, don’t you have to partner up with a larger digital platform and a larger player? Because I mean, Mobike, OVO, neither of these are platform business models, even though they’re called sharing. It’s not true. I mean, they’re just, they’re just digitally innovative service businesses, fairly traditional ones. They’re not platforms. You want to be on a digital platform that’s playing a major role orchestrating the ecosystem. especially if your service, bike sharing, is so obviously just another version of mobility. So within this idea, I think you had to get with the bigger animal and you had to be with an ecosystem orchestrator, a digital platform. So I think that was pretty clear early on. So that’s kind of concept number one for today is think about these greater ecosystems emerging more and more. They’re happening pretty fast in retail, pretty fast in communications, pretty fast in entertainment. People keep pointing to education and healthcare and public services as a natural place for this, but of course those things happen much more slowly and or not at all because those decisions are often politically made more than anything else. I come out of a healthcare background. Okay, so that’s kind of concept number one. Think about sort of this idea of greater ecosystems and what that means. The other idea I wanted to do today, on sort of the concept list is the idea of bundling. Now bundling has really interesting economics. I’m going to cite some stuff from, there’s a web page by a guy named Chris Dixon, D-I-X-O-N, I’ll put the link up there so everything I’m saying is pretty much from his website because he has a very good summary of bundling. But bundling is one of these things that economists, business people have done forever. And has suddenly become much more important because of digital economics. You know, this is kind of a follow up for the last two lectures, which was, you know, digital economics made things like versioning. Very, very important. They made things like compliments. Very, very important. They’ve made things like consumer surplus. Very, very important. Now, these are traditional ideas, but they’ve become a lot more important. And I’ll talk about a couple of those probably today in the next class. one of those ideas bundling. We’re gonna take two products, we’re gonna bundle them together and you’re gonna buy both for one price. So, you know, you walk down the aisle at the Walgreens or the Carrefour, whatever, and you can buy shampoo or you can buy shampoo bundled with conditioner and bundled with soap, like in one little package for a different price. So this stuff’s been going on in products forever and definitely in services as well. Right, it’s a lot easier to bundle services. We will do your consulting and we will sell your apartment for you. We will do the listing and we’ll do the sale. We’ll do the advisory work and the transaction. You can bundle services pretty easily. Okay, when you start getting into digital, bundling is pretty powerful. Now the example that Chris uses is the idea of cable television. Because cable television, like, If you’re in the US or Europe, you probably have a cable package. You’ve got 300 channels. The vast majority of them you don’t watch, but you paid for them all. And that was a good deal for you. Well, it was a really good deal for Disney and ESPN and others, but it was also a very good deal for the consumer, even though people complain about this. South Park has an amazing episode about, you know, the cable company, even though consumers complain about this, it’s a very good deal for them. the fact that they’re buying 200 channels, even though they like to complain about it. Now, the example Chris uses is, okay, let’s say you can buy ESPN and the History Channel, and you have two different types of consumers. You have a sports lover and you have a history lover. So the first thing you talk about is willingness to pay. Now, willingness to pay has become big in digital. Willingness to pay is, here’s how much I would be willing to pay for this service like, YouTube or Youku. People actually would be willing to pay for that. You don’t have to offer that for free. Now they choose to, but they don’t have to. You could actually charge people for that and they would be willing to pay for it. Now sometimes a competitor will offer something cheaper so that’s not an option, but the willingness is there in the consumer mind because of the perceived value. And depending on the competitive dynamic you may not be able to charge that. And depending on whether it’s a digital good, you may choose to offer a price far below the willingness to pay because it makes sense strategically to do that. And the gap between your willingness to pay and the actual price, we call that the consumer surplus. Now, the digital age is just an explosion of consumer surplus. We are getting everything free or dramatically less than we’ve ever gotten things before. It’s amazing. Everything in the app store almost consumer surplus. So, you know, this is all amazing for us. None of this is captured in GDP numbers, which I think is interesting when people say, oh, the GDP is not going up as fast as we want. Oh, you know, incomes are not growing as fast as we think they should be. Certain people’s incomes are growing faster and people’s incomes are growing slow. You hear these discussions all the time. Nobody