I’ve discussed Amazon’s basic business model in an article and podcast.

- What Amazon Should Copy from Alibaba and Pinduoduo (Tech Strategy – Podcast 124)

- Why I Really Like Amazon’s Strategy, Despite the Crap Consumer Experience (US-Asia Tech Strategy – Daily Article)

And I basically argued that I look for 3 things in this type of company:

- A long-term secular growth trend with a stable minimum floor for demand.

- A strong business model with moats that captures this trend.

- Minimal risk of significant change in consumer behavior, technology, or regulations.

But I didn’t really go into question 2 in detail. That’s what this article is about.

Competitive advantage in digital businesses is my area of research. And I think this is where people are underestimating Amazon’s ecommerce strategy long-term. It is also where they are over-estimating Amazon Prime (and Netflix).

Amazon’s Ecommerce Business is Getting Stronger.

Amazon’s ecommerce business is a combination of an online retailer and a marketplace platform. The company does lots of spending and innovation in logistics and technology. But, as mentioned, there is little innovation on the consumer-side. Certainly, nothing like what we see at Alibaba and Pinduoduo.

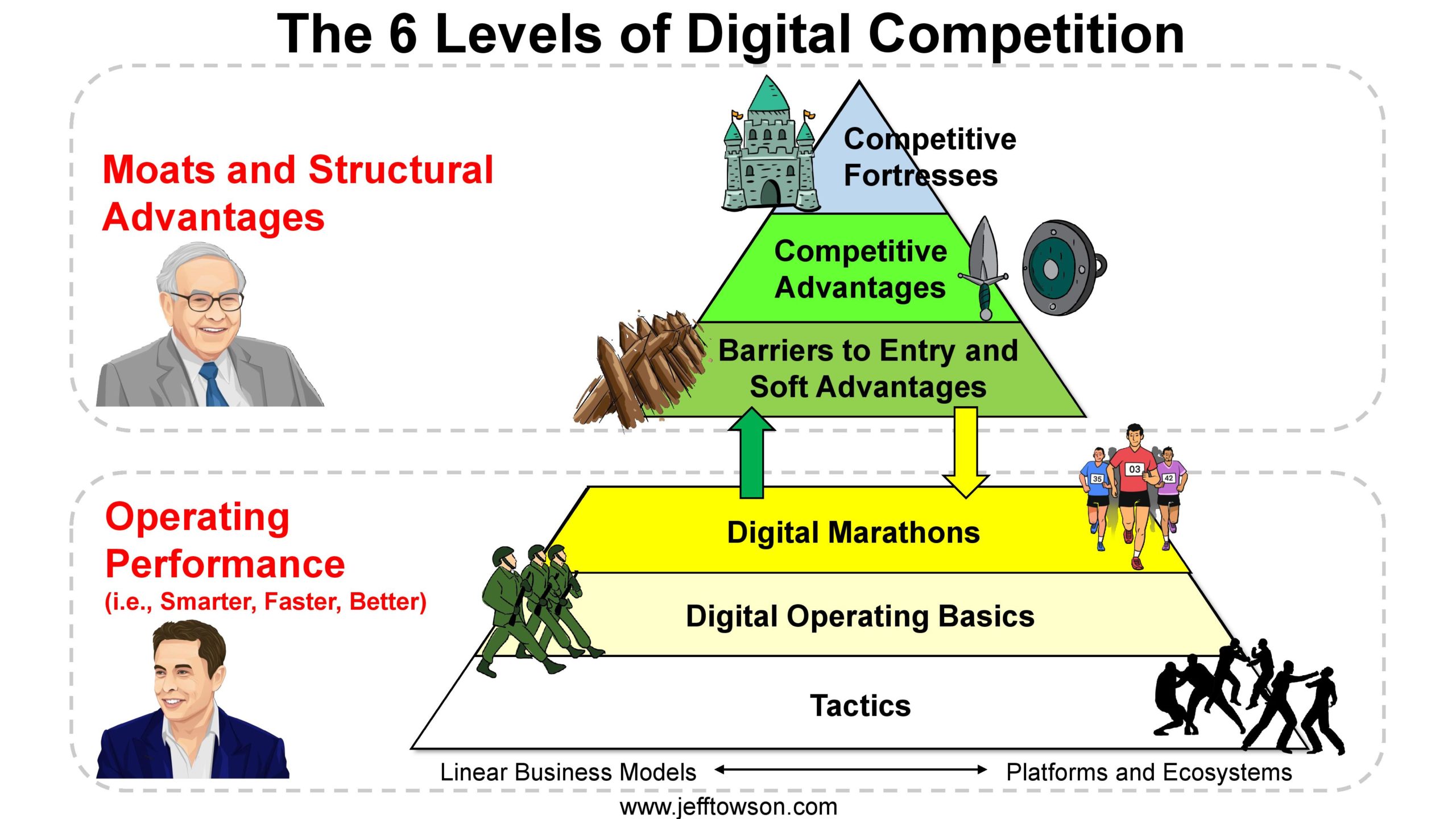

So let’s just run my 6 levels for digital competition for the ecommerce business.

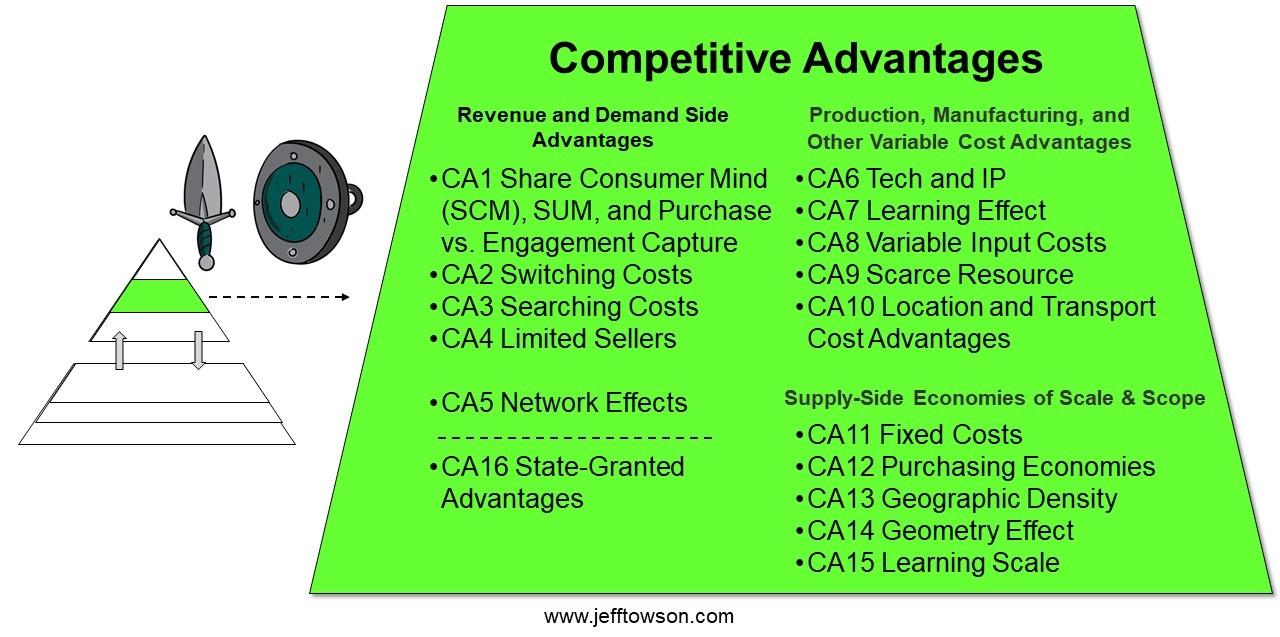

Level 2 is Competitive Advantages. And there is a lot going on with Amazon ecommerce here.

