For the past five years, I’ve been watching Alibaba pull farther and farther ahead of Amazon in its consumer offerings.

- Alibaba’s ecommerce products have integrated with entertainment, especially live-streaming (which is fantastic).

- Payment, credit and wealth management products were built upon Alipay.

- Ecommerce services, like food delivery and hotels, have been added with ele.me

- Social is being somewhat added with DingTalk.

- And, of course, physical retail is being integrated, with a surge of creativity in supermarkets, hypermarkets, department stores and other formats.

You compare all of that with Amazon and it’s pretty shocking. Why is Amazon so stagnant on the consumer side? I went into Amazon in my latest podcast:

But I thought I should take apart why I still really like Amazon. Even as a non-innovator on the consumer side.

An Introduction to Amazon’s Strategy

Amazon is a pretty easy business to understand in terms of strategy. There is a world of complexity in its operating details (especially the logistics and supply chain), but the business model is pretty simple. Using my terminology, it is 3-4 linked businesses. And that puts it at the top of my 6 levels.

There is:

- Its ecommerce business, which has both a linear retail model and a marketplace. And most of the interesting cost structures and operations are as a retailer – including its cost of goods sold, delivery costs and inventory management. It’s similar to JD in its control of its operations end-to-end (especially the consumer experience).

- A video streaming service. Another linear business model.

- AWS, its cloud business which is also a combination of a linear business model and a platform business model. Cloud services as platforms can be a combination of a coordination, collaboration, and standardization platform and an innovation platform.

- Logistics, although it’s not clear to me how much of a separate business this is going to be. It could be similar to JD Logistics.