ever talks about the consumer surplus. Even like the poorest person in, well, not say not poorest, but even low income people in Africa are getting an amazing consumer surplus where they can get on Facebook for free and they can watch YouTube for free and they can do Twitter for free. Well, they’re probably not on Twitter, but there’s an explosion of free stuff, which is amazing, that’s not priced in when people calculate this stuff. Okay, that’s a side thing, not terribly relevant. Alright, so we have people who love sports, people who love history. You measure how much would a person who loves sports be willing to pay for ESPN? The example Chris uses is $10. We think, let’s just use that, okay, this person is willing to pay $10 for the ESPN because they love sports. The history lover is willing to pay $10 for the history channel because they love history. However, each person is also willing to pay for the other one. the sports lover is willing to pay $3 for the History Channel. They’re not willing to pay $10, they’re willing to pay $3. Because they don’t love it, but you know, if it’s $3, I’ll buy it because I actually do like it. A History Channel, same thing. They are willing to pay $10 for the History Channel, the history lover, but they’re also willing to pay $3 for ESPN. So how do you price? Well, if ESPN prices at $10, well let’s say ESPN prices at $9. and let’s say history channel prices at $9. So they take the willingness to pay and they drop it 10%. That gets you to nine. So the sports lover gets the show they want and they get a 10% sort of $1 consumer surplus. Great, history lover, same thing. They pay $9, they get the channel they want and they get a $1 consumer surplus, great. If you assume that you have, let’s say, just one of each, then the overall income coming in is about $18. And the consumer surplus is $1 for everyone. So these sellers make $18. And the consumer surplus that everyone gets is $1. Okay, fine, because they’re not buying the History Channel if you’re the sports lover and vice versa. Okay, let’s say you bundle them. When we bundle them, what we do is we sell both. channels together for thirteen dollars. So suddenly it’s worth it for the ESPN, the sports lover, to buy both the ESPN and the History Channel because it’s ten plus three. They’re willing to pay for both. And if we sell similarly the History Channel for thirteen dollars it basically maximizes where everyone is willing to pay. And you discount it a little bit, let’s say 10%, so you price both channels bundled at 11.70, which is a 10% drop. Now what happens then? Well, both parties should be willing to buy the bundle. So the sports lover is actually spending more than he or she would have, and the history lover is actually spending more than he or she would have, but they’re actually getting a good deal, and the person selling, suddenly gets whatever it is 11 by 24 dollars. So the amount of money coming in goes from 18 to 23. So the sellers are doing better. At the same time, the customers are also doing better because they’re getting a consumer surplus of about a dollar 30 each. Everybody wins. It’s better for the consumer. It’s better for the seller. And what they’re really doing, if you want to look at Chris’s page, you’ll see what they’re really doing is they’re flattening the demand curve. Usually, well, I won’t go into that because I, if you’re not looking at the chart, it’s hard to explain. But the idea is when you start to bundle, you can get a win-win for the buyers and the sellers and it’s particularly easy to bundle digital goods and information. Why? Well, because of what we talked about before, the sexy but dangerous economics of digital. You have low marginal cost and they’re non-rival goods. So it doesn’t cost you anything to. to offer another version and just give it away and bundle it with something else. You can offer a tremendous consumer surplus and customers are willing to pay more. So generally speaking in the world of digital, a bundle beats an a la carte offering. So Spotify beats iTunes. Cable packages win. You can bundle. a Mobike ride sharing service with ride hailing, let’s say under a subscription service, subscription is a type of bundle, and do dramatically better. And what you see now happening in China is you see these companies like Alibaba starting to offer VIP memberships, where if you sign up for their membership, you get a discount on movies, music streaming, buying goods, delivery and bike sharing. because Alibaba bought Hello Bike. So you get discounts on everything. So when you start to bundle these things together, now this is more of a physical service, but it’s kind of a digital product. You can start to do these things. There’s a lot of ability to do this. And it’s pretty powerful. One of the big challenges for like a guy like me who’s doing this as a subscription service is probably subscriptions online, whether it’s podcasting or whatever. will start to become bundled fairly quickly. So there’s this pattern of you break everything apart and then you re-bundle it. You break it apart and you re-bundle it. Anyways, so bundling’s powerful. It usually beats a la carte. The economics are great for the consumer. The economics are great for the seller. It usually can scare off new entrants fairly well. Microsoft used to bundle office, windows, all of that. If Alibaba is bundling bike sharing