This week’s podcast is about Coinbase, which has been coming back in terms of share price and revenue.

You can listen to this podcast here, which has the slides and graphics mentioned. Also available at iTunes and Google Podcasts.

Here is the link to the TechMoat Consulting.

Here is the link to the Tech Tour.

Here are the three lessons:

Lesson 1: Don’t get seduced by stories and cool business models.

Lesson 2: You live and die with the customer. Bitcoin + Coinbase was a 10x solution to a massive problem.

Lesson 3: You can’t disrupt the government. Or State Owned or State-Directed Enterprises. Unless they approve.

Here are the mentioned slides.

Cheers, jeff

- Coinbase and the Tech Uncertainties of Platform-Protocol Hybrids (3 of 3)(Tech Strategy – Daily Article)

- After the Fall of Crypto, Is Coinbase an Opportunity? (Tech Strategy – Daily Article)

——

Related articles:

- How to Think About Web 3.0 Business Models (1 of 2) (Asia Tech Strategy – Daily Article)

- Platform-Protocol Hybrids and Why DeFi is the Center of Web 3.0 (2 of 2) (Asia Tech Strategy – Daily Article)

From the Concept Library, concepts for this article are:

- Role of the State

- Platform-Protocol Hybrids / Web 3.0

- Blockchain

From the Company Library, companies for this article are:

- Ethereum

- Bitcoin

- Coinbase

Photo by Kanchanara on Unsplash

——-transcript below

Episode 223 – Coinbase.1

Jeffrey Towson: [00:00:00] Welcome, welcome everybody. My name is Jeff Towson and this is the Tech Strategy Podcast from Techmoat Consulting. And the topic for today, three lessons from the fall and maybe rise of Coinbase. Now, I haven’t talked about Coinbase in about a year or so. The last time I did is because the share price had collapsed down to about 50 per share, up from over 200 when it was flying high.

And I raised the question of, is this an investment opportunity? Coinbase is now up to about 150. So to some degree, the answer to that question was yes. That’s short term, let’s say. But I thought I’d talk a little bit about where it is and more specifically, I think at least what I’ve learned from watching this company rise and fallen.

It may be rising again. We will see, but I thought that would be a [00:01:00] good topic for today. I think this will be a bit short for today. Anyway. So that will be the topic. Housekeeping stuff. We have China tech tour small China tech tour. I should think of a different name for that. In November going to Shanghai, Hangzhou just, it’s just going to be a handful, a small group of people.

Pretty, I wouldn’t say informal, but yeah, a little bit, which is a change from the somewhat larger groups we’ve done this year. So we’re going to visit some tech companies, do a lot of discussion. Should be a lot of fun. If you’re interested, go over to Techmoat consulting. com. All the details, including dates and price are there.

Techmoat consulting. com. Just look for tours. You can’t miss it. Okay, and standard disclaimer, nothing in this podcast or my writing or website is investment advice. The numbers and information for me and any guests may be incorrect. The views and opinions expressed may no longer be relevant or accurate.

Overall, investing is risky. This is not investment, legal, or tax advice. Do your own research. And with that, let’s get into the topic. [00:02:00] Now, Web3 actually is pretty cool as an idea. It got subsumed as a topic because there was a bunch of fraudulent behavior. Both at the business level like FTX and many others, but also at the, the token level and the, the various coins and all of that nonsense.

There’s a lot going on, a lot of rampant profiteering and or speculation and or just flat out fraud. So that was part of it. I think the more important stuff longer term, cause that’s not uncommon in new businesses when there’s a lot of money. The more important ones are. The lack of customer adoption for most all of this stuff.

Yes, there was cool business models and a lot of cool ideas and a lot of money, but very little customer adoption outside of decentralized finance, which was mostly speculation. And let’s say Bitcoin and Ethereum. The NFTs and all of that. So there was always a customer adoption problem. [00:03:00] People weren’t using it, even at the height, very few people were using this stuff.

