In the past 3-4 months, Sea Limited stock price has fallen from $350 to $90 per share. That is interesting.

The business model is as formidable as ever. It benefits from compelling long-term consumer spending growth trends in both SE Asia and Latin America. And, unlike Alibaba, Sea Limited is in +9 countries and is politically diversified.

So, what’s going on with the stock price?

I think it’s all about growth.

- There are concerns that Garena’s growth is decelerating.

- The growth in Latin America and other distant markets is unclear.

- There are concerns that management is spending more on growth than it can fund from internal operations, meaning capital raises and dilution.

There is just a big question about the rate, quality, and cost of Sea’s various growth initiatives.

And this is really about CEO Forest Li and trying to figure out his intentions. He is a growth-focused leader. He is playing the long game and sacrificing near-term position and profitability, which I like. But he is also increasingly ambitious in Sea’s growth-focused initiatives, which concerns me. You can see the progression.

- Sea expanded Garena across SE Asia and Taiwan.

- Sea jumped from gaming into ecommerce (in SE Asia).

- Sea jumped from being a game publisher to being a game developer (i.e., Free Fire).

- Sea jumped into payment, credit, and maybe financial services in SE Asia.

- Sea acquired a Hong Kong vehicle for doing investments and acquisitions.

- Sea expanded into Latin America in ecommerce.

How do we assess the rate, quality, and cost of Sea’s various growth initiatives? I think we can ask three questions:

- How are the growth initiatives different in terms of increasing economic value?

- What is the rate of economic growth vs. cost? Keep in mind, growth often destroys economic value.

- What is the probability of success?

- How are the growth initiatives different in terms of users, engagement, and retention?

- Sea is a digital company. Users and engagement are the core assets. There can be lots of value in acquiring these assets, beyond just operating cash flow.

- How are the growth initiatives different in terms of strengthening the business model?

- Does an initiative lead to a winner-take-all or winner-take-most model that can later be monetized?

Recall, Core vs. Adjacency Growth

Lat year, I did a podcast on the various types of growth.

This was largely a summary of the thinking of Bain’s Chris Zook, which I find pretty useful. His books Profit from the Core and Beyond the Core are quite good for traditional businesses. His approach is focused on achieving sustainable growth that creates economic value.

Here is the framework.

- Companies with sustainable growth have 1-2 strong cores. These profitable cores have:

- Loyal customers

- Competitive advantage

- Unique skills

- An ability to earn profits

- Note: This is Garena in SE Asia already. And it should be Shopee in SE Asia, in the near future.

- However, core engines need to continually adapt. They cannot be stagnant. Sustainability means continually adapting the core. That can be by:

- New products / services

- New customers, including microsegments

- New geographies

- New businesses

If you look at Sea in SE Asia and Taiwan, you can see 2 strong cores that are well positioned to adapt going forward. And there is also a good secular growth trend of SE Asian in consumer spending growth.

Chris Zoom also talks about growth adjacencies. Core engines can fade or be disrupted so you also want to continually test for growth paths that are not too far from a core. These can include:

- New customer segments

- Micro-segmentation of current segments

- Unpenetrated segments

- New segments

- New geographies

- Global expansion

- Local expansion

- New channels

- Internet

- Distribution

- Indirect

- New products

- New to world

- Complements

- Support services

- Next generation

- Just new products / services

- New businesses

- New to world needs

- New substitutes

- New models

- Capability adjacencies

- New value chain steps

- Forward integration

- Backwards integration

- Sell capability to outside

The expansion into Latin America could be considered a global expansion. The expansion into payment is a capability adjacency. The expansion into game publishing with Free Fire is backwards integration.

Ok. That’s a decent framework. And I think these are the growth questions that are giving people concerns about Sea. So how can we rate Sea’s adjacency moves?

3 Factors to Assess Sea’s Adjacency Moves

Here are three success factors from Chris on this:

- Factor 1: Adjacency needs to be tightly tied to a strong core.

- The economic distance should be short. How much does the adjacency overlap with a core?

