I recently wrote about Shein and how they are increasing on rate of learning (plus low prices). That article is here. And I characterized their rapid updating of their site (adding +1,000 new products per day) as “retail at the speed of algorithms”.

However, there are other types of rate of learning. One is when a company is good at introducing major new products on a regular basis. that is what Steve Jobs did with the iPod, iPhone, iPad and so on. I call that type 2 rate of learning. And I think you can definitely see that in some of the digital giants, especially Tencent. Take a look at Tencent’s product history.

- QQ instant messenger (1999).

- QQ Live – Peer to peer streaming media

- QQ Show – avatars and such

- QQ Player – media player

- Qzone, a social networking site.

- Tencent Traveler, a browser.

- com, a C2C auction site (2006). Now part of JD.com.

- Multiplayer online games.

- Tencent Weibo.

- Tencent Weiyun, a cloud storage service.

- Didi Dache Taxi.

- Tencent Music and music distribution (2014).

- Tencent Pictures (2015).

- Virtual Reality Headsets (2017)

And that is not even close to the whole list. They are actively exploring and exploiting opportunities in their business. Compare that to Facebook and Airbnb, which really have not changed significantly in +10 years.

When Does Rate of Learning Type 2 Become a Competitive Advantage?

Compare Apple in 2000-2010 to Coca-Cola.

Apple under Steve Jobs had a clear ability to repeatedly:

- Launch new products.

- Capture new markets.

- Improve old products.

This type of company performance could be put under rate of learning or sustained innovation. I tend to put Elon Musk more in the innovation category, given his continued engineering breakthroughs. I tend to put Apple under Steve Jobs in the rate of learning category as he was mostly adapting existing technologies into new consumer devices. You could consider this customer-facing innovation.

But the question remains: when does this type of operational activity become a structural advantage?

When does it become an ability that is going to create more and more value over decades?

Which brings us to Philip Fisher, often referred to as the father of growth investing. From his book Common Stocks and Uncommon Profits, we get a good picture of how he invested in tech-related companies with the ability to do Type 2 rate of learning over long periods of time.

Philip Fisher, the First Tech Investor

Fisher invested for 75 years by targeting companies with the potential for long-term growth related to technology. Specially, he wanted the type of long-term growth that required repeated new market and products. Fisher invested through the Great Depression, World War II and the American post-war boom. He became a specialist in manufacturing companies driven by technology (electronics, chemistry, metallurgy, etc.). His timing was both horrendous and fortuitous.

In 1927-8, 20-year old Fisher was in the 3rd class at Stanford Business School. The class had 19 students. The class ahead of his had 9 students. He dropped out in 1928 after the first year to take a job in investment and became a statistician (later renamed security analyst) at the Anglo-London Bank. And in 1929, Black Tuesday hit and the Great Depression began.

“In 1929-33, we went through four years of such economic hell that people who went through it have been psychologically scarred ever since. You saw people who were well-fixed lose jobs, people who had been wealthy going through their homes taking out every light bulb except one in each room. I knew a manufacturing executive who went to work as a watchman, and his wife took a job cleaning and cooking.” – Philip Fisher

In 1931, Fisher established his own firm Fisher & Company. He said he started his company that early in life because there were no jobs. So he started in a tiny office. No windows. Just a space for a desk, two chairs and a phone. In 1932, he made $2.99 per month. In 1933, he made $29 per month, which was about same as selling newspapers on the street.

But he was able to meet people with money as they had lots of free time. One investor told him later “listening to this guy will at least occupy my time…If you had come to see me a year or so later, you never would have gotten into my office.”

But his timing was fortuitous. He was molded by the Great Depression to only invest in the very best companies. Those that could survive massive adverse events. Those with competitive advantages. And that was the scarred mentality he took into the beginning of the technology age in Silicon Valley.

Post-War American Manufacturing Began to Combine with Technology and Research

In 1929, when Fisher started investing, only a half dozen US industrial corporations had significant research departments. Radios and cars were the newest technologies of the time. This was well before television, most communications, transistors / electronics and semi-conductors / computers. But things were starting to change.

- In 1953, US corporate spending on R&D was $3.7 billion.

- By 1956, it was $5.5 billion.

- In 1957, it was $7.3 billion (according to Fisher).

Technology and research began to be incorporated into corporate America, and into manufacturing in particular. It had become a driver of new products and sales.

