Grab, Gojek and especially Shopee are really getting international attention now. As I’m writing this, Sea Ltd is at +$125B market capitalization. SE Asia has really arrived as a tech market.

The investor who always comes to my mind when I think about these companies and SE Asia is Tom Russo. He has been investing in emerging markets for +30 years, mostly in consumer brands. And he is very good at capturing value across lots of different developing economies. This is not a China or India situation, with one big common market. Russo invests in companies like Nestle that capture value from rising consumers in lots of smaller developing economies. And that is how I see investing in Sea and SE Asia.

Intro to Thomas Russo

Thomas Russo is an investor in the mold of the Warren Buffett and Philip Fisher-style value investing. He graduated from Dartmouth College in 1977 with a B.A in history. He later went on to graduate from both Stanford Business and Law Schools (JD/MBA) in 1984. So he clearly has some serious intellectual horsepower.

I assume it was at Stanford that he became a Buffett-style value investor. He studied under Professor Jack McDonald, who was the West coast academic guru of value investing. This is in contrast to Ben Graham, was the New York value investing guru. Graham’s style of value investing shaped young Warren Buffett and many others. Jack McDonald was a West coast academic in the style of Philip Fisher, whom he taught about . McDonald taught over 10,000 MBA and Executive Education students over a 50-year career at Stanford Graduate School of Business. Charlie Munger was a big fan.

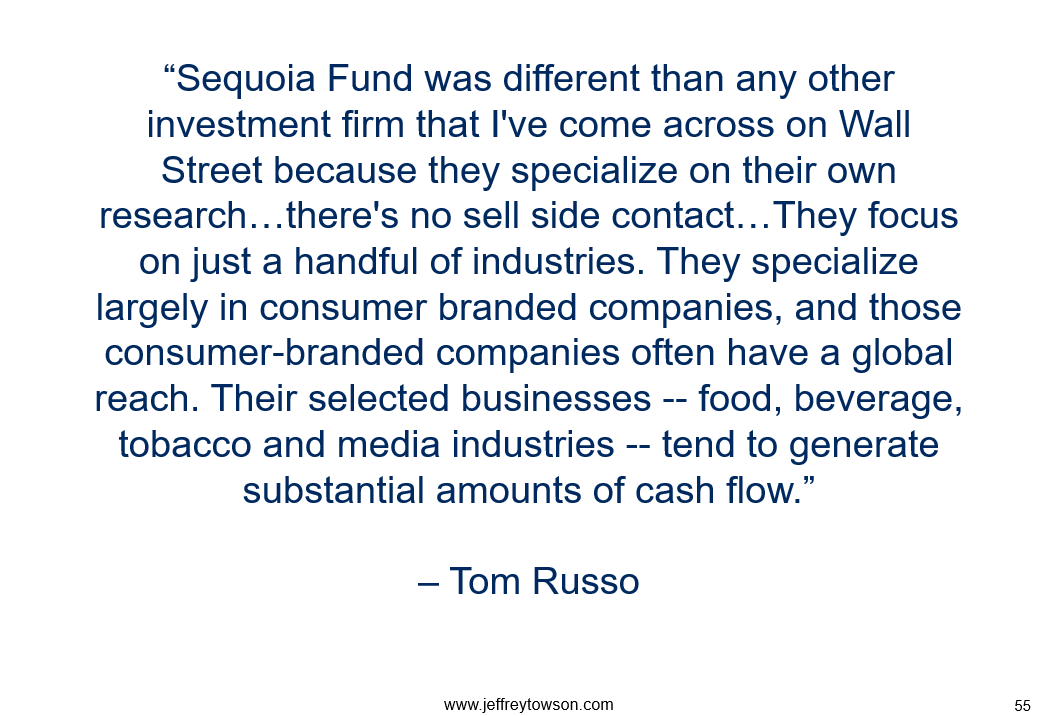

So it’s not surprising that Russo went from studying under Jack McDonald to working for Bill Ruane at the Sequoia Fund in New York. Sequoia focused almost entirely on consumer products such as alcohol, beverages and tobacco. And it had a value approach that Bill Ruane learned from Ben Graham, as a classmate of Warren Buffett. When Warren Buffett closed his original Buffett Partnership, the only mutual fund he recommended to his clients was Bill Ruane’s Sequoia Fund. Tom would end up working for Sequoia from 1984 to 1988.

