Last week, Tencent announced its financial results for Q1 2026. These were pretty important. Because they gave us real details about their big moves in GenAI and Agents.

In this 4-article series, I’ll go into the details of Tencent’s revised approach to AI and Agents.

But first, let me go through the financials. I have 5 quick points here. In Part 2, I’ll get into the AI stuff (i.e., my area).

Point 1: Tencent’s Q1 Revenue Growth Was Solid and Diversified. Like Always.

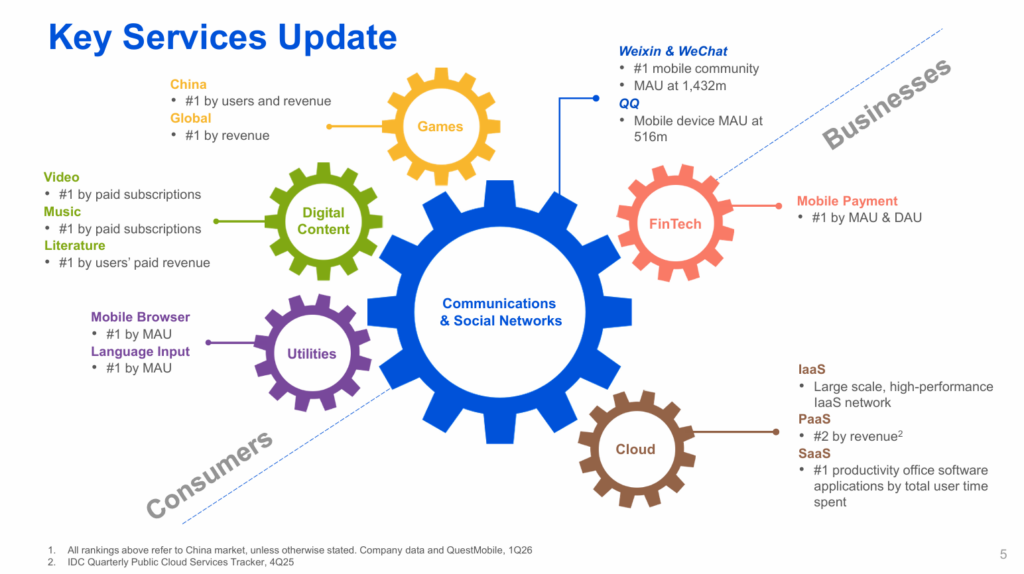

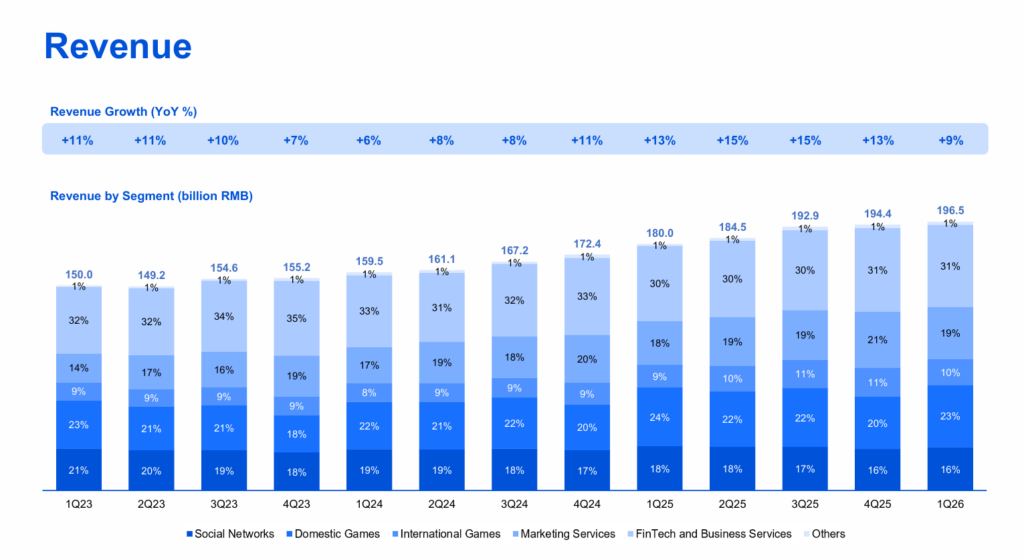

Tencent is a big, complicated business. And the businesses interact with each other. It’s one of the few real digital ecosystems. Here’s a slide from management’s earnings presentation summarizing its various interacting business.

