This is Part 2 about Pinduoduo and the idea of interactive / engagement-driven ecommerce.

In Part 1, I discussed a recent whitepaper with its authors Elliott Zaagman (co-host the China Tech Investor podcast and a research and communications professional focused on China) and Matthew Brennan (Managing Director of the China Channel.)

Their whitepaper on Pinduoduo and interactive commerce is available at China Channel or can be downloaded directly here (Interactive Ecommerce Whitepaper 2020.08.10.)

You can listen to this podcast here or at iTunes, Google Podcasts and Himalaya.

The 5 choices for explaining Pinduoduo’s success are:

- First mover in a huge market. Got the right product at the right time in the right market.

- Offered low cost (sometimes free) products to a frugal demographic.

- Interactive / engagement-focused ecommerce.

- Group buying and virality. The tie with WeChat.

- Good execution and management.

Related podcasts and articles:

- #31: Introduction to Pinduoduo

Concepts for this class. The slides discussed in the podcast are located below and correspond to the 4 ideas below.

- Value for Money. The Power of Cheap and Free. Example of Digital Superpower #1: Dramatically improving the user experience.

- Interactive / Engagement-Focused Ecommerce

- Virality and Word of Mouth

- External View and Base Rates

Companies for this class:

- Pinduoduo

———

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.