- Radios started to be put into cars (i.e., Motorola).

- Cathode tubes gave rise to color television.

- Transistors gave rise to electronics (i.e., Texas Instruments).

- Semiconductors gave rise to computers (i.e., Hewlett Packard).

Technology began to be incorporated into the suppliers of manufacturers, then into manufacturers and then into just about every other company.

Fisher became a specialist in innovative companies driven by research and development. Mostly in manufacturing. Like Ben Graham, he had an investment approach that well suited to the turbulent era in which he lived. Ben Graham bought really cheap companies, got out fast and avoided the frequent booms and busts of his time. Fisher bought the best companies that could cruise over the turbulence.

Fisher was one of the first, if not the first, to develop the thesis that growth stocks have identifiable characteristics that make them different from ordinary stocks.

- They are qualitatively different. (Ben Graham was almost entirely quantitative in analysis).

- Some are well-positioned to grow in profits over decades.

- They are well-defended against downturns and competition.

“it is as powerful to invest in companies adopting technology as those creating it.” – Philip Fisher

Fisher said 1954-1969 was a “magnificent time”, with significant advances in his portfolio focused on electronics, metallurgy, chemistry and machinery industries. And in 1955, Fisher first invested in Motorola, one of the first mobile telecommunications companies. It grew 20x over 21 years and Fisher held the stock until his death in 2004.

Motorola was a Steve Jobs-type 2 learning company that continued for decades. So how did Fisher spot it so early on?

The Rise and Rise of Motorola

Founded in 1928, Motorola (then called Galvin Manufacturing) pioneered mobile communications with car radios and public safety networks.

- In 1930, they introduced the Motorola radio, one of the first commercially successful car radios. Founder Paul V. Galvin created the brand name Motorola for the car radio, linking “motor” (for motorcar) with “ola” (which implied sound).

- In 1940, Galvin Manufacturing Corporation developed the Handie-Talkie portable two-way radio. This handheld radio became a World War II icon.

- In 1969, Motorola made the equipment that carried the first words from the moon.

- In 1983, Motorola launched the first commercial handheld cellular phone.

When Fisher purchased the stock, Motorola was just a radio manufacturing company and was not recognized for strong R&D or company management.

“As for Motorola, Wall Street is just beginning to see how good management really is. In the recent semiconductor depression, it was the only major company to earn subnormal but not insignificant profits.” – Phil Fisher

Motorola had the pattern I look for with Type 2 rate of learning as a structural advantage.

- I frequently launched new products, captured new markets and improved old products.

- This created new revenue streams.

- The new products and their revenue streams were protected. They did not decline as competitors copied them.

- So each new revenue stream increased the overall revenue going forward.

“If the growth rate is so that in another ten years the company might well have quadrupled, is it really of such great concern whether at the moment the stock might or might not be 35% overpriced?” – Philip Fisher