For Q1 2026, Tencent’s revenue was 196B RMB ($28B USD). And most of that came from four revenue engines:

- Marketing services: 38B RMB

- Domestic games: 45B RMB

- Social networks: 32B RMB

- Fintech and business services: 60B RMB

Here’s the summary from management’s presentation.

You can see that the revenue is pretty evenly distributed across its businesses. And that it hasn’t changed. That’s my take-away here. We don’t see any major disruption in the top lines due to GenAI.

Q1 growth was solid at 9% YoY overall. That fits within Tencent’s recent 8% and 15% growth per year (since 2023).

Ok. So, we see big revenue with solid growth across a diversified digital ecosystem. That’s pretty much how Tencent always looks.

The key point is that the basic financial picture hasn’t changed. Despite all the big tech changes happening.

Let’s get to something more interesting.

Point 2: Marketing Services Showed a 20% Jump in Revenue. That’s Important.

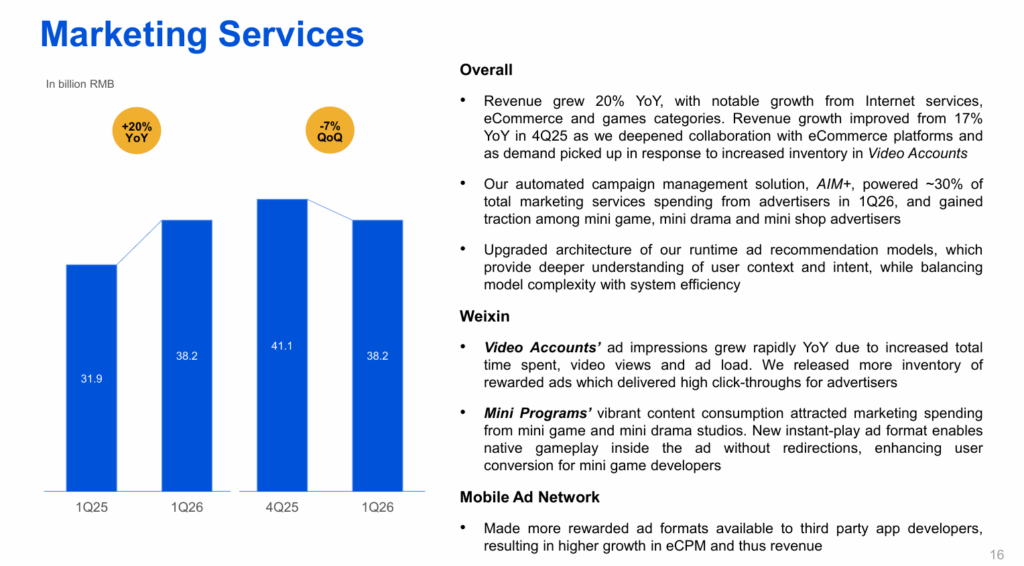

Tencent’s marketing services revenue grew 20% (yoy) to 38B RMB ($5.6B USD).

And this is the number I pay the most attention to. Tencent is an expert in marketing the same way Alibaba is an expert in ecommerce. Marketing cuts across most of their business activities, especially gaming, video and ecommerce. And marketing revenue for Tencent is like GMV for Alibaba.

Marketing is also something that GenAI can have a particularly big and fast impact on. GenAI is really good at content creation, personalization and increased conversions.

So where did the 20% revenue jump come from?

Management did comment on this. Here is a slide from their presentation.