And then of course the government role, which has grown over the years, even though the story died down, it’s. Become a bigger and bigger issue. And that’s goes country by country, but that those are I think the bigger longterm factors are customer adoption for various products and then government role.

So I wanted to talk about a couple of concepts that I think matter and then just, Kind of what I learned from Bitcoin as a, not really Bitcoin, Coinbase, but Coinbase is mostly Bitcoin and Ethereum for all the talk. There were two couple of things I thought were valuable. Number one is a business model.

I was calling the platform protocol hybrid which I’ve written about before. There’s graphics. I’ll put some graphics in there. It’s basically a new type of business model built on top of blockchain as opposed to built on a server where we might call it a platform business model if it’s built on a blockchain Which means [00:04:00] if you’re building if you’re YouTube you’re building a platform business model But you control the server and the computer But if you’re building on a public blockchain, you don’t control then we would call it a platform protocol hybrid And I’ll talk a bit about that.

And then the other concept I want to talk about for today was just the role of the state. I think people in the West, which I’m, I’m from the West. I think they have a hard time with this question. I think when you come out of China and the Middle East and a lot of my sort of stomping ground.

This is just normal, like how to think about the role of the government and the state. And when I say state, we’re not just talking about government. We’re talking about institutions associated with talking about certain individuals, families, things like that. The state can be a lot bigger than just the guard the government apparatus.

It can be party. So the role of the state, I think, was always pretty clear in what was going on with Web3 for those of us that come out of this world. [00:05:00] Maybe not for the Westerners so much. Anyways, those are the two concepts to think about for today. Role of the state, platform, protocol, hybrid.

And those are both in the concept library, and I’ll talk about them as we go through. Alright, let’s talk about Coinbase. For those that aren’t familiar, it’s a pretty straightforward company. It was the flagship of Web3. Basically, they’re, they have a big story. But, at the end of the day, they were only doing a couple things.

You could basically buy and sell, tokens and various types of coins. So Bitcoin being the big one stable tokens, Ethereum, those were the big three, but there’s 20 or 30 others. And what they did is two things is he’s number one. They were a very good on ramp. For getting involved. And that was really, I think, still their primary roles.

So they help people get into this because you could basically transfer money from your bank account, using your card into [00:06:00] Coinbase, and then you could start buying and selling these coins. So they would say, they are a combination of traditional finance and blockchain finance technology, creating trusted and user friendly products.

That’s straight out of their. Their first financial filing and then their latest stuff. That’s how they describe themselves. Now, they have a bigger story than that from their 10K from 2023. They say, our mission is to increase economic freedom in the world. Okay. A quote, we are working to update the century old financial system by providing a trusted platform that makes it easy for our customers to engage with crypto assets.

Including trading, staking, safekeeping, spending, and fast free global transfers. That’s pretty good actually. The key [00:07:00] words are all there. Trusted. This is a lot about trust. Nobody knows what to do with these. It, crypto, they’re calling them crypto assets now, which expanded from coins and financial instruments to everything from NFTs to gaming assets, things like, but we’re mostly talking about financial aspects.

So trusted was a big deal. makes it easy for our customers to engage. That’s the easy on ramp. You put in your card, you load up some money, and then it lets you do various services, trading, staking, safekeeping, spending, and fast free global transfers. That’s pretty much most of it. Trading, obviously buying and selling.

Staking, which is for those not familiar. You can stake, if you have a bunch of crypto assets, a bunch of Bitcoin, a bunch of Ethereum, you can stake them, which basically means like you’re gonna get paid interest. It’s like putting it in a savings account and they pay you a couple [00:08:00] points of interest on that, but you can’t take it out.

They’ve changed the word storage to safekeeping, which is interesting because the term that everyone always used was store of value. Which is still the biggest use of Bitcoin. People aren’t trading Bitcoin and they aren’t using it as payment. They’re using it as a store of value. So it’s interesting.