—-transcription below

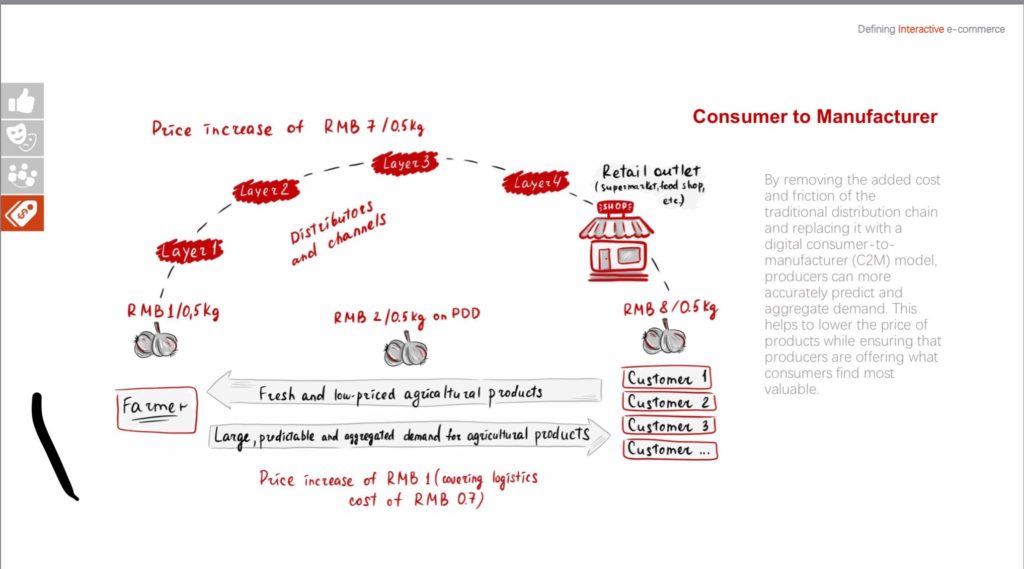

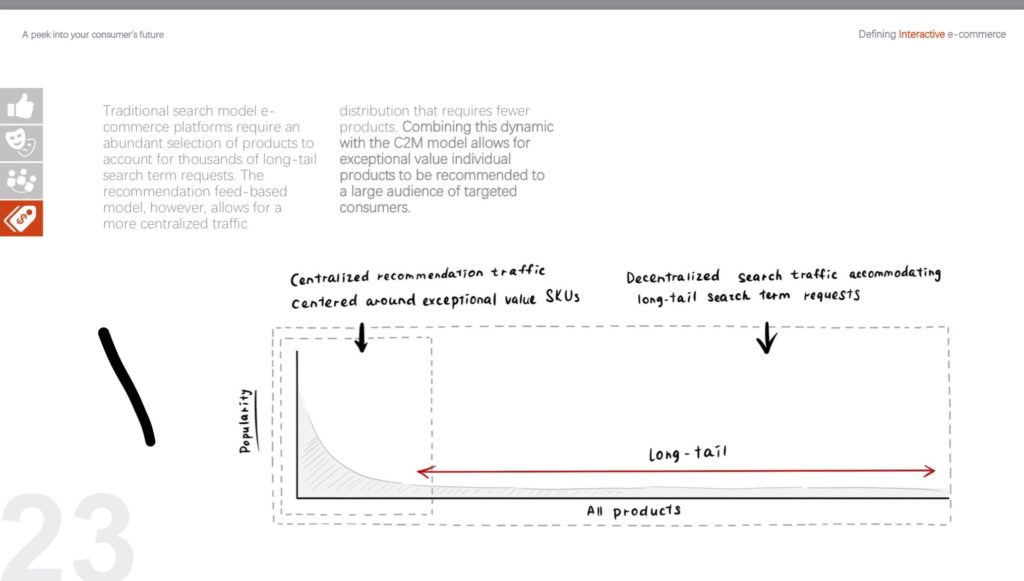

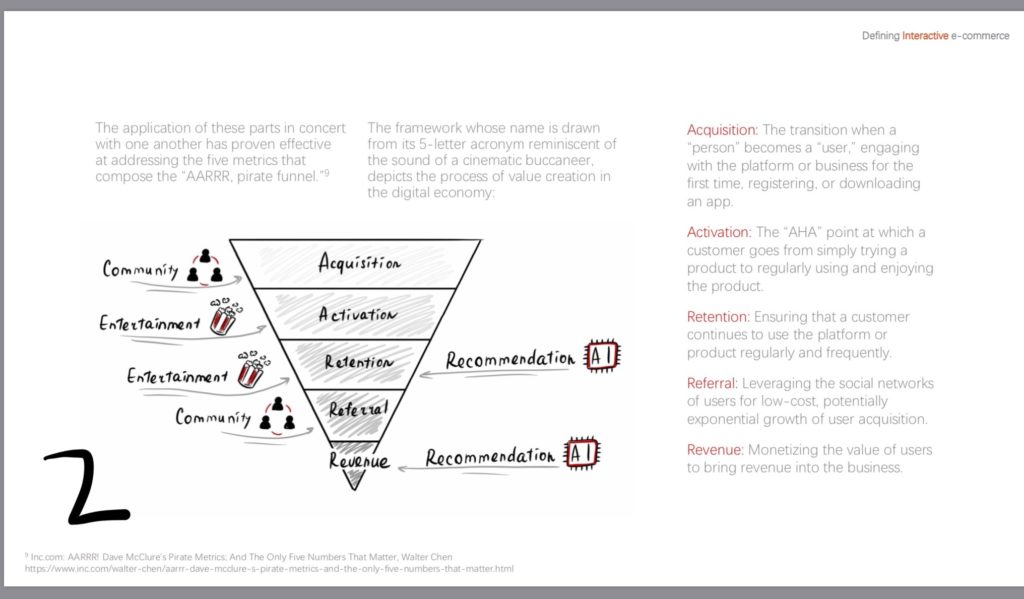

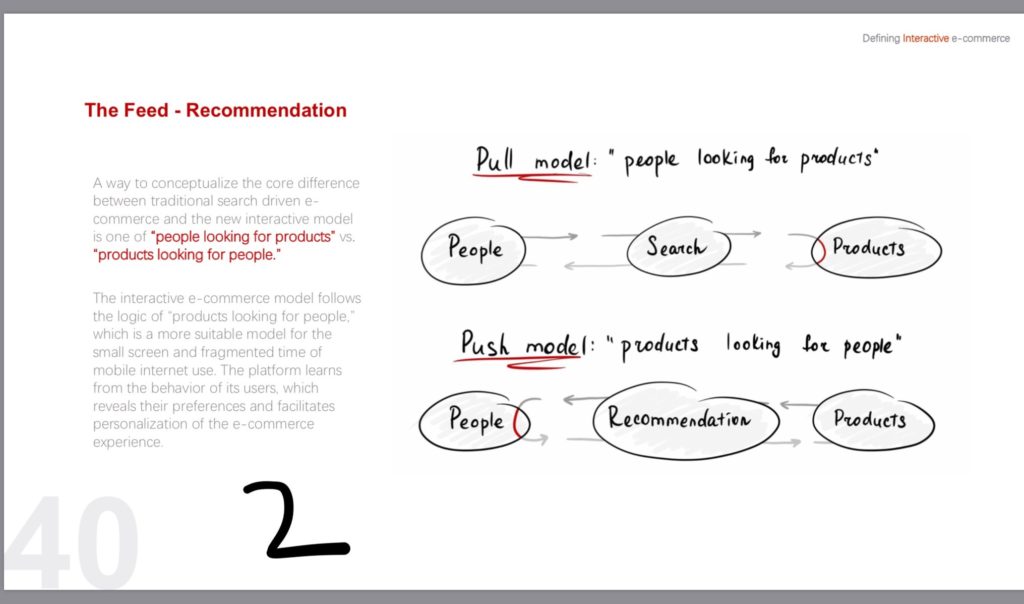

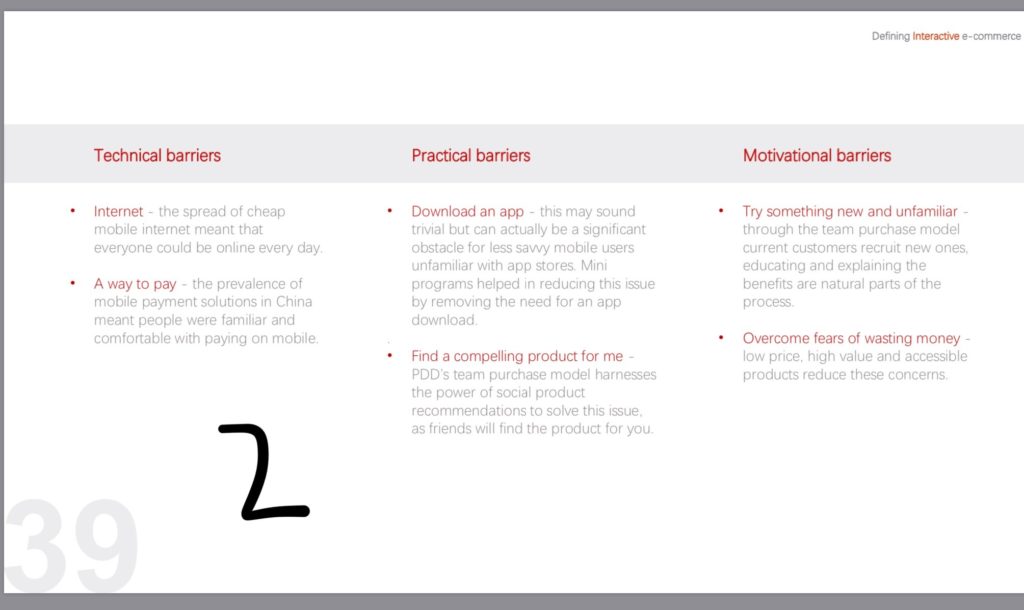

Welcome, welcome everybody. My name is Jeff Towson and this is Tech Strategy. And the question for this class, what is the secret of Pinduoduo’s success? And this is really part two of this question, the previous podcast, which is number 45. What was the same question and did that as an interview, as a discussion with Matthew Brennan and Elliot Zagman, who had recently put out a white paper on this subject. So. This is gonna kinda be the second pass at this question, and I’m just gonna take you through some other theoretical strategy aspects that didn’t get covered last week. And then at the end, I’m gonna basically put to you the same question as the previous one, which is what is the biggest factor for their success? And I’m gonna give you the same five choices I gave you in the previous one. So we’ll see if at the end of this year, thinking has changed. Now, for those of you who are members, This is gonna be the same basic learning goal, number 31 as the last one, which is an introduction to Pinduoduo. This is under level eight of the sort of curriculum for the class. The three ideas, actually there’s four ideas. I give you three sort of key concepts to remember about this company and this situation. And that’s generally how I like to do it. I sort of tee up what I think are the important concepts of digital strategy and then we tie them to a company. So if you can remember the company, you can remember the concept. So just a little trick. But three of them are the same as the previous podcast, which are value for money, basically the power of offering things cheap, interactive or engagement driven e-commerce, which we’ll talk a lot about, virality, team buying, which is a big part of Pinduoduo. And then those are the same three as the previous podcast. The fourth one, fourth concept for today is, what we call the external view or base rates. And this is, investors always talk about this, but for those of you who aren’t on the investment side, this might be new. So external view and base rates, those are the four sort of key concepts for today. And for those of you who aren’t members, you can sign up right now at jeffthousen.com. There’s a free 30 day trial. So it doesn’t cost anything. See how it works for you. Try it out and join the group and it’s actually been going pretty well. This is about 10 months into this class. I feel like we’re really starting to click a lot more. So hopefully it’s getting better and better as we go along. That is the idea. Okay, let’s get into the case. Now in the last podcast, I gave you basically five options. The question here is, how did Pinduoduo break into a relatively established? market, let’s not call it mature, but established e-commerce was not a new thing. It is dynamic, it does change, but it certainly wasn’t a new thing. So it’s, let’s say, an established market with major players that are fairly well run, Alibaba, JD, I mean, this is not like a sleepy incumbent you’re taking on. So how did this company break into this space and then show really stratospheric level of growth? And we’ll talk about that sort of crazy growth story between 2015 and 2018. Okay, when you see something like that, the first thing, something special is going on because that’s not what happens in business. You don’t break into an industry like this and just, you know, the numbers go off the chart. Whenever that happens, it’s not that people are working hard and it’s not that people are smart. It usually means there’s some economic or strategic element playing out. that the numbers just grow too fast for, hey, we worked really hard. And the five choices I gave you for what were the biggest factors for that break-in and early success, not their situation now, but 2015, 2018. I gave you five choices, and these are in the show notes, and we’ll go through these when I ask you in this class. First one was First Mover in an untapped market. Basically, this fourth and fifth tier Chinese cities. was a very big market and they were sort of had the right product at the right time for this market and it just clicked. Second option, low cost products and services for a very frugal demographic. Being cheap is a big lever in any business. Anytime you can take something that exists and let people do it cheaper, that’s a big sort of dimension of attack. Number three, engagement-focused e-commerce or interactive commerce. That’s kind of the theoretical idea. We’ll talk about that. Number four, team buying, which is a viral mechanism. When one person buys, by definition, their activity brings other people in as customers, group buying. And number five was just good execution and management. Maybe other people had tried and this group just pulled it off. Okay, so. Which of those five were sort of the top one and two choices to explain this phenomenon? Now, if you go through the history of PDD, I’m Pinduoduo, PDD, okay, they kind of talk about it in two phases, there was PHH, which was, you know, when they started out, they started out basically as a retailer, not a marketplace platform, but more of a retailer, connecting consumers with… you know, manufacturers and produce and sort of C to M direct retail in the agriculture grocery space and basically offering low priced products for this sort of very frugal demographic of third, fourth and fifth tier city populations. Okay, that’s not really the interesting phase because that’s not when we saw the growth really kind of explode. when they start calling themselves pin do a do a PDD, that’s when the numbers really go off. So I’m just gonna sort of jump to that. And that’s between say 2015 September-ish when they started and 2018, they brought in according to them 300 million active buyers per month. That’s a crazy level of growth in just a couple of years. And if you look at the sort of self-reported numbers, You know, late 2015, September, November, within three to four months, they had 10 million people. And so you could see it, when it started to click, it really jumped off the page. Okay, and then they went public in 2018, and then things have changed a bit since then. But if you look at that period there, you’re gonna hear a lot of different ideas thrown together, you’re gonna kinda hear some different stories. I think it’s easy to get confused. There’s a lot going on. I’m gonna give you the commonly sort of described story. If you go look up Wikipedia or something, you’ll hear all of this mentioned in various forms. It’s easy to get confused. First thing they did is they shifted to a marketplace platform. Okay, I’ve talked about platforms over and over marketplace. Obviously one of them, you know, instead of being a retailer, we buy the goods, we own them, we put them in our warehouse, they’re on our balance sheet, and then we sell them and we make a gross margin. Now forget that game, we’re just gonna enable interactions between other parties, merchants and consumers, or in this case also manufacturers. Okay, they shifted to a marketplace model, much less