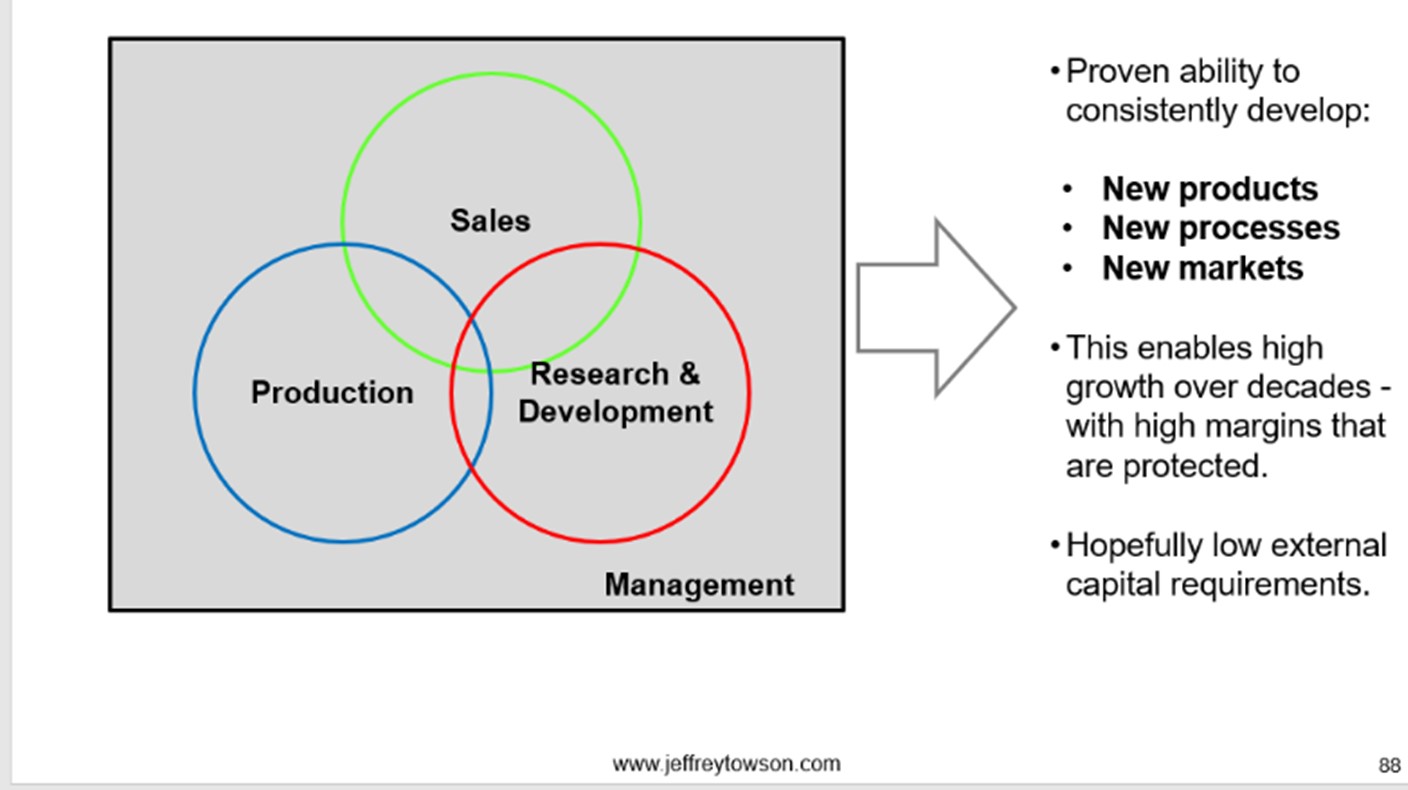

The trick is to identify companies capable of this sort of pattern. And to know when it has reached the level of a structural advantage. Fisher’s did this with analysis that was mostly qualitative – focusing on the intersection of management, research and development, manufacturing and sales capabilities. You need all of those right to get repeated product creation and launch.

Fisher had specific questions for each of these capabilities. Above average research and development capabilities (relative to competitors) were the starting point.