In 1989, Tom became a partner at Gardner, Russo & Gardner in Pennsylvania – where he would go on to build a great track record. By 2017, Russo’s portfolio had grown to +$13.5 billion (through separately managed accounts and partnerships).

However, like Sequoia, Russo has always focused on a narrow range of consumer products. These industries historically were food, beverage, tobacco and advertising-supported media. So he owns companies like Nestle, Diageo and Marlboro. And he holds them long-term. Advertising has been traditionally critical for beverages, tobacco and food – but this has changed due to the Internet and other factors. He doesn’t seem to focus on advertising much anymore.

So why these sectors?

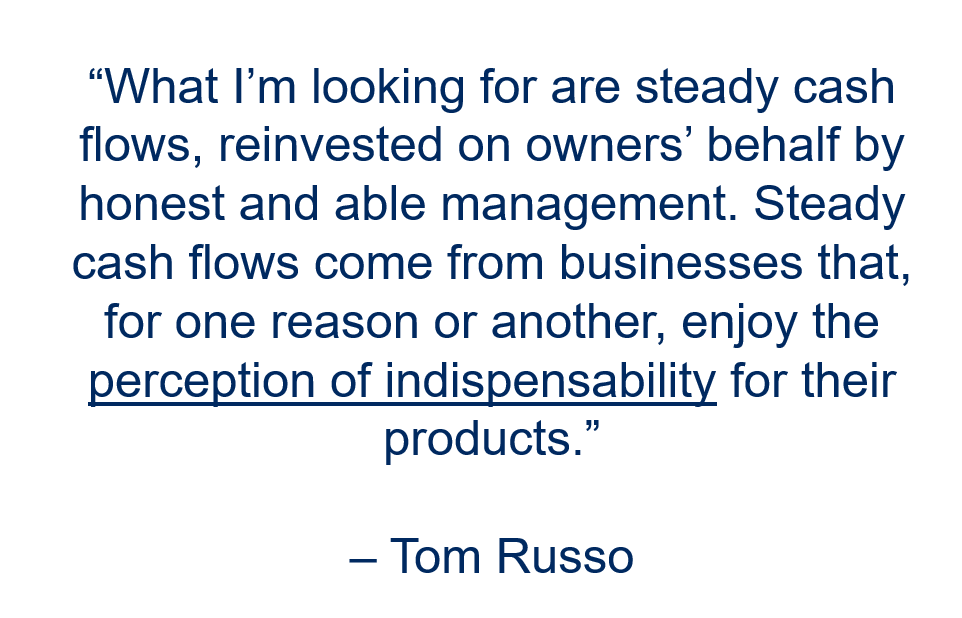

Because a small number of industries have “historically proven sustainable amounts of net free cash flow”. He thinks they have superior economics and just throw off more cash flow.

- He looks for companies with strong cash-flow characteristics. His portfolio companies tend to have strong balance sheets and a history of producing high rates of return on their assets.

- His goal is absolute return rather than a relative return.

- His long-term investment objective is compounding assets between 10-20% per year without great turnover, thereby realizing a maximum amount of realized gains and net investment income.

- His challenge is finding these great companies at reasonable or bargain prices.

So he is all very similar to Buffett. He focuses on long-term compounding of value.

“I consider myself to be a farmer—not a hunter. And I think most people on Wall Street are hunters. They like to fell big beasts and I’m very comfortable planting a few rows and just tending to them carefully.” – Tom Russo

Russo Goes for Developing Consumer Spending + Western Governance

So Russo was not always a developing economy investor. He was doing beverages and household staples in the USA – but he began going international in the 1980’s. He cites several reasons for this.

- Foreign companies had emerged as competitors in food and beverages. So studying them was required.

- The ability to obtain information about foreign companies was increasing.

- Company prices in the USA in the 1980s were inflated due to lots of leveraged buy-outs at the time.

- Foreign companies in developing economies were cheaper.

So he really was one of the first value investors to focus on developing economies and emerging markets. And he did something very clever.

He focused on Western-based companies that had reliable management and rules-based governance – but which were mostly capturing value in developing economies. He split the question. He wanted to capture the rising discretionary spending in the emerging markets. But he wanted to avoid the management risk, limited rights and poorly developed governance. So he bought companies like Nestle, which is based in the EU but makes most of its money in developing economies. He bought Bic (pens, lighters, razors), which is based in France, but sells all over the world. He focused a lot of family-owned businesses in Europe.

It was a clever strategy to reduce the risk of emerging market management and governance while still capturing emerging markets consumer growth.