with movie streaming other sort of e-commerce, you know, how do you, you know, that’s going to scare off any standalone bike sharing company from entering this space. So it scares people off. It tends to work better when you’re doing sort of preference based goods like e-commerce or media. It doesn’t work as well in commodities and bike sharing is kind of a commodity service, but you don’t get everything in life. Subscriptions, that’s kind of a type of bundling. Even versioning, which I talked about in the last two episodes ago, versioning where you offer different versions of the same service, that can be a type of bundling. The economics tend to work the same. So anyways, that’s, I think, the two concepts for today. Think about greater ecosystems and think about bundling. And when you take a traditional business like renting a bike, physical, in the real world, and you start to bring in… the economics of digital, because now it’s a little bit of a smart bike, you can start to see a bigger effect on things like bundling. So that is the basic theory for today. Now let’s do the question for you. Okay, so the question for you is, what should OFO have done early 2018? They had enough cash. The market was sort of, you know, not collapsing, but consolidating. We have now seen at that point 2018, we definitely saw DD bikes and Blue Go Go as a competitor, a large competitor with this is just one offering. Mobike and Maytuan rumored to merge and then Alibaba and Hello Bike have partnered up. So you’ve seen the larger animals start to consolidate up and we’re still on our own as OFO. What should we have done? Like if you were CEO, you’re vice president or they call you. come on down, tell us what to do, give us your three minute pitch. What should you have done? And I will give you three options. Well, let me say four options. Four options. We have to partner with the lion ASAP. So whatever it takes, go down to Dee Dee, go down to Alibaba, kiss the ring. I’m mixing analogies here, you can’t really kiss a lion’s ring, but you get the point. Whatever it makes. Whatever it takes partner with the lion as soon as possible one because they could crush us if they wanted to But to be it’s obvious. We’re not competitive as a standalone company Because of bundling because of these greater ecosystems emerging because of just pure size and cash flow we’re not Viable or at least not competitive and maybe not viable as a standalone company. So number one do whatever it takes Number two, maybe if we’re not competitive, we have to start to avoid the competition. Look, we could do that. We go down there, they tell us to get lost. All right, then we have to avoid the competition. Go to the boonies, go to the fourth tier and fifth tier cities. Go out to the west of China. But if we can’t, we have to avoid them. So let’s go somewhere they aren’t. and try to get to cash flow positive as soon as humanly possible. And Carlsberg beer is my favorite example of that, which I, you know, I’ll cover them at some point in detail, but, you know, they, they basically lost in the beer market in China around 2002 and they closed up shop. And then a couple of years later, 2014, they came back and they went far to the West of China and they just avoided the competition and did great. So go to the boonies, avoid the competition, get to free cashflow positive as soon as possible. Number three, you have to sort of take on the management. Well, let’s skip that one. Let’s say number three, split the company. Okay, maybe you don’t want to maybe we have to break this company in half. Maybe the company does have serious problems. Maybe, you know, We have to keep fighting in Shanghai and Beijing, but maybe we need to split this company down the middle, sort of good company, bad company. Let’s take those regions where we think we can get to profitability, or we think we can get to sort of cashflow, and just break it up geographically, and split that off and run it as a separate company. Hello Bike did very, very well, even though no one talked about them. because they basically avoided the competition. They weren’t in Shanghai and Beijing, which is why people didn’t talk about them, but they were out in third tier cities just doing quite well and Alibaba ended up buying them. Let’s just do that. Let’s just take off half the company and go out into other regions and be that way. And then the other company may have to raise money on its own. It may just perpetually lose money. It may end up failing, but let’s, you know. Let’s try and split this between good company bad company. And then I guess the fourth one, which is not really a management recommendation, this would be an investor recommendation is to become an activist. You know, this is Carl Icahn. Come in at the board level and shake things up and fire people, try to take over the company, threaten to take over the company. He doesn’t actually take over companies very often, but he does. threaten proxy votes and things like that, which you can’t really do in China, but that would be kind of the other ideas, do an activist investor play, which is, so let’s say one, two, and three, those are really management options. Option four is more of an activist investor option. Okay, so of those, pick your favorite one. You should be able to vote, just click on the page there. And if you want, which I recommend is, write a three minute