Running the list, a couple of minor things jump out:

CA1: Share of the Consumer Mind

This is the Warren Buffett term for having a degree of customer captivity on consumers. There are lots of ways to achieve this (habit formation, emotional, perceived risk, etc.). But I think for Amazon, it is not particularly strong. There is some brand loyalty and lots of usage. But this is mostly typical shopping. Not entertainment. People mostly go on Amazon for the same reason they go to Walmart. It’s ok and there is some demand-side power, but it doesn’t knock me over.

CA2: Switching Costs

Investors love switching costs but you can’t really do these very much in B2C digital. They annoy consumers so it has to be light touch. However, it is particularly effective on other user groups on platforms. Third party sellers on Amazon’s marketplace have significant switching costs. The more they become dependent on the platform and the more they operationally and technically integrate, the higher the switching costs. Not bad.

CA4: Limited Sellers

I also call this a “long-term supply-demand imbalance”. This is when the market is limited to a few sellers for the long-term. And these few sellers have some demand-side power by virtue of this imbalance. They can premium price and other things.

Given that Amazon marketplace’s is approximately 25% of US ecommerce spending and Amazon’s retailer is 17%, the business has +40% of the US market. This is a limited sellers situation. For Amazon’s ecommerce business, this is by virtue of its network effect and supply-side power (discussed in a moment).

Ok. Those are fine but not overwhelming. The real competitive power starts to kick in with:

CA5: Network Effects

In 2021, Amazon’s marketplace platform was in 19 countries – and surpassed $390B in GMA (not including Amazon’s own direct retail). In 2017 alone, over 1M sellers joined the platform.

Big surprise, this massive marketplace has big network effects. And while some network effects are fairly weak (hello Uber), they are strong on Amazon. The value to consumers continues to increase with the increase in merchants and product types. There is a nice long-tail of product types that increases the value to consumers and enables personalization. That is rare. I’ve written about this here.

Looking for competitive advantages on the cost and supply-side, we can see some minor strengths in proprietary technology (CA6) and learning effects (CA7). But the power is really in:

CA11: Economies of Scale in Fixed Costs

The numbers that matter here are R&D, logistics and technology, which are really under the heading of “infrastructure”. And the numbers are huge. Amazon is flooding money into infrastructure in a way that dwarfs its competitors.

You can’t really separate out the tech spending for ecommerce vs. AWS. Or the marketing spend from AWS and Amazon Prime. But the logistics picture is pretty clear. In 2020, Amazon capex was $35B, which was more than three times Walmart at $10B. And competitors Target and Home Depot were each at $2-3B.

The logistics spending is going into capacity and automation, which is fairly similar to Alibaba. Lot of new fulfilment centers, moving supply chain in-house, adding air infrastructure and moving the inventory closer to consumers.

In theory, superior scale and higher fixed cost spending gets you lower per unit costs (as you spread fixed spending over larger activity). However, most competitive advantages can be used for offense or defense. That’s why my little graphic is a sword and a shield. Superior scale can be used as a weapon. You can outspend rivals in strategic assets, such as logistics, R&D and marketing. Or it can be used for defense, where you cut costs below what your rivals can match and pass savings onto customers. You can also use it to take profits. Amazon mostly plays offense.

CA12: Economies of Scale in Purchasing Economies

Amazon’s superior scale also plays out in a major way in the cost of goods sold (when Amazon acts as a retailer). Similar to Walmart, they use their scale for discounts from suppliers. It also plays out in the delivery costs, where they have long been a big buyer. Although they have now mostly brought these costs in-house.

Both scale advantages (C11, C12) are on the supply side and are only available to the market leaders. Everyone can build switching costs and consumer power, but only the market leader can scale advantages versus smaller rivals.