I’ve looked at quite a lot of his investments over the years. And read a lot of his comments. From this, I think he has 4 investment rules. There are certainly lots more than this. But I think these are particularly helpful when looking at SE Asia.

Russo’s 4 Investment Rules (In My Opinion)

So let’s say he is looking for “globally great companies” that capture the rising discretionary spending of the developing world – and that have Western-level management and governance practices. That’s a simplification but useful. Then I think 4 rules jump out.

Now, those are pretty common. But when you think about them in terms of developing economies, they have a different meaning.

For example, Russo explains having a “global brand” as:

“My ideal business typically owns strong brands which address the needs and wants of developing-market consumers who are growing rapidly in number and in purchasing power. Those brands create the impression in consumers that there is not an adequate substitute, which makes them aspirational and affords their owners valuable pricing power.” – Tom Russo

He use the terms “indispensable” and “no adequate substitute” all the time.

For #2 on re-investment, he talks about companies that have long investment runway in developing economies.

“ The best way I’ve found to participate in the growth of developing markets is through European companies whose brands have been present but unaffordable in those markets…and whose managements are willing to redeploy Western-market cash flows into the expansion of those brands in the developing world, where the tastes already exist, the preferences already exist, but affordability hasn’t.”

That’s really interesting. He likes companies that have long been present in these countries but unaffordable for most consumers. It’s an interesting type of legacy branding.

But I think #3 and #4 are the real insights.

“Good management” in this situation means being smart and responsible with cash flow. It means management that thinks like a long-term owner and not a short-term manager. It turns out this is critical when looking at these types of companies. He likes companies with strong cash flow characteristics. That’ good. But it also means management can do a lot of dumb things with that cash. Lean and struggling companies can’t really be irresponsible with cash. They don’t have enough. They can’t buy planes and jump into bad businesses. They can’t do empire building.

It’s always the successful companies with good cash flow that have CEOs that do dumb stuff. It’s one of the big risks of these types of companies. They make a lot of money and then management just flushes it away. I think about Baidu this way.

So Russo focuses on family-owned companies.

- “As an investor in businesses, which generate enormous cash flows, my single most important issue to get right is what management will do with cash flow through reinvestment.” – Tom Russo

- “Management must continue to think of the owners when they reinvest and not reinvest in a way that ensures that management can own bigger cars or afford other luxuries. “ – Tom Russo

- “The best businesses are very personal. It’s all about the culture, the people, and the leaders. “ – Tom Russo

- “It doesn’t require family ownership to find managers who care about their company’s future beyond them, but it is even more rare without it.” – Tom Russo

