Sea Limited is rocking and rolling. Jumping from gaming to ecommerce. Then to payment and financial services. And now to Mexico. There is a growing public consensus that the Sea management team is extraordinarily effective.

That’s cool. But it would have been much better to know that two years ago, when the stock was much cheaper.

So I went back to my notes on Sea from 2019 and looked for signs and indications of what was to come. How can you spot such a company early on?

I came up with 6 early indicators that Sea was something special. And that it was about to take off.

Indicator 1: Sea Had a Focused, Winning Strategy for Gaming (Localization + Immersive).

Reading Sea’s annual report for the first time, it was the strategy for gaming that really jumped out at me. They company had a very precise approach and was focused on the best single opportunity I know of in gaming.

Sea (Garena) was focused on the most immersive games. They specifically cited:

- Battle Royale games

- Multiplayer online battle arena

- Massive multiplayer online action games (MMOAG)

- Massive multiplayer online role-playing games (MMORPG)

- Sports games

These are the most immersive games and they have the most dedicated users. These players play more frequently. They play longer. And they spend more money in the games. These games also have lots of content sharing and social communications. Lots of voice and chat integrated. Plus there is game streaming and tournaments.

Sea was going for users, engagement, and data. It was a platform strategy. And they were explicitly avoiding casual games.

***

The other half of their gaming strategy was localization.

The problem with building platforms in gaming is you are highly dependent on the game developers. This is not a fragmented marketplace platform where the platform has most of the power (like Shopee). You need the popular titles, owned by the big developers. 80% of Garena’s revenue back then came from 5 games.

However, SE Asia, unlike the US and China, is an unusual geography. It is fragmented. To get to scale as a platform, you need the entire region. But that means winning in the Philippines, Thailand, Malaysia, Vietnam and so on. That means localizing the language, advertising, regulatory compliance, distribution and user experience.

This need for localization in SE Asia put Garena in a stronger position as a publisher and distributor. Electronic Arts might want to go direct in the US and Japan. But they would rather go through a partner for Myanmar and Malaysia. Garena can pitch itself to game companies as the platform that can localize gaming and experiences country-by-country across the whole region.

- For consumers, Garena provides “access to popular and engaging mobile and PC online games.”

- For game developers, it can “develop”, “curate” and “localize” games for each market.

A gaming platform that focuses on immersive experiences plus localization in SE Asia is just great strategy. That was a clear indication of management focus and ability. In my notes at the time, I circled their description of their gaming strategy and wrote “wow” on the side.

Indicator 2: Sea Signed an Important Strategic Partnership with Tencent.

As mentioned, gaming platforms are dependent on game developers and owners. Sea has some strengths and they do have exclusivity for most games (a sign of strength). They also developed Free Fire, which helps.

But game licenses are still also one of their biggest costs of revenue (a sign of weakness). They are still highly dependent on game developers and a small number of popular games.

Fortunately, Tencent has the same problem. And Tencent’s dominance of the Chinese gaming market makes them stronger than any game developer. Tencent is to gaming what Hollywood is to movies and television. And in 2018, Garena announced a strategic partnership with Tencent which got Garena a 5-year right of first refusal to publish Tencent’s mobile and PC games across Southeast Asia and Taiwan.

Again, wow.

That was a big deal. They piggybacked Tencent’s access to games.

How can any other gaming platform in SE Asia compete with Garena plus Tencent?

I think this was an early indicator of their deal-making abilities, which is an important skill for tech giants. Their continued growth over time is going to dependent on their ability to buy as well as build. Sea isn’t buying into companies every week (like Tencent and Alibaba), but they will do a lot more of that going forward. And that Tencent deal was a great start.

Note: Sea has recently acquired an investment firm in Hong Kong. And they have moved into Latin America.

Indicator 3: Sea Got Traction in Ecommerce in 2017.

Management’s most daring move was its jump from gaming into ecommerce. It took them out of their expertise in gaming and into the world of warehouses, delivery and small merchants. Note: Solving the problems of small rural merchants is a big part of doing ecommerce in SE Asia.

And this was a logical horizontal move. Sea’s strength was their capture of digital consumers across SE Asia. Most SE Asian ecommerce players were specific to one country at that time. There were Vietnam players. And Thailand players. And so on. Only a few companies had a regional footprint. Garena had a big user base, lots of engagement and data. And these were still the early days of ecommerce in SE Asia. So the jump to ecommerce was not as radical as it seems.

In retrospect, Sea may also have been aware of the management issues at ecommerce leader Lazada. Certain senior manager at Lazada had moved to Shopee early on.

While Shopee’s strategy for ecommerce is pretty standard, it is the execution that gets your attention. In the 2017 and 2018 financials, you can see the company starting to execute effectively.