***

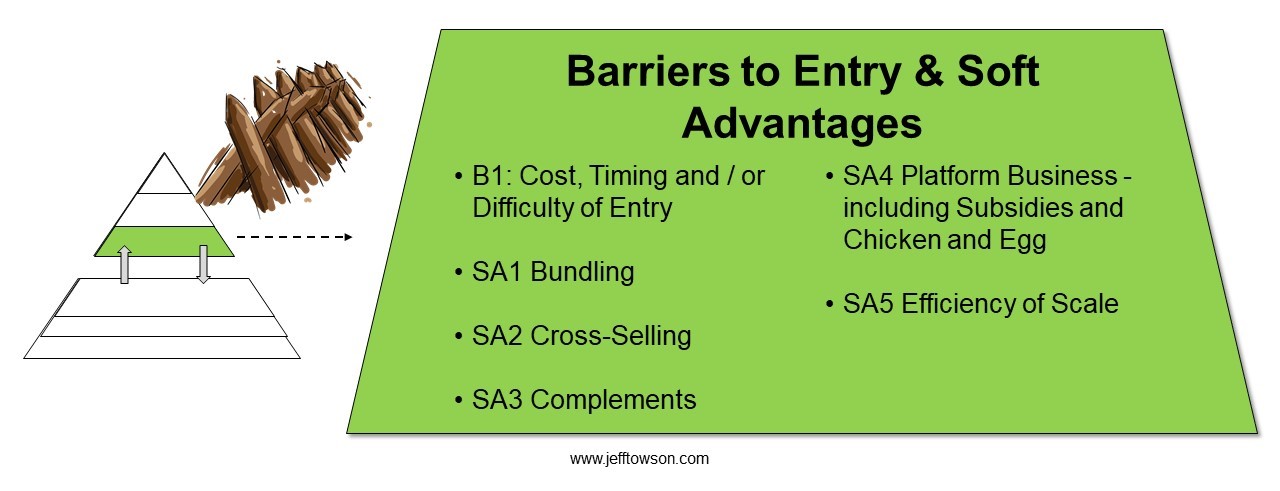

Take a look at Level 3:

You need to separate the difficulty of jumping into a business (barrier to entry) and the difficulty of competing in a business over time (competitive advantage). These are two different things. And new digital tools and business models can impact one, both or neither. Usually, new digital tools impact barriers to entry the most.

B1: Cost, Timing and/or Difficulty of Entry

This is basically doing a reproduction valuation of the key operating assets. What would it take to replicate them and get into the business? Would it be expensive, difficult and/or take a long time?

Amazon ecommerce is fantastic here. Building out all those digitized warehouses to cover the US (and 18 other geographies) takes years, if not a decade. And it’s not just about spending the money (which is big), it’s also about developing the specialized technology to automate them and match the performance. I usually like combinations of digital and tangible assets because of the barriers to entry they create.

SA4: Platform Business

Getting into a marketplace business means getting over the chicken-and-egg problem, also called the cold start problem. That is difficult in a new platform. It is next to impossible against an incumbent. Additionally, Amazon is adding advertisers to their platform. And a search engine (sort of). They can increasingly add user groups and do price subsidies.

Amazon’s ecommerce business has a fantastic barrier to entry. And several good soft advantages.

***

Ok. So what? That’s pretty standard stuff for Amazon. And for big retailers and marketplaces. This is first level thinking.

But now let me ask two questions that will show why Amazon ecommerce is getting stronger and Amazon Prime is getting weaker.

Question 1: How Do These Advantages Play Out Versus Rivals, New Entrants, and Substitutes?

This is the part people usually get wrong.

How do the competitive advantages appear to large rivals? Could a large rival take market share over time?

- For Amazon, this is basically Walmart and Target. We are long past the days of online companies have competitive advantages over offline players. Most mass merchandise retail is heading towards online-merge-offline. With this business model, that means Walmart and Target and a few others.

- Right now, Amazon is beating them in all the factors just mentioned. And getting stronger.

How do the competitive advantages appear to small rivals? Could a smaller rival grow to become a large rival?