pitch to either the CEO or the board on what you’re going to do. And you know, keep it to three paragraphs. Think about it in terms of bundling. Think about it in terms of ecosystems. I give you really three ideas this time, ecosystems, bundling and money war. So think about it in terms of those and make your best shot like, you know, the more you can try and answer this question, what should OFO have done? the more this is going to be valuable to you. So that’s it. Please do it right now. Stop the podcast. Either write something really quick or just tap on the screen which one you would vote for. Okay, do that now. Alright, how’d you do? Did you really do it? I’m gonna keep pushing. I’m the official nag in your ear. That’s one of my roles here. Anyways, that’s it for today. I think this is a pretty interesting case. All of this bike sharing stuff, I thought it was, I’m not a VC guy at heart, I’m really not. I’m much more interested in this situation. I like, you know, I love studying great companies. I’m more interested in kind of great companies that have one or two problems. I like great horse bad jockey, where you can replace the management and suddenly you do well or two businesses where one of them is great and one of them kind of sucks and then you just split off the bad one. I like that kind of messy stuff because I think you can bring more to the table. Great companies are awesome to study but they don’t usually need much. If there’s a financial crisis, great, buy shares in great companies. But that’s a… That’s kind of a different strategy. Okay, anyways, that’s it for me. I’m heading back to China in a day and I’m gonna do my interview with Guo Ping, who is the CEO of Huawei, which I’m pretty excited about because I’m the first sort of, they call me an influencer. I don’t really like that term very much, but it’s better than thought leader. Both of those terms are kind of vain and I don’t know. I haven’t come up with a good term for whatever it is I do, but. I’m the first one of those that they’ve ever invited to come interview their senior management. So one of the cool things about not being a media person or a journalist or a, you know, let’s say a McKinsey or BCG or Bain type consultant is you can have more fun. So they said, okay, let’s do an interview. We’ll do it in a conference room or, you know, and I said, I don’t want to do that. Like that’s uninteresting. I said, I want to go to his favorite hot pot restaurant, or I want to go to a local bar, and I want to interview him over hot pot and or beer. And they came back and they said, okay. So apparently on Wednesday, I’m going to be interviewing the CEO of Huawei at a local hot pot restaurant, which is just more fun. It’s, you know, I used to be a management consultant and it’s so stuffy. You know. It’s so formal and you have to because it’s client service and I understand all that but it’s it’s so much more interesting when you can kind of be yourself and have fun. Anyway so that’s what we’re doing on Wednesday. If you have any suggestions for questions to ask now please email them to me or just put them in the comments for this this episode. It’s on jefftowson.com. You’ll find this where the where this podcast is located. There’s a comment section. Put them in there and we’ll see. It’s going to be about an hour. So it’ll be great. I’m really looking forward to that. And then it’s back to Bangkok for the end of the year. Oh, actually I’m going to, I’m going to Chongqing the next day with Jingdong to look at their new e-space. So they have this new mega shopping mall, 50,000 square meters with Apple and Samsung. And it’s their sort of experiential retail flagship. So I’m gonna go meet them and sort of go through that and get a sense of that. I’ve written a bit about that. but I want to dig into a lot more of that because I think when you get into online merge offline, especially in retail, it’s really, I mean, supermarkets are kind of interesting, but that’s just buying stuff for food. We don’t spend time in supermarkets for fun, but when you go to shopping malls or when you go to walking streets or department stores, there’s so many aspects of life that happen there, like entertainment, chatting with friends, just hanging out, just somewhere to go. So when you start to do OMO for that, there’s a lot of interesting stuff you can do. I mean, that kind of captures a lot of urban life. So I’ve been looking at that. So I’m kind of excited and we’ll see how that is. I went to Intime, which is the Alibaba department store a couple of weeks ago. So this is sort of the other one I’ve been keeping my eye on. So I’m gonna talk with Huawei on Wednesday, head out to Chongqing, which is a super fun city. If you’ve never been to Chongqing, that city is just the best. like the geography is crazy and you know it’s mountains and rivers it’s just so much fun and the foods phenomenal so that’s going to be thursday and then back to bangkok and that’s the end of the year so i’m pretty excited it’s going to be a great week anyways that’s it for me for today uh… thank you so much for uh… listening thank you so much for doing the assignment if you did the assignment uh… please subscribe if you have it you can go to jefftowson dot com or sign up at itunes I really do appreciate that. And apart from that, have a great week. Thank you for listening and I will talk to you next week.