capital intensive. They started to leverage in WeChat in a very powerful way, because keep in mind, they did kind of hit the timing right here. WeChat was really just taking off in terms of WeChat plus mobile pay at that time. Suddenly… this other demographic out in these other cities, they weren’t sitting on their PCs, well, no one in China sits on their PCs, but they didn’t have Taobao and Tmall accounts. They had a lot of cheap smartphones, they had data plans, and at a certain point, they all got on mobile payment where they could start to buy things at any time. So they kind of hit the window for when WeChat and mobile pay really hit the ground in China. They also sort of timed it beautifully in that logistics, had been, you know, the logistics network of China had been building out for seven or eight years related to e-commerce. And it was robust enough to reach all of the cities, all the provinces, all the, most of the villages. And you could start to sort of contract that instead of having to build your own warehouses, which is what JD had had to do and what Alibaba had done, although they kind of did it indirectly. And then you have this other factor of the fact that like, if you’re gonna do C to M, consumer to manufacturer, where you’re gonna connect manufacturers, say making Kleenex or, you know, it could be on the produce side, agriculture, directly with consumers, you need to be in a country where all the manufacturers are, that really helps. Well, China has that. So it’s kind of all three of those factors all hit at about the same time. And that’s why this idea, maybe they just had the right product for the right market at the exact right time and things took off. 2017, you also saw WeChat mini programs start to take off. So WeChat went from being Messenger and then Messenger and payment to Messenger payment and e-commerce. That all happened at about the same time. You’re going after… Not rural. Everyone thinks it’s rural when you say fourth and fifth tier cities. People think it’s villagers. It’s really not. It’s, you know, there’s hundreds of Chinese cities with 300,000, 500,000 people in them. A million people is a pretty small city in China. So there’s tons of these. So this is an urban phenomenon more than anything else. A lot of moms, a lot of basically women, which is not uncommon in e-commerce. 25, 35, that sort of window, a lot of young moms. So with the things they were selling like produce, Kleenex, household items, you’re sort of speaking more to a household than as opposed to guys buying laptops, which JD does a lot of that. And because when they started, they really focused a lot on produce, perishables, household items, things that, you know, staples of a typical household. Even if that household is very, very frugal, which a lot of these consumers are, these are still the things you need in life, the staples, the repeat purchases. So that’s kind of one set of ideas you hear about with this company, but it also tees up the next one, which is they really didn’t go after broad-based e-commerce. You know, the traditional playbook for an e-commerce company like an Amazon or a big retailer like a Walmart is we have the largest selection of goods at low prices. It’s both. It’s breadth of products, so lots and lots of SKUs and low price. So you can go to Walmart to get virtually everything you need in life. There’s no reason to go everything else because there’s no reason to go anywhere else because they have everything. And Amazon kind of copied that in Taobao, copied that in JD. They have a more select spectrum of goods because they sort of select for quality. But that’s generally the approach. Okay. Pinduoduo really turned that on on its head. They said, we’re gonna ignore the long tail. We’re not gonna try and offer everything. We’re gonna only offer the things that are the most common purchases, the household items, the Kleenex, the toilet paper, some basic produce. And instead of offering the whole long tail, we’re gonna have this little pretty narrow sliver of goods and that’s gonna have some important effects on their business model. The first thing is, it decreases their operational complexity dramatically. And that plays out in costs. It’s one of these things where if you can decrease the number of products or services you offer, it plays out all across your organization. Management focus, inventory levels, accounts receivable. It’s just really one of those things when you do less, you do it better and more efficiently. It decreases the complexity. It also tends to decrease their need for inventory. It tends to lower their cost of goods sold because they can make larger purchases of a smaller number of items. Instead of making lots of small purchases across lots of things, we’ll make some big purchases across a small number of things. That’s really the Costco model, which is why you hear Pinduoduo, they self-describe as Costco meets Disneyland, which I think is not accurate. It’s kind of confusing really. I like the Costco part, which is… we are gonna offer a select number of items and those are gonna be really cheap because we don’t offer everything like a Walmart. And Costco and Sam’s Club are really counter strategies to a Carrefour and a Walmart model. And they’re known for being cheaper. That’s how you get to cheaper than Walmart is you narrow your selection of goods. Then it turns out there’s also some maybe funny implications of this. If you’ve… ignore the long tail go for select items, your company’s simpler and you’re generally cheaper. That’s the Costco effect. There is this idea floating around which I don’t know if it’s true or not, but because people purchase more based on sort of inspiration as opposed to searching, that they’re more accustomed to longer wait times. Basically, you don’t have to deliver everything the next day. people are willing to wait for these purchases in a way that they’re not willing to wait for, say, JD. Because a company like Alibaba competes on breadth of product selection, low price, speed of delivery. Well, their customers may not care about the speed of delivery. So they may have eliminated two of those factors and they’re mainly about price. I’m not sure that’s true. But that’s kind of the second idea you hear with Pinduoduo, this Costco approach that we’re gonna ignore the long tail go with very low prices on a select number of household commonly used items. The third idea you’ll hear, group buying. That we’re gonna use the WeChat effect, virality. Now, people like this because it’s viral. If I buy on Pinduoduo, the way it works, at least back then, not so much now. I go on Pinduoduo, it gets me two prices. I want to buy a box of Kleenex, here’s one price, and here’s a group price, which is 30, 40% cheaper. If I click on the cheap price, I have 24 hours to go find the number of people I need, and we all buy together, and then I get that price. And the company would set that. This wasn’t pin dodo, this is whatever companies they were approaching, a manufacturer, retailer, merchant, they would set the individual price and the group price and how many and things like that. And… You know, that gets you viral growth, which is very useful in the early days of a company because