Note the comment that Tencent’s Marketing Solution AIM+ “powered 30% of total marketing services spending from advertisers in 1Q26”.

AIM+ is Tencent’s automated ad campaign solution, which was launched in November 2025. It automates audience targeting, bidding, ad placements and creative optimization across the Tencent ecosystem. Basically, advertisers can set their high-level objectives and preferences and then the AI system handles execution and optimization.

I’m trying to dig more about AIM+. It’s still evolving but looks like a multi-agent orchestration system. I think it will be a multi-agent system that coordinates specialized AI modules to deliver full-cycle automation.

It’s really compelling as an idea. I’ve been waiting for agent systems in marketing within the ecosystem. But it’s hard to tell how important AIM+ was in the recent marketing revenue jump.

Management comments on this mentioned that:

- The marketing revenue jump was the result of an upgrade to the WeChat ecosystem traffic and ad models.

- There was also full deployment of the Tencent Marketing Solution conversion rate prediction task across Video Accounts, Official Accounts, Mini Programs, and Moments.

I’m trying to dig more into this area. “Marketing meeting AI” at Tencent is really important.

Point 3: Tencent Cloud Is Profitable, Growing Steadily and Going International

AI Cloud is usually where I look first for the enterprise adoption from GenAI tools. New GenAI tools are usually built by the cloud business. And businesses (especially smaller ones) typically start trying new GenAI products via cloud services (before building internally). And we can often see revenue bumps in cloud services pretty quickly with popular new AI services. That was definitely the case for Baidu Cloud and Alibaba Cloud.

Tencent Cloud is different. It is definitely a key area for GenAI and agents. But given the big Tencent ecosystem and their many, many products (especially gaming), we can actually find AI and Agent revenue and growth in lots of areas. Tencent is pretty unique in this regard. They have an almost uniquely large suite of digital products and services.

Tencent Cloud revenue is included in Fintech and Business Services, which grew 9% Q1 YoY. So solid growth.

I think the interesting story with Tencent Cloud has been:

- It achieved profitability in 2025. That was a big milestone.

- It has been going international pretty aggressively in the past year. Especially in Asia. Their tentpole project in Asia was the cloud migration of Indonesian giant GoTo onto their cloud services.

I broke down Tencent Cloud’s international push in previous articles.

- Get Ready. Tencent Cloud Is Going Global (1 of 2) (Tech Strategy)

- Tencent Cloud Goes Global. My Interview with VP Karl Xu. (2 of 2) (Tech Strategy)