Sea’s revenue for ecommerce (and other services) was:

- $17M in 2016

- $47M in 2017

- $270M in 2018

And the country-by-country breakdown (of total revenue) also looks really good:

For Taiwan:

- $109M in 2016

- $123M in 2017

- $218M in 2018

Thailand:

- $61M in 2016

- $133M in 2017

- $195M in 2018

Vietnam:

- $23M in 2016

- $98M in 2017

- $193M in 2018

Indonesia:

- $99M in 2016

- $24M in 2017

- $32M in 2018

I think the jump to $47M in regional ecommerce revenue in 2017 was the key indicator.

Indicator 4: Sea Really Hit the Accelerator for Ecommerce in 2018.

Take a close look at their financials for 2016 and 2017.

For 2016:

- Digital Entertainment Revenue: $328M

- Digital Entertainment Gross Profit: 44%

- Ecommerce and other Revenue: $18M

- Ecommerce and other Gross Profit: -260%

- Total Gross Profit: $113M

- Sales and Marketing Expense: 54% of Total Revenue

- Operating Income: -$205M

For 2017:

- Digital Entertainment Revenue: $365M

- Digital Entertainment Gross Profit: 41%

- Ecommerce and other Revenue: $47M

- Ecommerce and other Gross Profit: -227%

- Total Gross Profit: $87M

- Sales and Marketing Expense: 102% of Total Revenue

- Operating Income: -$502M

These numbers are really important.

- The gaming business is solid. Single digital growth in revenue and +40% gross profits.

- The ecommerce business is small but growing. The jump to $47M in revenue in 2017 was important.

- However, ecommerce has strongly negative gross profits. These are the early days of operating leverage.

- Sea really ramped up their sales and marketing spend in 2017 to grow their ecommerce business.

Overall, the new business was off the ground. Sea’s gross profits decreased a bit as a result. But they had cratered their operating income with the big marketing spend.

To me, this looks to me like a stable gaming business plus an option on a big ecommerce business. 2017 was the year to buy big into this company.

Now take a look at the next year.

For 2018:

- Digital Entertainment Revenue: $462M

- Digital Entertainment Gross Profit: 43%

- Ecommerce and other Revenue: $270M

- Ecommerce and other Gross Profit: -165%

- Total Gross Profit: $15M

- Sales and Marketing Expense: 85%

- Operating Income: -$989M

In 2018, their gaming and, more importantly, their ecommerce revenue takes off. The combined gross profit collapses. And they really put their foot on the gas for sales and marketing spend (mostly to acquire ecommerce users). Note: they didn’t really increase their R&D spending very much.

If 2017 was the year Shopee achieved product market fit, 2018 was the year it began to scale aggressively.

I think we will continue to see this financial picture. Rapid revenue growth but big spending in IT, logistics and sales and marketing. One day Sea will switch their focus from growth to profits. Until then, their profitability and true operating leverage will be hidden under all that growth spending.

Indicator 5: Sea Management Was Starting to “Explore and Exploit”.

Thomas Russo, one of my favorite investors, likes to invest in companies that show a “capacity to suffer”. And he looks for this in both the management and the major investors. Both need to be willing to take pain now for a much bigger gain later.

The above financials are a textbook example of a capacity to suffer. Sea’s management took fairly attractive financials in 2015 and cratered them with a big strategic and financial move into ecommerce. Very few CEOs and boards have the courage to do that. You ruin the financials of Coca-Cola and you will likely get fired. And for good reason. Most new initiatives fail. And most management teams aren’t good enough to pull it off.