- You need a strong core or a strong position in a channel, customer segment or product line in a weaker core.

- You need to really understand the linkage. Often, the linkage is considered superficially.

- For example, Snapple is close to Gatorade so shouldn’t that have worked? But it turns out production is totally different. So were the customers and advertising. And the points of purchase and distribution.

- Factor 2: The adjacency needs to be attractive in terms of profit pools.

- Factor 3: The company needs the ability to capture economic leadership in the adjacent market.

- You need to think about competitive advantage as an attacker and then as an incumbent.

We can assess Sea’s growth moves with these three factors. Recall my list from the beginning of this article.

- Sea expanded Garena across SE Asia and Taiwan.

- This could just be considered adapting a core. Or as an adjacency, in which case it nicely fits factors 1-3.

- Sea jumped from gaming into ecommerce (in SE Asia).

- This was the big adjacency move. But it also fits 1-3. Their gaming customers were a real asset for jumping into ecommerce (factor 1). And a marketplace platform is a very attractive business (factor 2). The bit question was factor #3. Could Sea take economic leadership when competing against incumbent Lazada? In retrospect it is clear that Lazada was weaker than most people thought.

- Sea jumped from being a game publisher to being a game developer (i.e., Free Fire).

- Again, a strong yes to all 3 factors. Sea leveraged its gaming customer base and distribution in SE Asia (factor 1). It targeted an attractive market (factor 2), which was the global market for games like PUBG and others. And it achieved economic leadership (factor 3).

- Sea jumped into payment, credit, and maybe financial services in SE Asia.

- This is unclear to me. It’s definitely factors 1 and 2. But it’s unclear if Sea can win in this space. There are lots of established and new players in digital finance.

- Sea acquired a Hong Kong vehicle for doing investments and acquisitions.

- Another copy of Tencent and Alibaba.

- Sea expanded into Latin America in ecommerce.

- This is really the biggest question. It’s a yes to Factor 2 but not too much for Factors 1 and 3.

- Factor 1: Shopee and Garena have no real linkages in Latin America. However, Free Fire has lots of players in Brazil. So there is a user base. But I think the linkage is much weaker than with their previous moves.

- Factor 3: Entering Latin American ecommerce means taking on Mercado Libre and Amazon. They are well-established in Latin America and are well-run. Plus, they have been building infrastructure for a decade. This is going to be an expensive fight. Mercado Libre, in particular, will respond strongly to any loss of market share. Expect them to ramp up marketing and infrastructure spending in response. This is likely value destructive in the near term for Sea (like in SE Asia with Shopee). The question is will this growth be value creative in the long-term?

An Aside: Why Alibaba Didn’t Enter Latin America

So, Sea jumped from SE Asia to Latin America. Ok. But why didn’t Alibaba or JD do this? They certainly could have. They have far more money and could have entered years ago.

I once asked Alibaba President Michael Evans how they assessed international markets for expansion. His answer, which I am paraphrasing, was they don’t focus on market size or opportunity. They focus on where they have advantages. That is pretty much Factor 1 and 2.

Alibaba management has often said there is no clear path for them to capture foreign consumers. There is nothing about their China current business that gives them an advantage in acquiring consumers in places like Italy or Brazil. They could certainly spend the money (which they have) but they focus on where they have advantages. And since they don’t have one in this case, their approach has been to do opportunistic M&A. They have never launched themselves in places like Mexico or India. But they do invest and do acquisitions if they spot an opportunity. For example, they bought Lazada.

***

Ok. Here are my conclusions for the question of Sea’s growth.

Conclusion 1: I Love Sea’s SE Asia Growth Story

I really like Sea’s SE Asia (plus Taiwan) business. It is a fantastic business model and has a solid growth story. It has all the factors above and positions them well for lots of adjacency growth.

And recall, I said there can be other types of value in growth.

- How are the growth initiatives different in terms of increasing economic value?

- What is the rate of economic growth vs. cost? Keep in mind, growth often destroys economic value.

- What is the probability of success?

- How are the growth initiatives different in terms of users, engagement, and retention?