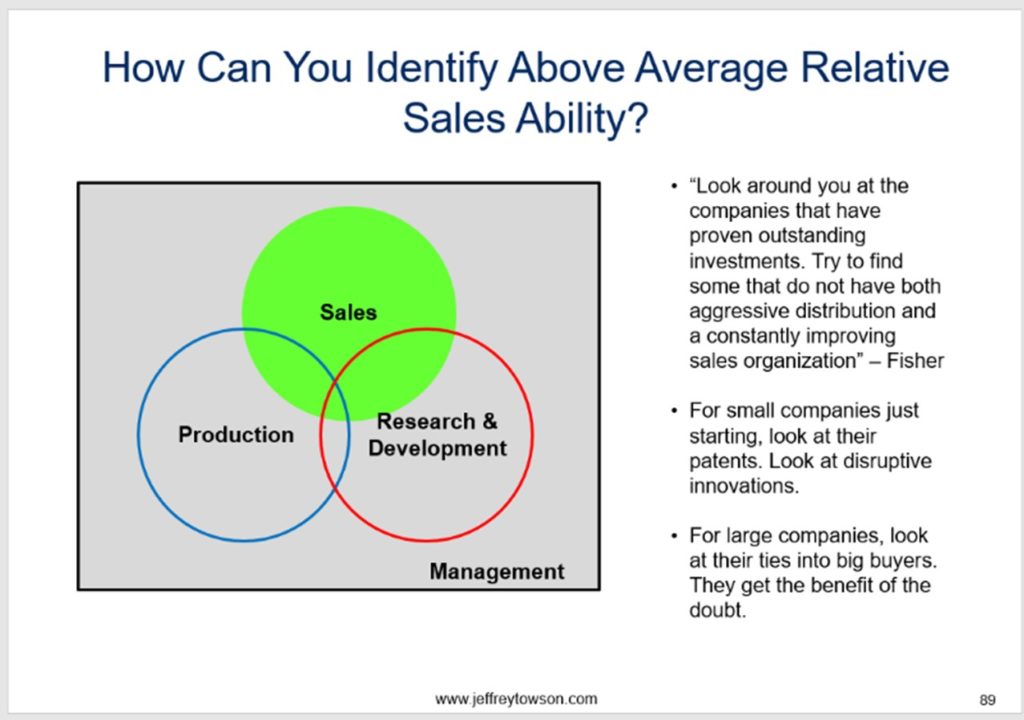

He also looked for a sales organization of above average ability, relative to competitors.

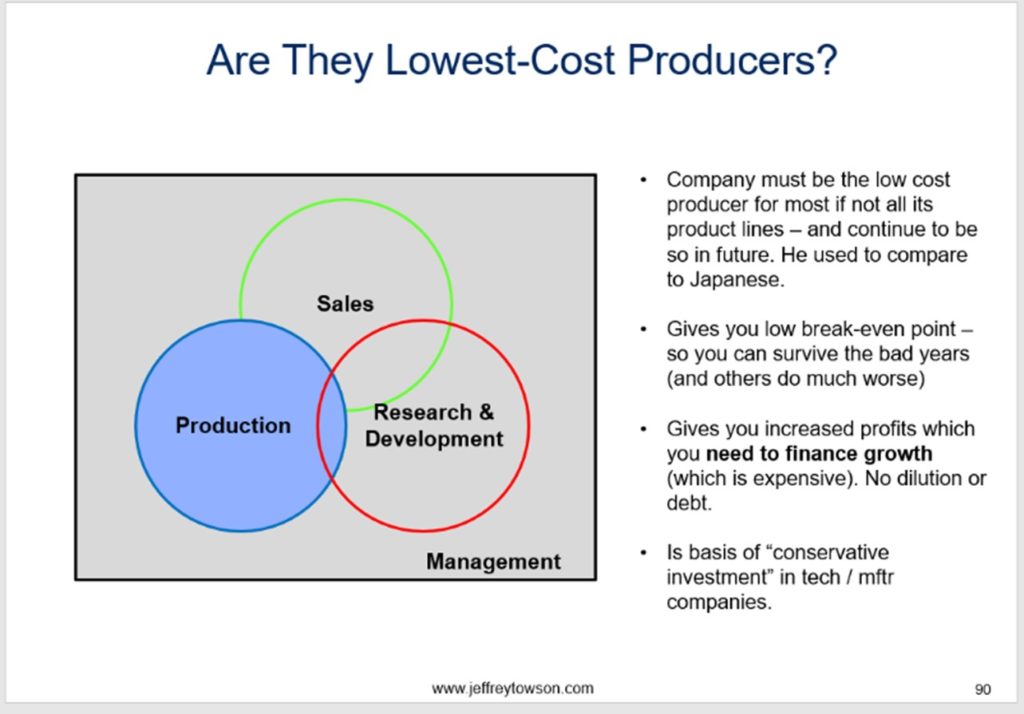

He looked for production and manufacturing abilities that put the company in the lowest cost position, relative to competitors.