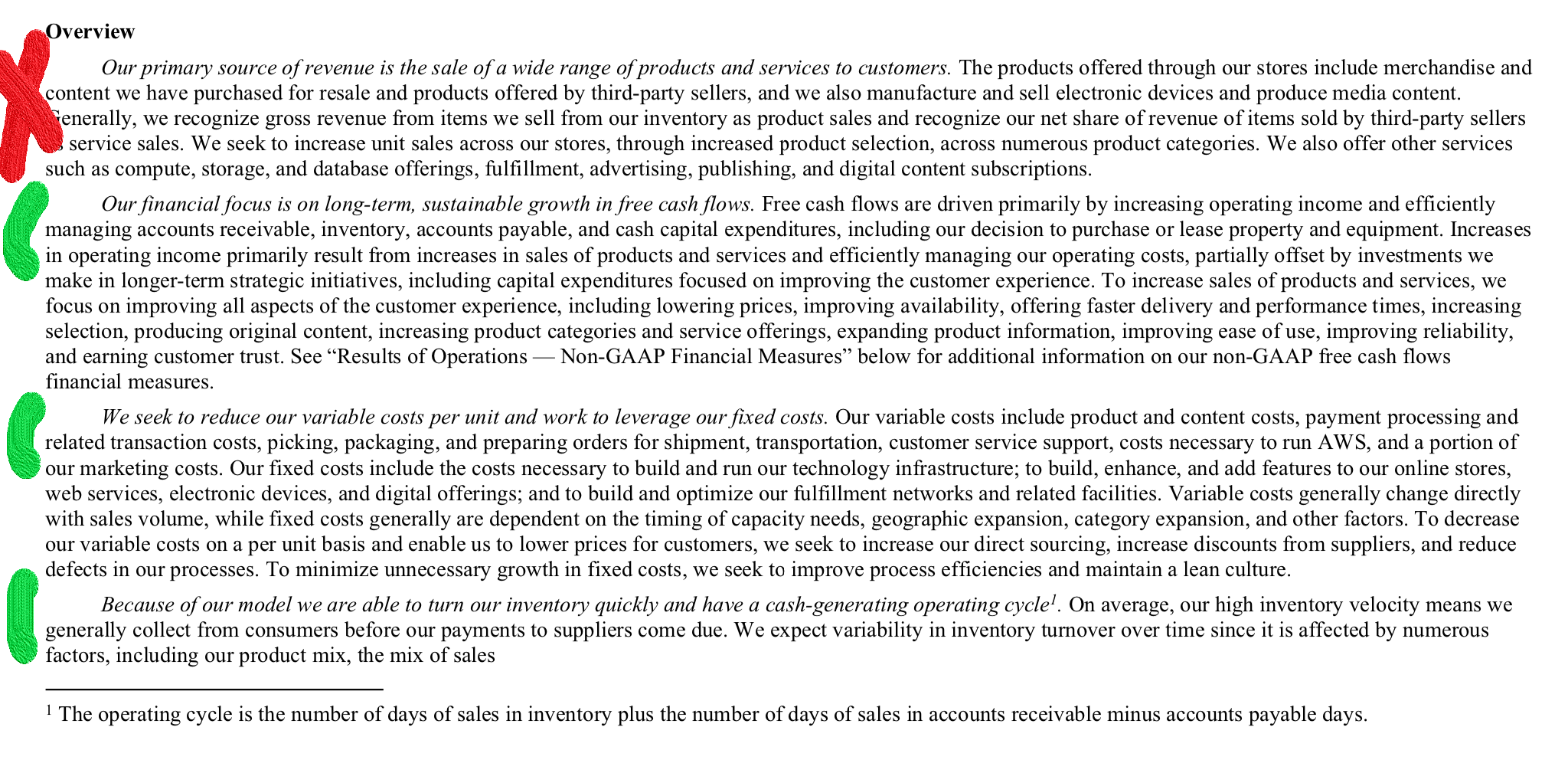

Going through the Amazon filings, what jumps out is how badly they explain their strategy. Read the first paragraph below (the red x) from their 10-k. This is the overview of the company.

That first paragraph is like the worst strategy summary ever. They sell a “wide range of products and services to customers”. Well, that’s vague.

And then they just list all the products and services of their 3-4 businesses together. They call themselves “earth’s most customer-centric company”. But then they list 7 customer groups, which are really user groups on platforms. It’s really terrible.

However…

Now read the next paragraph (marked in green). That is a really great summary of how Amazon creates economic value over time. It lays it out clearly.

The focus is on “long-term sustainable growth in free cash flows.”. That management’s bottom line, which is great. They accomplish this by:

- “increasing operating income”

- “efficiently managing accounts receivable, inventory, accounts payable, and cash capital expenditures”

- which is “partially offset by investments we make in long-term strategic initiatives, including capital expenditures focused on improving the customer experience.”

That’s exactly how they are increasing economic value over time. In the They go into this further in the final two paragraphs:

- They “seek to reduce our variable costs per unit and work to leverage our fixed costs”.

- This is basically straight out of my playbook for competitive advantages. They are focused on the reducing their strengths in variable and fixed costs.

- “we are able to turn our inventory quickly and have a cash-generating operating cycle.”

- I’ve mentioned in podcasts that I like marketplace platforms because they have negative working capital, which is the case for Amazon. It makes growth cheap.