every customer gets you two or three more customers you sign up. So you can sort of think of, well, that’s a cheap way of customer acquisition costs. It also helps you get cheaper products in general because we know that if so many people are gonna be buying from a manufacturer, the manufacturer will give a special low price for that item, you know, based on volume. So you kind of get two effects there. You get viral growth and then you also get basically cheap prices and people like cheap prices. And I’ve never, I’m not sure if this is true, but I’ve read that early on they were giving things so cheap that if you got enough people to buy with you, you basically got the item for free. And they were just using this as a mechanism to acquire customers and get them on the platform. I’m not sure if you could actually get stuff for free. I know you could get stuff really cheap if you brought in your friends. The next idea is what they call the Disneyland effect. I don’t really buy that. I think of it like TikTok. I think they have sort of created an e-commerce model that is engagement focused, not sales focused. They’re not, the whole thing is not designed to get you to come and spend money as a, you go to Walmart to buy stuff. That’s why you go to Walmart. They get you to come here just to spend time and enjoy yourself and watch some videos and do things like that. It’s engagement driven and then you buy stuff along the way. And as part of that, you know, it tees up lots. It basically you’re watching a newsfeed just like TikTok. You sit on there, special deals come up in a newsfeed. You pick the ones you want as they scroll by. That’s kind of what TikTok is doing. It’s a push mechanism rather than a pull mechanism. It’s not like going to Amazon and searching for what you want. You just turn it on, stare at the screen, veg out, and watch them throw up deals that you can choose to buy. So that’s really a contrast to Walmart. And I think TikTok is the closest analogy to that. Select items, you buy as you get inspired, it’s kind of fun, it’s discovery. And the metric you’re gonna look at is primarily interactions and engagement, not GMV. Okay, we’ll talk more about that. But those are kind of the big ideas. I also think they had a very tiny take rate early on. That’s kind of similar to what Xiaomi did. You know, Xiaomi got into the business, we’re gonna sell smartphones. They’re gonna look just like the iPhone. This is 2012-ish. And we’re gonna charge, you know, a gross margin, a gross profit of the item of 4%. under 5%. And by offering things cheap at a very tiny margin, well, it makes things cheaper in people like that. I also think they were doing a lot of this. They were just doing e-commerce at a tiny take rate. It makes things cheaper. That’s a good thing. And then maybe the simplest way to think about this is, you know, they were just making money in a different way. That’s a really powerful strategic move. And people like me who do strategy, you know, we tend to get overly excited about that. So it tends to get a bit over-hyped and maybe we overemphasize it a little bit. But they went into e-commerce the same way that Sam’s Club and Costco went into physical retail. They just said, we’re gonna do what looks kinda like the same as a Walmart, but we’re actually gonna make our money in a different way. So you go into a Sam’s Club or a Walmart, or not a Sam’s Club or a Costco, they’re trying to sell you memberships. You get a membership, they get a certain amount of money from the membership, and then, You know, the gross profits they make on their food are very, very small, because they’re kind of thinking as much, if not more, about the membership fees, as opposed to making money selling food to you. And that’s a good counter strategy. Now, this is kind of the same as they went into the idea of e-commerce instead of making money on transactions and selling stuff, selling goods. So we’re going to make money based on getting people’s engagement and time spent on platform, interactive, engagement-driven. And I think you can see that in the numbers because people always point this out at Pinduoduo. They say, oh, look at all these MAUs, these DAUs. This is a major e-commerce company. But then they look at GMV because everyone who looks at e-commerce loves GMV of gross merchandise value. And they say, huh, Alibaba’s, I’m sorry, Pinduoduo’s got 500, 600 million monthly African users, but their GMV is like 1 sixth of Alibaba. Well, that’s weird. You can see it automatically when you look at GMV and sales per customer on AlibabaJD, let’s say Suning.com, they’re all in roughly the same ballpark. And then you look at Pinduoduo and the number’s completely different. Well, that’s because I think that’s not the measurement they’re looking for. They’re focusing on engagement, interactivity, the same way Costco’s focused on memberships. So. You can kind of see that you look at their engagement, it’s very high, but you look at their GMV, their sales per user and things like that, it’s very, very low. So that’s engagement driven e-commerce, interactive commerce. And they’re making money more or less on advertising at this point, but when you get engagement, one of the nice things about that is you can start monetizing that in lots of creative ways. And China is really good at this. That… When you get these large volumes of people, whether they’re watching live streaming or playing video games, you see a lot of creative mechanisms to monetize that engagement, like gifting, virtual goods, live streaming, advertising. In fact, they tend to shy away from advertising because digital advertising in China is a little bit dodgy. So that’s one thing they’re doing. Okay, they’re focused on advertising, which is really the merchants and the brands doing this. The other thing… that they appear to be doing, although I haven’t confirmed this, is, you know, they’re focused on the float. I guess Colin Huang is a big fan of Warren Buffett. He’s met them. He met him at a certain point. Warren Buffett loves float. The basic idea is you always want to be in a business where you get paid first. Where instead of I buy the goods and I put them under the shelf and then I wait for people to show up and then buy them and then they give me money. Insurance is better. Insurance people pay you upfront. You sign a contract but you don’t have to spend any money. and then over the next year or so, then you may have to pay out based on what happens with the insurance claims. But you get your money upfront, so you’re sitting on a pile of cash. You can invest that and you can do some things. So, you know, there’s this idea that Pinduoduo is generating a lot of float. When people place the ads, it’s not really ads in this case. It’s, if you’re a merchant or a brand or a manufacturer and you wanna put your goods up on Pinduoduo, you’re basically paying for placement in the newsfeed. which is a really nice form of advertising. It beats the heck out of like banner ads and stuff like that. So you’re prepaying that. You get your money upfront. The other thing I’ve heard said, but I can’t confirm either of these two things, is anytime you click on, I’m gonna buy something with my friends, it automatically