- Sea is a digital company. Users and engagement are the core assets. There can be lots of value in acquiring these assets, beyond just operating cash flow.

- How are the growth initiatives different in terms of strengthening the business model?

- Does an initiative lead to a winner-take-all or winner-take-most model that can later be monetized?

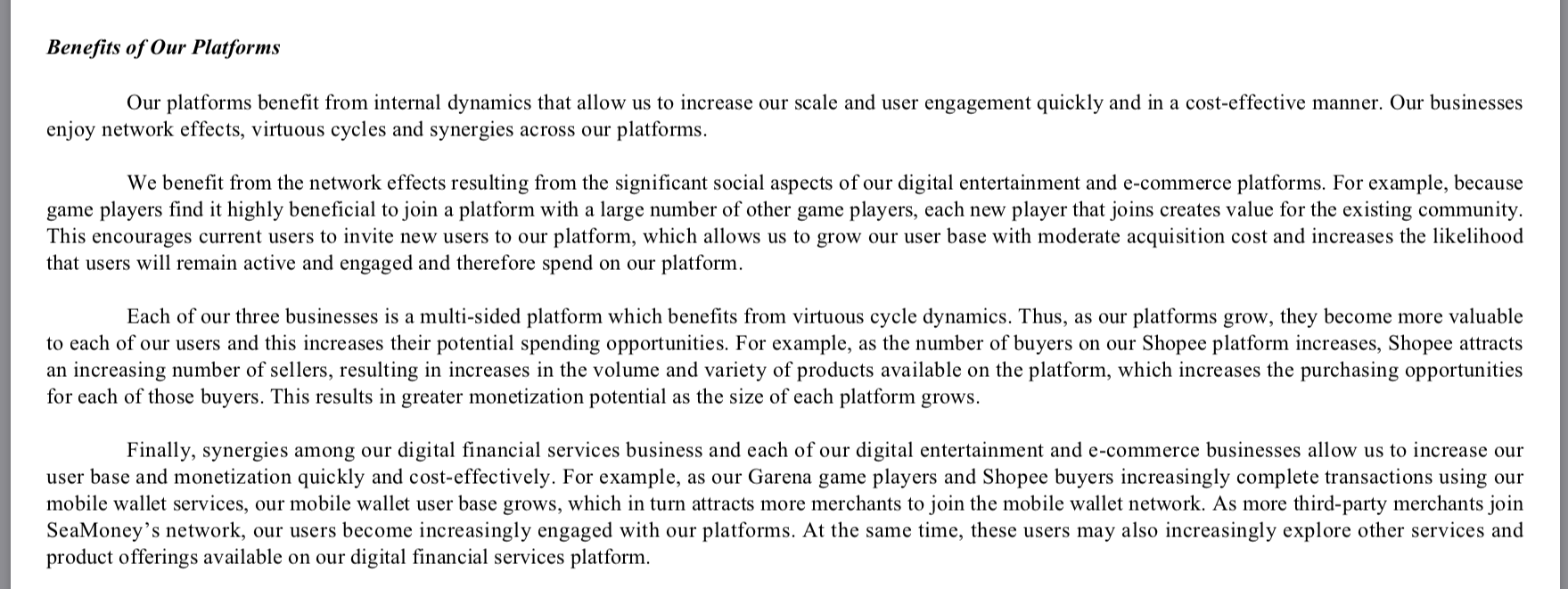

Sea’s SE Asia story really speaks to all three of these questions. Here is how Sea describes the benefits of growth in their 2020 10-k.

These four paragraphs are a good summary of what Sea has been doing in SE Asia. This is some good strategy thinking. If you really want to understand how Sea benefits from growth, just read these four paragraphs over and over. Here’s my summary:

- Paragraph 1 is good breakdown of complementary platforms.

- They are trying to grow user numbers and engagement.

- This results in increasing benefits (economic and competitive) of scale. This includes network effects

- They can also exploit synergies.

- Paragraphs 2-3 lays out the three platform business models they are building. Each business benefits from network effects.