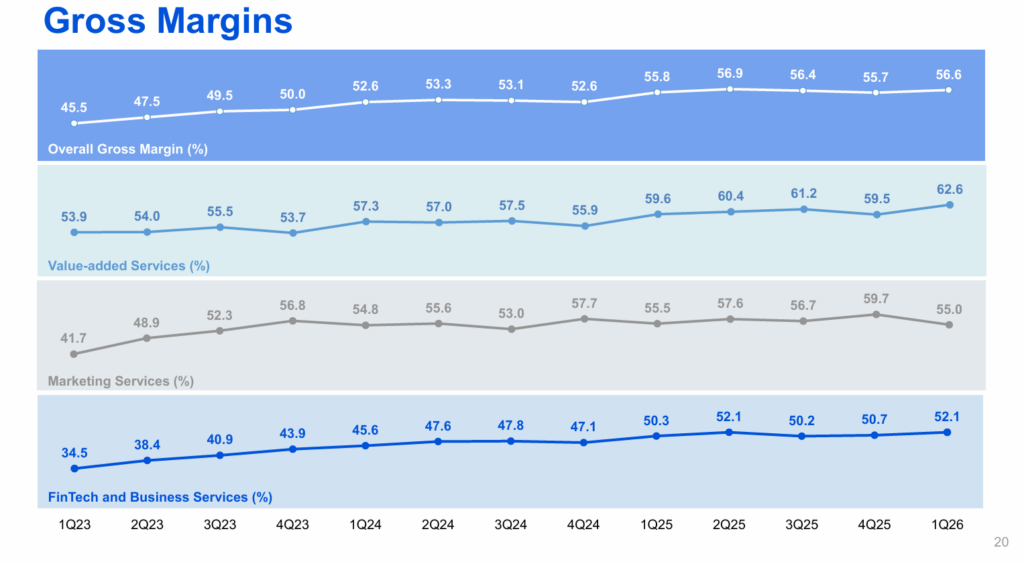

Point 4: Gross Margins Held Solid at 56%

Traditional software is good at standardized services (and connectivity), which has particularly great economics. There are big fixed costs which can be leveraged across lots of users. So you build a product one and then sell it over and over at very low marginal production costs. That means high gross margins, that often can increase with scale.

GenAI and agents, unfortunately, don’t have these super attractive economics. Intelligence (i.e., non-deterministic compute) have far greater variable costs. The more questions you ask an AI to run through its compute, the higher the costs. And this can vary significantly product by product.

So, we don’t really know what the gross margins are going to be for most of these GenAI services (yet). They do have significant variable costs.

And this problem is growing as the capabilities develop and with scale. And it is definitely a problem with agents, which use dramatically more compute than humans. Humans use GenAI episodically. We ask some questions here and there. Agents can run continuously. And while there are 8B humans, there could be 800B agents.

So Tencent has been deploying GenAI into its products and services, with rapidly advancing capabilities. And now they are really pushing into agents. But we still don’t know the ultimate cost structure (and therefore gross margins) for most of them.

But the gross margins at Tencent were pretty solid in Q1 2026. Gross margins were 56%. Which is consistent for Tencent overall. I don’t see any big changes for individual business units either.

See the released summary below.

Last Point (5): Tencent’s GenAI and Agent Push Definitely Showed Up in the Operating Profits.

Tencent’s big push into GenAI and Agents hasn’t shown up in the gross margins (yet). But it is definitely in the operating profits.

Tencent’s revenue and operating profits both grew 9% YoY. And operating profit remained stable at 38% of revenue.

But if you exclude the big new AI products (which they did in their released income statement), the operating profits growth would have been 17% YoY. And the operating profit would have been 43%, not 38%. See below.

The excluded new AI products were Hy, Yuanbao, CodeBuddy, WorkBuddy, and QClaw. I’ll go through these in detail in Parts 2 and 3.

There is definitely big spending happening in AI and Agents.

- R&D jumped 19% YoY.

- S&M jumped 44% YoY.

- Capex, which was 31B RMB (Q1 2026) grew 18% YoY.

But honestly, those numbers seem pretty conservative to me.

Look at what OpenAI, Grok and others are spending on this. They are flooding money into models and data centers. And many are doing big capital raises at ridiculous valuations.

In comparison, Tencent appears pretty prudent. Their operating profit took a moderate hit. But you can’t see much else in these numbers.

On the earnings call, management made some comments about this. They said they are going to increase AI-related capex. But that the KPIs for this will be both revenue and marketshare. So they are not going for margins and profits on this. Which is expected. But they are also not just going to marketshare at any cost.

When asked specifically about how AI will impact Tencent’s domestic gaming, they mentioned content production will become faster and that incremental revenue growth is one of the goals.

I really like that approach.

There is big spending on AI and agents and an aggressive push to put these tools into their products (both new and existing). But with a focus on both marketshare (i.e., adoption) and incremental revenue.

They are not going for marketshare and adoption at any cost. That’s explains the financials for me.

***

Ok. That’s it for a quick look at the financials. Note: I mostly do tech analysis, not financials. So let me get into that in Part 2.

-Jeff

Note: This article is not investment advice. The information and opinions may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.

——

Related articles:

- More High-Tech Flex by Huawei R&D (4 of 4) (Tech Strategy)

- 6 Big Events in AI Agentic Ecommerce (Tech Strategy)

From the Concept Library, concepts for this article are:

- Financials

From the Company Library, companies for this article are:

- Tencent

——

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.