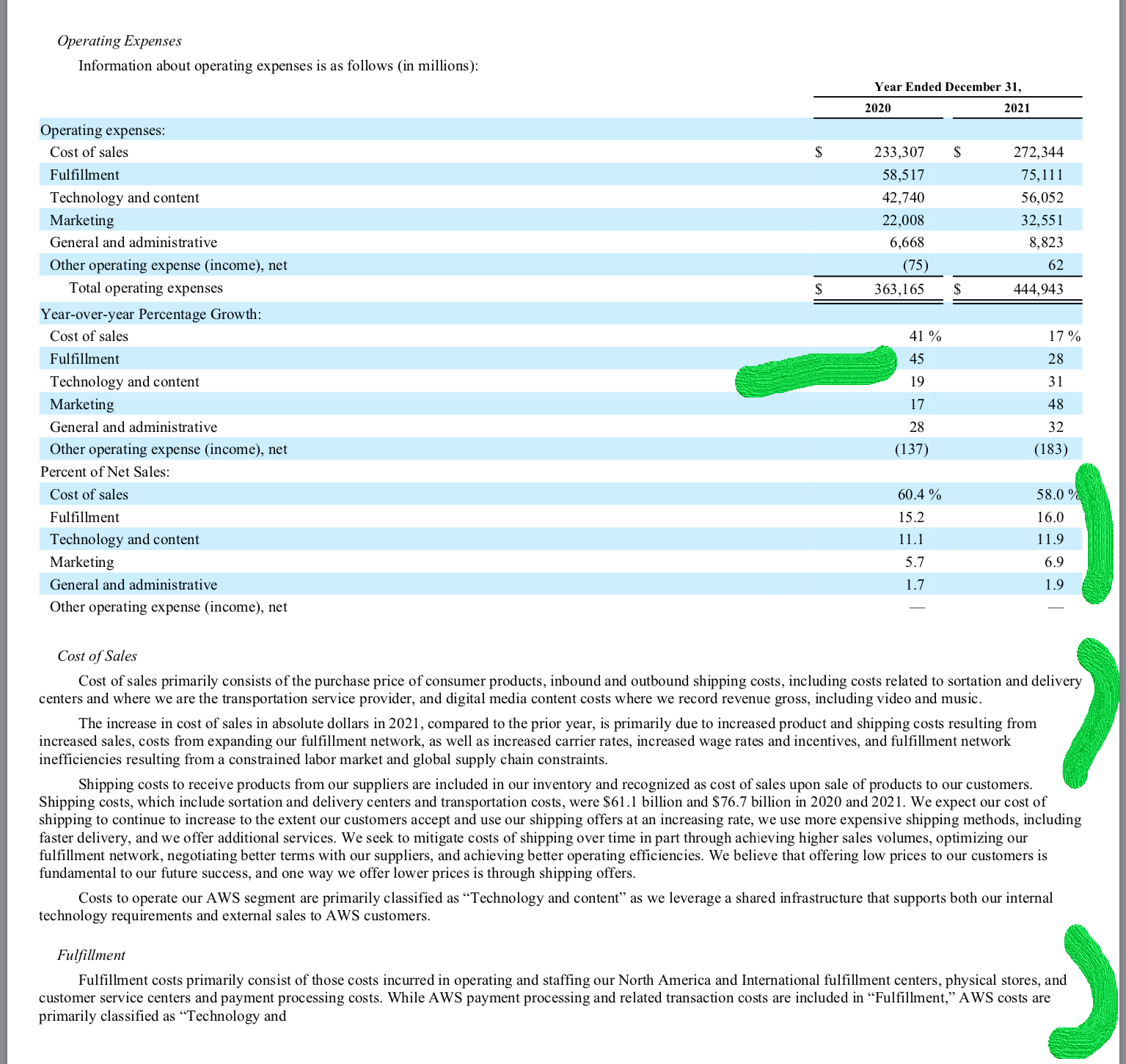

Overall, that is a really detailed and convincing financial plan. It’s like something written by an equity analyst. It’s not exactly inspiring but you can absolutely see it playing out in their financials. Note below list of Amazon’s major costs, which are cost of sales (including delivery and purchased content), fulfillment and tech (and created content). They are big numbers.

Finally, note the net sales:

These sales numbers are a confusing mix of retail sales and third-party sales. Plus, its AWS and digital goods as well. But it’s just worth noting the size overall. And the growth rate (+18% in North America).

Ok, fine.

But getting to my main point of Amazon’s lack of innovation on the consumer side. Which brings me to “jobs to be done”.

Recall, Clayton Christenson’s “Jobs to Be Done” Theory

About 100 podcasts ago, I talked about Harvard Business Professor Clayton Christenson and his theory of “jobs to be done”. It’s in the Concept Library but I haven’t talked about it in a long time.

Harvard Business School professor Theodore Levitt once said, “People don’t want to buy a quarter-inch drill. They want a quarter-inch hole!”. It was a clever way of saying that product categories and consumer demographics are a bad way to think about customers. Customers think in terms of problems to be solved.

Clayton Christensen better summarized this in his “Jobs to Be Done” theory. He put it forward as a framework for better understanding customer behavior, saying “people don’t simply buy products or services, they ‘hire’ them to make progress in specific circumstances.” It thinks about products in terms of “functional, social, and emotional dimensions” of the customers.

It’s a good question to ask about a business. For example, what is the “job to be done” for Amazon’s ecommerce business?

The answer is Amazon is where consumers can easily go to get everything they need – at a good price. Hence, it’s title as the “everything store”. And when Amazon discusses it consumer value proposition it always mentions the same three things:

- A wide range of products

- Value (i.e., cheap)

- Convenience and ease of use. Which means fast and usually free delivery, good customer service and universal availability (smartphone, pc, Alexa devices, etc.).

It’s the Walmart model, with a larger spectrum of goods but no stores.

However, Alibaba moved beyond this “job to be done” over ten years ago. The company is continually experimenting with consumer use cases, especially in their increasing footprint of physical retail locations. They are adding all sorts of live-streaming and short videos. They have shopping festivals every month. They have moved from transactions to shopping experiences and entertainment.

Looking at the video service of Amazon is equally unimpressive.

I once heard Ben Thompson describe the typical TV cable package as 5-6 different jobs to be done. And they have slowly been separated out into different businesses. They are:

- Story-telling. Human beings like stories. We watch tv shows and movies for this reason. That’s what a lot of tv is about.

- Mindless “vegging out” in front of a screen. This is also tv shows but it’s not about the story-telling. It’s more just mindless entertainment you can stare. Or watch while you clean the apartment.

- Education. We like to learn things. Lots of tv shows were about education.

- Sports

- News, current events, and other basic information like the weather.

I think we can view Amazon video (and Netflix) as 30% about story-telling. And 70% about mindless, vegging out entertainment. I think this is why most of the shows on Netflix are terrible. And while Amazon has documentaries, I don’t think it’s that much about education. YouTube, in contrast, is where you can learn how to do anything. Plus it’s a product for mindless and news, but not story-telling.