charges your card or your mobile payment or whatever you’re using. And then within the 24 hours, if you completed the transactions done, if it’s not, then the money’s returned. So they may be sitting on a lot of cash up front. And that’s consistent with the fact that Colin Wong went public and he still owned most of the company. That’s kind of, I think, another idea is making money in a different way in the same field is a great strategic move. I would generalize this more in that I think what we’re seeing across Asia. China definitely, Asia somewhat. This idea of adding value to your customers, your users, whether they’re merchants and brands, far beyond a transaction. That you might go into a store to buy something. That’s why you go. The store is there to do a transaction. You’re not going to digital spaces to do just the transaction. The store is offering you much, much more beyond that. The running club for Nike, which I keep mentioning, having fun on a website. watching live streams, they’re offering you a ton of value. And then the transaction’s only a subset of that. Now, I think that’s kind of a huge idea that we’re seeing playing out. Ant Financial, which for those of you who are members, I’ve put out two fairly in-depth strategy arguments about Ant Financial in the last week, though on email. One about how they really, three platform business models combined, and then how… They’re basically doing asset like credit tech. But Ant Financial is like that. Ant Financial Ant Group is offering a lot of stuff, payment, daily services, food delivery, movie tickets. They’re offering a lot of value beyond selling you an insurance plan. Now they’re making money on selling you the insurance plan, although they don’t sell very many of those right now. But they’re offering you a ton of value and then these financial services products like a mutual fund or borrow a little money or insurance fund. That’s just a subset of what they offer, even though that’s probably where they’ll make most of their money going forward. So let me sort of boil this down just to the three to four ideas I want you to remember for today. There’s a lot going on there. I think there’s three important strategy ideas and then one other idea, and those are the four concepts for today. And I’m gonna give you some slides from the document by Matthew and Elliot, which I think are great for this, and I will put those in the show notes. And the first one is just value for money. I mean, most strategy, when you take apart a company, it’s easy to come up with 20 factors that matter. The truth is it’s usually three things, no more than that. You do those three things right, the other stuff doesn’t matter so much. You gotta do it, but it’s not critical. You do all 20 and you don’t do those three right, it doesn’t work, right? So there’s kind of, I think, three big things happening that account for most of the success. And the first one is just value for money. This idea that, look, offering stuff for cheap, it’s just a good play. It’s, you know, pretty, anytime you can offer anything dramatically cheaper, people just show up at your door, especially if it’s a staple, like if it’s something you need in life as opposed to something you just like. That’s usually helpful. So here’s a quote from the doc by Matthew and Elliot, which basically says, Price is always the best vector of competition and the most direct method to delight consumers Okay, how are they accomplishing this? I think it’s four or five factors all playing out at once The first one is just C to M consumer to manufacturer, which is something you can do in China You know, there’s just a lot of layer of distribution in retail between let’s say a farmer which is where they started groceries perishables and Getting to the customer and if you can make a direct connection there, you can just really drop the cost of things. And it helps if you’ve got this sort of fairly narrow band of products you’re buying, and you can sort of tell the farm if you send us this many of this, we’ll cover it, you know, that having that direct connection and then sort of bulk buying a small spectrum, or a narrow spectrum of items is just going to let you drop the cost. And for those of you who know China, I mean, the agriculture space, the distribution, the small farms, it’s notoriously inefficient as a distribution and a supply chain. So I think that’s kind of the first one. And there’s a nice chart by Elliott and Matthew on this, which I’ll put in there. The second one is this ignoring of the long tail that you just do a small number of things, a small number of items around. you know, household commonly used things and then you offer them at an exceptional value. I mean, it’s like the core 20 things you might use in your household are dramatically cheaper and you just dump all that sort of long tail search stuff. And that also decreases your inventory costs, your logistics, I mean, it plays out all over the place. The other one they mentioned was, you know, just team purchasing, team buying. You know, if you’re doing bulk, Purchasing of anything which is kind of what Costco does, you know, you’re just gonna be cheaper So, you know higher volume higher sales you get low cost you negotiate and so on so that also helps you be cheaper You can kind of see that at least for the early phase of this company. There was just a strong You know, we’re gonna be cheaper than everyone else strategy and you know, that’s that’s great I think that’s great in general and I think it’s very good for this particular demographic of sort of lower tier Chinese cities. That actually is much more frugal than the rest of the population. So that’s number one. Number, that’s sort of number one concept for today. Value for money is a vector of attack. Number two, interactive or engagement focused e-commerce. I.e. hey, we’re not focusing on sales as I just said. And I’m putting in a chart here in the, on my webpage. It won’t be in the show notes if you’re listening to this on your phone, but if you click over to my webpage, you’ll see it for this episode. There was the sort of standard marketing funnel and Elliot and Matthew have sort of showed out where along the marketing funnel, you start at the top with acquisition, that’s the top of the funnel, then it goes to activation, then to retention, then to referral, then to revenue, right? It narrows. And that when you buy stuff on something like an Amazon, you really focus on that bottom of the funnel, right at the recommendation thing. I search for… I don’t know, a hairdryer and it shows me one. But you know, that’s where you spend your time, the recommendation, the sort of pull search-based e-commerce approach, where in this model, it’s really about engagement. And so you can see, you know, acquisition is a lot about team buying, group buying, community, activation and retention and referral. These things are a lot more just entertaining people, getting them to stay on your site and have fun. and they’re there and they’re doing stuff and they’re looking at things and then, you know, bottom of the funnels, then they buy stuff. So you’re really, you know, bringing in a larger group of people to get engaged on your platform. And