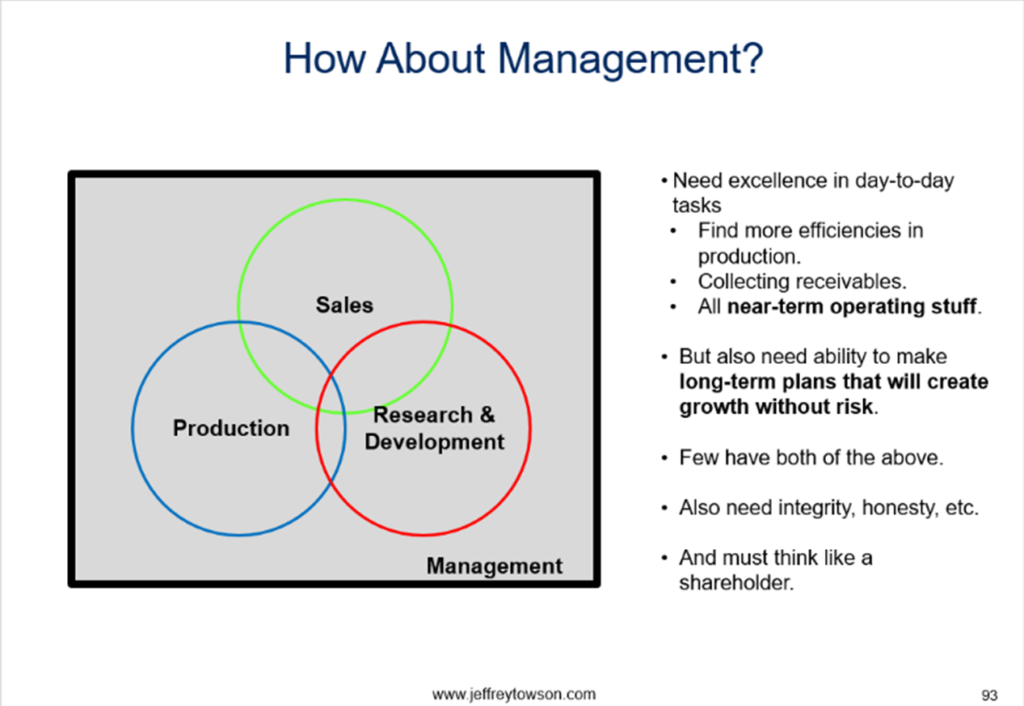

And all this required management that was able to coordinate these functions effectively.

You can see how all four of those capabilities are required for continued new product launches in manufacturing related fields.

- The R&D is required to be better than competitors.

- The sales force needs to be able to move the products.

- The manufacturing needs to be the low cost player.

- Management needs to be able to make all this happen.

But do you really need all 4 with Tencent?

There is no manufacturing. It’s software. And sales isn’t as necessary because they have a big captured user base. It mostly comes down to assessing their R&D and management. How are they different than Airbnb, Uber and Facebook?

I recently wrote about Dingdong and how they probably need to pivot to a more profitable service. Are they capable of this type of rate of learning?

The question Fisher would ask to Dingdong is probably:

***

Fisher spent his career working alone in an office building in San Mateo, Calif., south of San Francisco. There was a small outer office where his secretary sat, a couple of filing cabinets and a phone.

He also taught at Stanford Business School. And he authored three books, one of which became the first investment book on the New York Times best seller list. His first book Common Stocks and Uncommon Profits came out in 1958. Warren Buffet says he is 85% Graham and 15% Fisher. He contacted him after reading his book.

After 75 years of investing, Fisher, died in 2004. He was probably the last major investor who witnessed the 1929 market crash.

That’s it for today. This is my last week in Rio so I’m starting to pack up.

Cheers, jeff

—–—

Related articles:

- My 9 Investment Questions: Part 1 (Asia Tech Strategy – Daily Update)

- Shein and How To Compete on Rate of Learning (Asia Tech Strategy – Daily Lesson / Update)

From the Concept Library, concepts for this article are:

- SMILE Marathon: Rate of Learning (Type 2)

- Competitive Advantage: Rate of Learning

From the Company Library, companies for this article are:

- Motorola

- Tencent

- Philip Fisher

——–

Fu Ming

July 20, 2021 at 11:31amVery informative. I had never heard of Philip Fisher, the exact name, until this article, while I had heard of “growth investment.”

Besides Tencent, Google is perhaps another example of the type 1 innovation company, just like Tencent? In that sense, perhaps the key difference between type 1 and type 2 is really software vs hardware, where the former allows real-time continuous innovation and the latter requires quantum-like cadence?

And if we try to go back to “first principles,” where do the four distinguishing characteristics of growth companies, ie, excellent management, sustained innovation, outstanding sales and rigorous cost controls, come from? I suppose people? Especially the founders?

Speaking of Buffet vs Fisher (proxy for Value vs Growth), I wonder which one produced higher annualized returns over their investment lives? 🙂

jtowson

July 20, 2021 at 10:23pmI think the problem with Fisher is there just aren’t that many of these companies. he found like 1-2 every decade. Buffett has a much bigger pool of companies.

Fu Ming

July 21, 2021 at 4:33amall the more powerful? just imagine if one had put all his/her investment in Tencent or Netflix over the last 3 decades.

Diversification or Diworsefication? To borrow a term from Peter Lynch. 🙂

jtowson

July 21, 2021 at 10:43pmha. that’s a good phrase.