- An audience-builder platform. Garena benefits from being an innovation platform between players and game developers. But it also benefits from the social aspect, as they focus on multiplayer games. So, it has a direct and indirect network effect.

- A marketplace platform, which is Shopee. Note they are increasing the social aspects of Shopee as well.

- A payment platform with credit. This might be disrupted.

- Paragraph 4 is about how multiple platforms can be complementary. They cross-sell their users. They launch new products and services. And so on.

So how is this growth playing out?

Pre-Covid, we were seeing the numbers moving as we expect in Garena.

- User number and engagement was growing steadily.

- Revenue was growing.

- Gross margins were expanding. This is important.

- Fixed costs were decreasing. These are now combined with Shopee, but we saw these numbers going down prior to the launch of Shopee.

That is exactly what we want to see with a growing core.

Shopee is still earlier in its lifecycle.

- User number and engagement were growing rapidly.

- Revenue was growing rapidly.

- Gross margins were still negative but improving.

So I like the business model and I like the growth story of Sea in SE Asia and Taiwan. It is the growth of complementary platforms that all support each other.

Conclusion 2: Sea’s Play for Latin America Is Going to Be Really Expensive. And Could Fail.

For Sea in Latin America, there is Free Fire. But there is no gaming platform to build upon. There is no complementary platform. And there are dominant incumbents with tons of capital. This going to be a very expensive fight and Sea doesn’t have many advantages.

I don’t like any of that.

However, building a successful marketplace platform in a big market might be worth it. Sea has gone into a difficult and expensive fight. But at least, Sea is going after a big, big prize. A stand-alone marketplace is not as good as complementary platforms. But it’s still a fantastic business.

I don’t know if Sea will succeed. But I’m convinced it’s going to be a very expensive fight.

Conclusion 3: Sea’s Move into Game Development with Free Fire Was Fantastic

A vertical move from game publishing to targeted game development was a great adjacency move. It leveraged all their advantages in SE Asia. And it got them something none of their other businesses offered, access to a global market.

Like Tencent, Sea is in a good position to develop and acquire games. I would like them to do much of more of this, using SE Asia as the launching pad.

***

Ok. That’s my take. It’s an interesting company to look at right now.

Cheers from Sao Paulo, jeff

——–

Related articles:

- Growth, ROIC / RONIC and Growth + Sales in Digital Valuation (Asia Tech Strategy – Podcast 102)

- An Intro to Growth and “Birds in the Bush” in Digital Valuation (Asia Tech Strategy – Daily Lesson / Update)

From the Concept Library, concepts for this article are:

- Growth: Core vs. Adjacency

From the Company Library, companies for this article are:

- Sea Limited / Shopee / Garena

Photo by Sea Media Library

—–

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.

Stefan Conquist

March 20, 2022 at 4:02amJeff, thanks. You have previously observed that a big reason for SEA’s success over Lazada in SE Asia has been their ability to localize so well (better jockey”). And Shopee so far has apparently been able to succeed despite not having Lazada’s “faster horse” infrastructure advantage. During your visit to Brazil have you seen any evidence that they can pull this off in LATAM where MELI is the faster horse but with a proven jockey? When you say it will be expensive, I presume it means paying big money to either create their own infrastructure or to buy fulfillment services. I don’t like this prospect either. However I think SEA’s management has shown themselves to be pretty capable and it’s hard to see how they wouldn’t have considered this. Although “considering it” and “pulling it off” are 2 different things. And the whole thing still depends on the crazy ongoing success of Free Fire and its ability to cross-engage users with Shopee. Amazing. I guess we’ll have to wait and see whether this is “the little engine that could” or whether it’s a runaway train.

jtowson

March 20, 2022 at 3:48pmGood point on Free Fire. I didn’t think about cross-selling there. That could help.

I just think it is a much harder and more expensive play. MELI and Amazon are going to respond. Especially MELI as it has no fall back market. They’ll ramp up their marketing spend. Infrastructure spend. Discounts. etc. They’ll aggressively defend.