I think that was a really great chart they did. Another way, if you go for engagement as opposed to sales, you get higher frequency of usage. And this is really about being mobile first. I still think a lot of the Amazon and stuff, they still think about e-commerce as something you do sitting at your PC at work or at home. But what you really want is a mobile first approach, which is like TikTok and which is like PDV, where you’re carrying it in your pocket as you go through your day, and you’re always checking it all the time. So there’s a very high frequency of sort of engagement. You might check a couple of messages, you might just be bored, you might see if your package arrived, you might see whatever’s trending or it’s coming down the newsfeed right now that might be a fun thing to buy at a great price. you’re just always sort of checking in, checking in, checking in on your smartphone. And if you’re focused on engagement interaction, that’s gonna be different than, hey, I’m searching to buy a new fan, let me go do a search. So I think you get a higher frequency of usage. That’s a pretty good one. Generally speaking, this looks a lot more like a TikTok recommendation AI sort of matching algorithm. where based, in theory, let’s say at the beginning, they were doing this pretty brute force. You log in, you go onto the site, and they start sort of showing you a newsfeed of deals. Hey, you can get tissue, you can get whatever. Okay, probably brute force at the early days, but the AI will get better. Much like TikTok is very good at showing you videos one after the next that you really do like and become addictive very quickly. So you can see that they’re gonna have a more and more mature recommendation engine. that just pushes things to you one after the next and that should get smarter and smarter. I mean, ultimately TikTok is an AI company at its core. And I tend to think that Pinduoduo that’s also one of their core activities is actually AI and matching and push recommendation. So that’s important. They had a nice slide in this document, the white paper about lowering the barriers to purchase. I hadn’t really thought about that before. But the idea was that, you know, in a traditional search for e-commerce, you have sort of motivational — these are theirs terms, not mine — a motivational barrier, a practical barrier, a technical barrier. You know, I don’t really want to shop today. I’ve got to put in my credit card, all that stuff. Technical, I’ve got to be at my PC. But When you shift all of this to sort of newsfeed driven, engagement driven on a smartphone, all of those barriers go down, people just engage more frequently, easier. I thought that was kind of an interesting concept. I’m still thinking about that one a little bit. If you do a push model versus a pull model, TikTok versus I’m gonna search on Amazon for something, I think the psychology is different. I think, you know, if I go to Walmart, I’m going there to look, I probably have a list of what I’m looking for. I might browse a little bit, but I kind of have a list of what I’m going for. I’m sort of intent. I have what we’d call strong commercial intent. I think, you know, this push model, the engage model, it’s more about impulses, more impulse shopping, just show… stuff and people, oh that’s funny I’ll buy that, oh that’s kind of neat I’ll buy that. It’s a lot more emotional, it’s a lot more impulse driven as opposed to sort of search driven and more rational. They used a couple different analogies for this. One was the idea of a sushi train where you’re sitting in a sushi restaurant and there’s a little conveyor belt or maybe a floating little boat or something and it just brings food along and as things go by you kind of… choose what you want, and you think, oh, I’ll try that, that’s interesting. That’s a very different process than, you know, picking up a menu and searching for what you want. You know, they are different. The other analogies they used, it’s more like the night market, for those of you in Thailand, or like going to the carnival, where you just wander around and you do things as they hit you. I don’t really, I’m not sure that captures it. I think those are both good. I like the TikTok analogy that you just sort of, you know. sit there and the videos tee up one by one and it’s very engaging and it’s sort of emotional and it tees up impulse buying. But I do think the psychology is different in these two types of e-commerce. I’m hoping someone digs into that more, does some studies about that. And then I guess last thing is, you know, if you’re getting a lot of engagement, it’s more emotional, it’s more impulse. The trigger to buy is a lot lower if the prices are small. If everything you’re selling is 10 quai, five quai, 15 quai, one or two dollars, whatever, the impulse to buy, it’s a lot easier to do it. So people just click, I’ll buy that, I’ll buy that, I’ll buy that. So I think there’s a lot within that interactive or engagement-driven e-commerce. So that’s kind of the second idea. And there’s a bunch of ways to come at this. I haven’t quite got it settled in my brain, but yeah, it’s pretty cool. And the last one is group buying, which obviously, virality. get you lower costs, which are good. They did tee up this idea of community, that when you’re buying things together, the behavior is different. I’m not totally sure about that. The other analogy they used was like a girl shopping trip where five people go shopping together, so it’s more of a group activity. I’m not totally sure I buy that. I like the idea of just virality and… you know, getting lower price because, you know, you’re all buying together. Beyond that, I think it probably depends on the industry sector. I don’t think girl shopping trip really makes sense when you’re buying Kleenex. If they were to do a model like this within fashion, then maybe that could be pretty compelling. So I think we could see this in other places where maybe that dimension would play out in different ways. But for basic household items, yeah, I don’t know. But anyways, that’s sort of the three ideas, three concepts, value for money, interactive or engagement focused e-commerce, and then team purchase virality, which is really in this case WeChat. I mean, that’s really where that’s all happening. You can’t really think about Pinduoduo as a company without thinking about WeChat. I mean, they are linked. And if you take away one, you know, well, if you take away Tencent WeChat, Pinduoduo is no longer Pinduoduo. I mean, it is core to the company. And that brings us, I guess, to the question. So… You know, I’m going to put it to you now. This is your question. What is the biggest factor? I’ll let you choose two. What are the two biggest factors that explain this sort of crazy early success, both breaking into this market and then the explosive growth in that 2015 to 2018 range? What are the top two factors that account for that, such that if you were going to build a business and you wanted to copy this, These are the two things you’d focus. We gotta do these two things. And the five I gave you, which are in the show notes, are first mover, which is, you know, they got the bright product at the right time in the right