- The position of the giants is insurmountable to the dwarves at the national level. There could be competitors at the regional level and in certain categories. I have written about specialty ecommerce strategies that are viable – but they all include avoiding the strategic targets for the giants.

What the barriers and competitive advantages versus new entrants? Could a well-funded company break into the business?

- In China, yes.

- In the US, against Amazon, nope. This would be very difficult and would likely require a major acquisition like Walmart buying Jet.com. We’ll see this coming a long way off.

What are the substitutes? Are there low-cost or free substitutes?

- Families need both staples and discretionary products in life. And Amazon’s marketplace plus retailer model means there is little they don’t have and no substitutes.

***

I like to think about these questions from the point of view of a rival or new entrant. Could I come up with an approach for breaking into this business? Could I offer a differentiated product? Could I come up with a low-cost substitute?

And basically, I can’t figure out any way to overcome Amazon’s advantages. I see a long, hard and expensive fight for every customer. I would have to get lucky with bad management or a new technology that let me jump in.

Question 2: How Will this Picture Change Over Time?

For Amazon ecommerce, it all basically gets stronger.

- The marketplace will continue to add more merchants, categories, and products. Amazon looks more and more like the everything store.

- The network effect will continue to increase somewhat linearly for both consumers and third-party sellers.

- The company will maintain or increase its purchasing power in its cost of goods sold. They will be untouchable in terms of price to all but a few companies.

- The company will keep outspending rivals on logistics and technology. This will likely keep resulting in faster delivery, better customer service, more advanced technology and cost reductions. Plus, Amazon has externalized its web services (AWS) and logistics as services to the market. This will get them even greater economies of scale in these areas.

- The barrier to entry keeps growing with greater logistics and technology infrastructure. If they would add physical retail (like Alibaba) it would be even better.

What about changes in consumer behavior, technology, or regulations?

- Amazon ecommerce is not exposed to consumer behavior changes. Consumer buying behavior will change but a lot of it is stable. And with all Amazon’s merchants and products, they will naturally adapt to any changing behavior.

- Technology is going to change, which is a risk. But Amazon plus AWS is on the technology frontier. Plus, they can do M&A if they miss something important.

- Regulations are really the only big unknown here. Labor unions are potentially an issue. So is regulatory action. But the trend is towards digital operations and robotics.

Basically, I see only a few large rivals to pay attention to. The infrastructure-focused business model is almost untouchable now. And the key competitive advantages identified are all going to get stronger over time.

- I do know some good counter strategies for specialty ecommerce and for some segments like groceries, furniture, and fashion. I like Etsy and Oriental Trading Company.

- I think there is the potential for an entertainment and attention businesses like TikTok to add ecommerce. This focus on consumers and attention, instead of infrastructure, is a potential counter strategy.

- My biggest concern is the WeChat mini-programs approach that rejects the marketplace model and mergers social media with ecommerce. Shopify plus Facebook would be a concern in the USA.

But I don’t know how to beat Amazon’s core business or take significant market share right now.

***

Now, the reason I ran a checklist for ecommerce is because you get very different answers when you run it for Amazon Video. It immediately jumps out how much weaker the business model is. And that much of its success is from tactical and operating performance, not structural advantages. I’ll cover that in Part 2.

Cheers, Jeff

—

Related articles:

- Why Netflix and Amazon Prime Don’t Have Long-Term Power. (2 of 2) (US-Asia Tech Strategy – Daily Article)

- What Amazon Should Copy From Alibaba and Pinduoduo (Tech Strategy – Podcast 124)

- Why I Really Like Amazon’s Strategy, Despite the Crap Consumer Experience (US-Asia Tech Strategy – Daily Article)

From the Concept Library, concepts for this article are:

- Economies of Scale: Purchasing Economies

- Economies of Scale: Fixed Costs

- Network Effects

From the Company Library, companies for this article are:

- Amazon

Photo by Christian Wiediger on Unsplash

——-