Final Point: Why I Still Like Amazon’s Ecommerce Business, Despite the Crap Consumer Experience

So, Amazon is pretty impressive in terms of its business model. It’s a linked business model, with two particularly attractive businesses. The company is also particularly innovative on the logistics and infrastructure side. But it is pretty much a non-innovator in terms of the consumer experience.

So why do I like it? And ecommerce, in particular, so much?

Because I am mostly looking for 3 things:

- A long-term secular growth trend with a stable minimum floor for demand.

- A strong business model with moats that captures this trend.

- Minimal risk of significant change in consumer behavior, technology, or regulations.

And if we look at Amazon’s 3-4 link businesses, does the lack of consumer innovation really affect this?

Nope.

What about the ecommerce business (for consumers)?

- What is the job to be done?

- We know the job to be done (discussed above). It’s still mostly the Walmart model.

- Is there a tailwind (a secular growth trend) for demand?

- Yes. Every year, there are more American families and they rise in wealth. The GDP per capita steadily increases in the US (unlike most countries). Since Amazon’s founding in 1994, the GDP per capita of the USA has doubled. And the population has grown from 263M to 334M people. The spending of American (and Chinese) middle class families is my favorite long-term tailwind.

- There is also a shorter-term tailwind which is the movement of physical retail online. This has been significant for about 20 years.

- Is there also a demand floor in activity, revenue per transactions and overall transaction revenue?

- Yes. Physical goods can’t really fall in cost below a certain point. Families need milk and bread no matter what. There is a nice solid floor for demand.

What about for the video streaming business?

- What is the job to be done?

- As mentioned, it’s story-telling plus mindless entertainment.

- Is there a tailwind for demand?

- No. In terms of activity, there are only 24 hours in a day. So, yes there are more Americans every year, but the overall activity is not steadily increasing.

- It is also probably not increasing in terms of revenue per activity. Streaming has made video much cheaper than cable. YouTube and other services are free. While activity may be stable, revenue per activity has been decreasing.

- You could argue there is a short-term tailwind for cable cutting, which moves more demand to streaming. But I think that is driving activity more than revenue.

- Is there also a demand floor in activity, revenue per transactions and overall transaction revenue?

- No. There are too many substitutes for this job to be done. Yes, video (and music) are more stable than things like live-streaming and short video. But this consumer behavior and technology changes in this area all the time.

What about for cloud storage and services (for enterprise)?

- What is the job to be done?

- Cloud often begins with storage. But as companies digitize more of their operations and launch more features, they usually create hybrid digital operations (part on cloud, part on premise). The jobs to be done are pretty complicated.

- Is there a tailwind for demand?

- Yes in terms of activity. This is going to be a massive trend long-term. However, we need to watch for overall revenue. This may end up making everything cheaper, which often happens with technology. So, while activity may increase, spending may not.

- Is there also a demand floor in activity, revenue per transactions and overall transaction revenue?

- Probably yes for the dominant platform cloud providers like AWS. The smaller enterprise services can change very quickly. And lots of these services get commoditized and become obsolete. For example, Zoom is at risk of this. But being one of 3 big cloud and service providers is about as good as it gets.

What about for the logistics business?

- What is the job to be done?

- This is the unclear question that JD has tried to answer this with its end-to-end, integrated solutions for logistics and fulfilment. It’s not clear this is getting a lot of traction. Amazon is probably closer to the FedEx model in the short-term.

- Is there a tailwind for demand?

- Yes, in terms of activity. The numbers of packages moving around increases as a country becomes wealthier. It’s actually a nice long-term growth trend in terms of volume. Plus it is boosted by ecommerce usage and cross-border activity. And the revenue per transaction stays stable, unlike for technology and digital goods. The logistics volumes for China are crazy.

- Is there also a demand floor in activity, revenue per transactions and overall transaction revenue?

- Yes. I like logistics as a potential business.

Overall, I really like the ecommerce business and the web business. And logistics could be very attractive as a stable, long-term growth story.

That’s my take. Cheers from Koh Chang, Thailand, -j

——

Related articles:

- What Amazon Should Copy From Alibaba and Pinduoduo (Tech Strategy – Podcast 124)

- Amazon Has a Winning Long-Term Strategy. Amazon Prime and Netflix Don’t. (1 of 2) (US-Asia Tech Strategy – Daily Article)

From the Concept Library, concepts for this article are:

- Economies of Scale: Purchasing Economies

- Economies of Scale: Fixed Costs

- Linked Businesses

- Jobs to be done

From the Company Library, companies for this article are:

- Amazon

Photo by Christian Wiediger on Unsplash

#techstrategy #amazon $amzn

——-

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.