market, and the fact that they put it together first gave them a sort of a open field to run, where they didn’t have to fight anybody because they kind of put it together first. So it’s sort of a first mover thing. Second one is this value for money. low cost and in some cases free products to a very frugal demographic. Number three interactive or engagement focused e-commerce it’s this sort of clever business model. Is that a major factor or a minor factor? Number four group buying virality and number five just good execution and management. You know maybe other people had the same idea and they just outran them they were just faster on their feet. Maybe. Okay, so choose your top two and pause the recording, write them down, put them in your notes. If you’re in the subscriber, put this in your journal and then come back. Okay, now my take on this, which you’ve probably heard from last time was, I think it’s mostly about being cheap and viral group buying. I think the business model is super cool. I think it’s a really interesting idea. I think it’s gonna play out in a lot of other sectors in a much more interesting way, like fashion, luxury, things like that, where you can really get a lot more engagement, interactivity. I’m not sure you can really get that much interactivity or engagement when you’re selling Kleenex. tissue paper. But I think the business model is really cool, but I think those other two levers are actually more powerful. Now, the last concept I want to sort of talk about today is this idea of external view, the external view versus the internal view and base rates. Now, for those of you who are investors, this’ll be very, very familiar. Investors talk about this stuff all the time. But when we look at, let’s say, Pinduoduo, here’s a… Here’s how it’s described. This is in Wikipedia. Pinduoduo ranks just behind Alibaba group with close to 600 million users and recorded one trillion yuan in GMV in under five years. Getting to the same scale took Alibaba 10 years to achieve. Now, when I read something like that, the investor side of my brain starts to flash red, which is, okay, you did what Alibaba did in five years? Really? the fastest growing e-commerce site ever. That’s what we would call outlier performance, which is, the internal view would be, we study a company, we look at its financials, we take apart its strategy, all of that stuff. You get very into the sort of details inside a company, how it’s done, and the human brain tends to significantly overvalue that type of information. And we do just tend to think that way. We think in terms of stories and our own personal experience in companies, as opposed to taking the external view, which would be looking at an entire industry, looking at an entire economy, and looking at all the companies and seeing how they all do in sort of groups, like what is the standard performance of a restaurant? What is the standard performance of a factory? And you develop these sort of base rates, these baseline rates for certain industries. And that’s another way to look at the world. And usually if you’re an investor, you wanna do both of those. You wanna spend some time doing the internal view, then you wanna flip and do the external view and get a sense of that. And when you hear a story of outlier performance, you know, that’s very, very rare. And you know, if someone comes up to me and they says, hey, me and my two partners, we have a dental practice and we bring in $20 million a year revenue. I’m like, No, you don’t. Not by dentistry, you don’t. Because I can look at thousands of dental practices and three dentists don’t generate 20 million in revenue. Like that is not the base rate, that is not the normal. I can draw a bell curve of performance of dental practices, get sort of a Gaussian distribution, and that’s not in it. I mean, that’s a massive outlier. So I don’t know, maybe they’re doing something else on the side, maybe they’re selling something out, maybe they’re money laundering or something. You know, it’s, but it ain’t coming from the dentistry. And if you’re an investor, you’re thinking to start a company or join a company, you can get a sense for the industry. So when you, you know, as question of a Pinduoduo and having such outlier performance, for me, that raised a big red flag that maybe I’m not understanding what’s going on. Maybe this is a different business than I thought it was. Maybe something’s going on here. And people, you know, companies do tend to smooth their performance. They tend to. shade their numbers. It’s not a matter of if companies do it, they all do it. It’s a matter of how much. And in China, Asia tends to be quite a bit more. It doesn’t mean anything nefarious is going on. When a company like you read the gap earnings in the next section is here’s our non-gap metrics. Well, guess what? The non-gap metrics always look better than the gap metrics, right? It’s a way of smoothing things over, making it look nice. You can see people sort of let’s say movie theaters in China, these have movie releases and every Friday and the new movies would come out in China and all the studios, the production houses would hire people by the thousands and thousands to go sit in seats. So that the next morning they release, hey on the news, last night this movie opened and it was number one. Okay, why? Now, if one company does it, the other companies have to do it, right? Because if you know your competitor’s doing it and you have a movie opening and they do it, you kind of have to do it. So a lot of this is institutional imperatives, institutional pressure. Then there can be a spectrum of mild smoothing all the way out to luck in coffee, let’s say. So outlier performance, I immediately start looking for stuff like that. Another thing that kind of got my attention with this company, and this is not really specific to Pinduoduo, but this is a common sort of thing I look for. If I hear the story of outlier performance, usually people want to know why. How did this happen? So you get Lambs Armstrong, which is, you know, he wins the Tour de France four times. Everyone goes, oh my God, that’s amazing. No one’s ever won it four times. And especially after he had cancer, that’s crazy. However, that’s amazing. And then you start to get told the superhuman explanation, which is this guy is superhuman, you gotta understand. And there’s literally new segments like this where it’s like they film Lance Armstrong running on a treadmill, and they have these machines hooked up to him and they show you that like, look, his heart is abnormal. It can pump more blood per pubic centimeter than any heart on the planet. They start giving you a superhuman explanation for outlier performance. Now looking back, it’s kind of obvious. It’s like, well, he was cheating, right? He was taking steroids. That’s a much more likely explanation for outlier performance than, oh my God, this person’s got a heart that pumps whatever, whatever, right? So you kind of keep a heads up when I hear the heroic founder, the heroic CEO, the super humans that explains the performance, okay, another little alarm goes off in my head. Another couple of red flags I always keep an eye out for. Anytime people are giving the customers or the investors exactly what they wanna see. You know, the movie theater thing is because everyone knows that when people decide to go to the movies on Saturday, Sunday, they always, you know, it’s very often you look at what came out on Friday and did well. So the movie studios are showing people what they wanna see, which is always a big hit. There’s a lot of Chinese companies in particular that have gone public, especially in the United States, where they’ve shown the Western investors, institutional and retail, exactly what they wanna see, which is rapid growth. So you see these companies going public, you know, whether they’re digital or back in the days of the China hustle, you know, you saw these huge growth stories. They didn’t have any cashflow, they didn’t have any earnings, but man, the growth. And that’s exactly what these investors wanted to see. And that’s what Luckin Coffee showed. They showed amazing growth. 