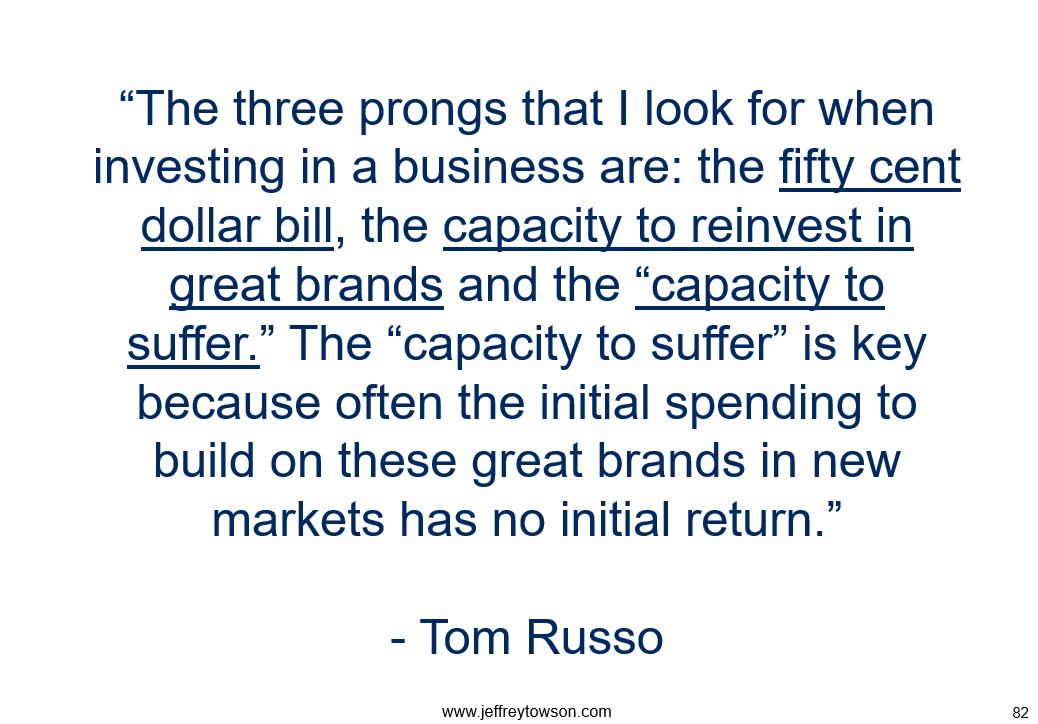

And that brings us to the point for today, which is the “capacity to suffer” (his 4th point).

Shopee and the Capacity to Suffer in SE Asia

Look at some of Russo’s quotes on “capacity to suffer” below. And think about what it takes to build a consumer-facing business across the many countries, cultures, regulatory environments and islands of SE Asia.

- “Jean-Marie Eveillard used to talk about the importance for investors to have the “capacity to suffer,” and I’d argue that same capacity to accept short-term pain for long-term gain is critical in management.” – Tom Russo

- “Many companies will try to invest smoothly over time with no burden on currently reported net income, but the problem is that when you are trying to invest in a new market, smooth investment spending really doesn’t give you enough power to make an impression. You end up letting in a lot of competition that will drive down future margins.” – Tom Russo

- “…the things that are required to pull more consumers towards your product are very expensive. In the process of those upfront structural cost investments, whether they’re investments in working capital, in plant and equipment or whether investments of the income statement and advertising, promotion, you’re going to end up burdening your current reported profits.” – Tom Russo

It’s rare for management to actually do this. They saw they will but most like to smooth their earnings. They don’t want to shock their investors with big drops in earnings. They prefer to make slow, steady investments in areas like distribution and marketing. But what Russo is saying is you really have to do big upfront moves to build a market presence in a developing economy. You are going to have to move big. It is going to hurt in distribution costs, marketing costs, working capital and operating profits.

- “Wall Street rewards a high conversion ratio. Wall Street rewards a low working capital as a percent of sales. In the case of those companies like Nestle, you’re supposed to invest in working capital because the route to market requires that the retailers have funding so they’re not out of stock. It’s a very difficult process to stock a traditional channel. And the last thing a company like Nestle would want to do is starve that channel of capital. It’ll show up on higher receivables, ultimately.”

- “If there’s one lesson I’ve seen Warren take advantage of so well over the years, it’s the profits that come and the wealth that’s driven long term by companies able to take the short term burden on reported profits.”

Now, imagine doing that across 6-8 developing economies in SE Asia?

What jumped out at me looking at Sea Limited and Shopee in 2016-2017 was how much management was willing to crater the attractive financials of their gaming business. They went big into ecommerce and their financials went into the toilet. It is now paying off but it was impressive. I wrote about that in:

Shopee now appears to be doing the same thing in Mexico and Brazil. They appear to be moving across lots of new developing economies the same way they did in SE Asia. And the same way Diageo, Nestle and other Russo companies have been doing for decades.

That’s most of what I wanted to cover today. This entire approach, which Russo has been working on for +30 years, seems really appropriate for ecommerce companies moving across lots of smaller developing economies. Sea and Shopee for sure. Maybe Delivery Hero?

A few last quotes.

- “For me it’s all qualitative and contextual. Once you begin to research an industry, you have to survey the entire landscape to understand it, from the competitors within the industry to the competitive threats from outside the industry. Ideas naturally flow out of that process.” – Tom Russo

- “My research is people intensive: meeting with management of the companies in a category, speaking with market participants about who has competitive advantage and how the distribution system works.” – Tom Russo

Cheers, Jeff

——

Related articles:

From the Concept Library, concepts for this article are:

- Capacity to Suffer

From the Company Library, companies for this article are:

- Thomas Russo

Photo by Mufid Majnun on Unsplash

———

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.

Fu Ming

August 21, 2021 at 7:43amThanks so much for introducing another Investment giant and his approach. Super interesting.

What Tom Rusou said was so true even for China to probably 5 years ago, when some domestic brands only started to challenge the dominance by the foreign brands. Brands that came to mind are Nike, P&G, and Starbucks. While Nike and P&G have been challenged now, Starbucks is still pretty much the only game in town.

jtowson

September 1, 2021 at 9:15amTom Russo has a significant position in Alibaba. He wrote about it in the recent investor letter.