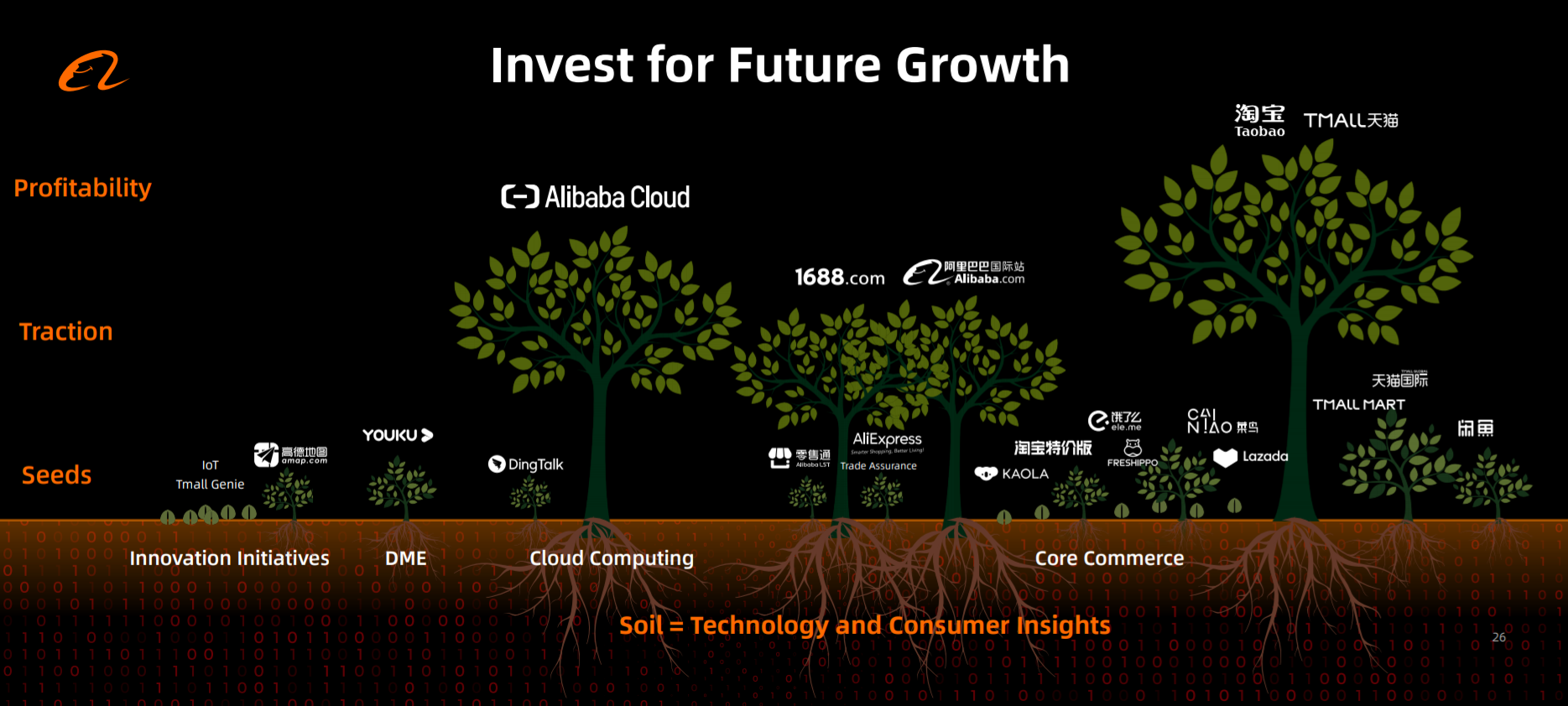

What you see at Sea in 2016-2018 is a Jeff Bezos-style “explore and exploit” approach to management. They made a move into ecommerce over 1-2 years. But they didn’t really hit the gas until they had product-market-fit and growing adoption. Alibaba does the same explore and exploit approach. The digital world moves quickly so leading companies are always exploring and testing new ideas. And then they exploit and grow the winners. Note the below chart of the various initiatives Alibaba is exploring.

Certain businesses, like Amazon, Alibaba, Meituan and Tencent, are very good at this. Others, like Airbnb and Facebook, are really weak at this.

Indicator 6: Sea Was Playing to Win Big.

Ok. My last point.

I’m a strategy guy. And one of the first thing I noticed about Sea was that they were building three complementary platforms. One in gaming. One in ecommerce. And one in payment. Each would be very attractive in its own right. In fact, gaming, marketplaces and payment platforms are among by favorite business models.

- They all have strong network effects and competitive strengths.

- They all have attractive unit economics. Note: Both Garena and Shopee have strong negative working capital (most everything is prepaid), which I always like. That’s very different than say advertising-based businesses.

But when you put these platforms together, they strengthen each other. They are complementary. They can share users, marketing, data, IT resources, and capital. They can cross-sell. They can bundle (yes!!). The most powerful digital companies (Tencent, Alibaba, Amazon, Google) are complementary platforms. Although they are often called ecosystems.

That strategy put Sea right at the very top of my pyramid for competitive strength and defensibility. I call companies at the top of the pyramid “competitive fortresses”.

Now Sea may not succeed at this this. But it was an early indication that Sea was playing to win. They were going for Boardwalk and Park Place. They may fail. But they are aiming for the biggest prize.

***

That’s my take. I think it’s a really important question. How can you spot a company like this early on? Before most everyone else? Any thoughts would be appreciated.

Cheers from California,

jeff

—–——–

Related articles:

- Can Shopee / Garena Beat Lazada? Tencent vs. Alibaba In SE Asia. (Jeff’s Asia Tech Class – Podcast 29)

- 4 Strategy Lessons from the Spectacular Rise of Sea / Shopee / Garena (Jeff’s Asia Tech Class – Daily Update)

- Lazada vs. Shopee is Faster Horse vs. Better Jockey (Jeff’s Asia Tech Class – Daily Lesson / Update)

From the Company Library, companies for this article are:

- Sea Limited / Garena / Shopee / AirPay

Relevant Concepts:

- Competitive Fortress: Complementary Platforms.

Photo by Japheth Mast on Unsplash

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.