200 outlets year one, 400 outlets, or sorry, 4,000 outlets year two. They were showing a growth story to the people who really wanted to see growth. This is what Bernie Madoff showed to his investors. Stable dividends and returns year in and year out, like clockwork. Because he knew that’s what they wanted to see. Okay, so you kind of think, okay, what do the investors want to see? And is this, you know. Okay, growth coming out of a Chinese company makes me suspect. Other things to keep an eye on, an association with famous people, social proof. When you say, look, I don’t understand this, this is Theranos, it’s some diagnostic equipment lab company in Silicon Valley. I don’t really understand what they’re doing, but you know, George Sulz is on the board and all these famous people are on the board. So it must be okay. They associate themselves with famous people. That’s another one. And… You can really see those four with Pinduo Duo. Doesn’t mean anything’s wrong. Doesn’t mean they’re doing anything. But it got my attention. You can see the outlier performance story. You can see the heroic founder, the superhuman founder story being told. Now that could just be media relations because they would do that anyways. You can see the massive growth story, which is in e-commerce, which is exactly what international investors want. And you can hear the association with other famous founders in China and Warren Buffett and all this. Those associations are being made too. Okay, that’s one, two, three, four. That got my attention. And there are a decent number of people in China who are wondering what’s up with this company. Nothing, there’s no smoking gun or anything, but people are kind of wondering, like is there something, are they shading a little? Are they shading a lot? How much of this is what? You hear this question a lot. Now the one that did really get my attention was the management changes. Because in the last couple months, the CEO has stepped down legally from the PRC position, still in control of Caymans, but the PRC company is no longer legal representative, he’s no longer technically CEO. And that one was really quite strange. Like, why would a CEO founder step down after five years? That’s not common. I can’t think of any other company in the middle of this massive growth, because their growth in the last 12 months has been amazing. Five years, really? And middle of massive growth and you’re stepping down? And you know, that’s odd. Well, what’s the explanation? And they gave an explanation that was totally like, oh, family and the next generation of leadership and blah, blah, blah. None of it was terribly convincing. And then it’s like, you step down as CEO in the middle of a COVID pandemic? Why in the world would anyone do that? I can’t think of a single CEO that stepped down in the midst of all of, why not wait six months until this is over? Bob Iger stayed in Disney to see it through to the end, right? Why in the world would any CEO step down in the middle of COVID? That makes no sense to me at all. And I’ve yet to hear an explanation that makes any sense at all. So anyways. I thought I would bring that up, not necessarily to point the finger, because I don’t actually know what’s going on. And I think it’s a very cool company to study from a strategy perspective. And that’s kind of the nice aspect of what I do, is I’m looking for strategy lessons, digital strategy, digital transformation, things like that. And you can find those, you know, no matter what. So the lessons are very valuable. It’s a great company to study. It’s really cool, actually. A lot going on, but I did want to mention that, look, there are some questions floating around about this company. And we’ll see what’s what in the future. The truth always comes out eventually, so we’ll see what’s what. And I thought it was a good opportunity to bring up this idea. Look, you really do want to take the external view. You want to think base rates. Don’t get too sucked into how cool strategy can be, because I think strategy is really cool. I think what Pinduoduo is doing in e-commerce. is super interesting. But that’s also a bit of a weakness because I think it’s cool. So you kind of pull your eyes up and you look around and anyways, that’s a good concept to keep in mind. External view and base rates, that’s the last concept for today. So that’s it for this week. I hope that was helpful. Pretty cool company overall. And yeah, we’ll see what happens next. Oh, also thank you to those who sent me ideas for where to travel. I… sort of asked that a couple weeks ago, because I’m eager to get back on the road. And I asked for sort of ideas, and people sent me some really cool locations to think about, so that was very helpful, I appreciate that. And especially also those of you who sent me, or did surveys and sort of gave some feedback on the course and what’s good and what sucks, that’s really helpful and spending a lot of time working on that right now. But other than that, it looks like I am trapped here for at least another couple weeks. I’m thinking of heading down to the islands in the south of Thailand in a couple of days. Just shake things up a little bit. Although I did just, I just started playing Grand Theft Auto, which I had never played before. Man, that just wiped out an entire day. Like, it was really, that game is just the best. It’s, yeah, so that kind of killed my Saturday, unfortunately, but yeah. Apart from that, if you have any suggestions for video games, please let me know. I’m just, I’m really enjoying this. I’ve been traveling so much. I haven’t been able to play a lot of these. So I’ve been kind of exploring different games. I did, you know, Star Wars and Grand Theft Auto and Call of Duty. If you have any suggestions for PS4 games, the one I want to get is Ghost of Tsushima. That’s probably the next one I’m going to get. But yeah, any suggestions would be great. Grand Theft Auto is just crazy. I don’t know who thought that game up, but I’d like to hang out with that person for a while. Anyways, okay, that’s it for me. Thank you so much for listening. I will talk to you next week. And for those of you who haven’t subscribed, go over to jefftowson.com, sign up there. There’s a free 30-day trial. And I will talk to you next week.