They changed the word in their latest 10 K spending and then free global transfers. A lot of the early adoption for things like Bitcoin came out of Argentina and Venezuela and basically places where, you know, as soon as you, you got your paycheck, your currency was just being devalued by the day.

And so you’d put it in your bank account in Argentina and it would be worth nothing. Very quickly, so you would transfer it to U. S. dollars, but then the government started limiting that. So they started buying Bitcoin very early on. There’s a 21 million limit on Bitcoin, so you can’t [00:09:00] ever increase the supply.

So it makes it a good store of value. Okay, so that’s their basic description. They describe themselves as a quote critical infrastructure for on chain activities. Fine. The services that are associated with that self custody wallets, decentralized apps and services, and then open communities.

Fine. The user groups that they mostly serve are consumers and institutions who are their primary customers, people buying, Bitcoin and Ethereum and whatever. So retail users, that’s consumers. They discover trade, hold on to, various. on chain assets. Institutions, this is the area that’s been growing.

Market makers, asset managers, hedge funds. This is where FTX was really positioned. Coinbase [00:10:00] was much more of a, this is a marketplace for pretty basic using and holding. And then FTX was, you could do a lot of fancy trading and this and that. I didn’t understand 80 percent of what they were doing.

And then the other group is developers. So once you get this sort of platform, people can start to write decentralized apps that run on these things. So that’s their main user groups. Okay, so what happens with this companies? They basically had a rise and fall, and maybe they’re coming back again.

But if we look at monthly transacting users, so this is anyone doing any sort of transaction within a month. 2021, which is right when they had just gone public, 11 million monthly transacting users. 2022. This is when all the scandals happened that, the tokens got wiped out these marketplace [00:11:00] platforms like FTX and the others all turned out to be calm, not all, but a lot of them fraudulent.

And even though Coinbase was differentiated from all of those, the difference, the biggest differentiator Coinbase always had was we are not here to operate outside of the government regulations. We work with the government. So we’re gonna be the bridge between traditional finance and blockchain technology.

So we work with them. So when people lost trust in all of these decentralized marketplaces, Coinbase was, let’s say, more trusted, but even they took a hit. And I moved my, I have some Bitcoin and stuff, not a huge amount, but some, I moved it off Coinbase in 2022 and I put it into cold wallets. But I basically don’t, didn’t trust any of the platforms anymore, so they got hit.

2021, 11 million monthly transacting users. By 2022, it dropped to 8. 3. 2023, it dropped to seven. So yeah, fewer people using the [00:12:00] services at least for transactions. Now, if they’re storing their money there and not doing anything, it wouldn’t show up in those numbers. And they have traditionally said they have about 43 million, in that range, that number is a couple of years old.

Users, registered users. Okay. So that one goes down. The big number that went down was trading volume. So this would be the financial value of all the trades. So when people are doing fewer trades, it goes down. And when the price of Bitcoin and Ethereum goes down, the value of the trading volume in dollars also drops.

So they went from about, 1600 billion, so 1. 6 trillion in trades in 2021 down to 800 billion, 830 billion in 2022, and then down to 468 in 2023. So just the volume, the financial volume of transactions [00:13:00] has dropped. Okay that’s not good for them because historically, they made their money by charging transaction fees.

That’s where their revenue came from. When they went public, that was the story. We make our money with transaction fees. Okay, that’s really bad. Now what they’ve done since which is good, is they’ve shifted their revenue from transaction fees to transaction fees plus services plus subscriptions. And what does that mean?

Now that means they’ve offered a couple types of services where you can do trading without a fee, especially for institutional users. They shifted into stable coins. Stable coins are, there are crypto assets that are tied to, say, the U. S. dollar. The USDC, which is their primary stablecoin, it’s basically a digital version tied to the U.

- [00:14:00] dollar. They get revenue for that, they get rewards, they do interest income. All of that, they get custodial fees if you have a custodial wallet, which means your wallet is held by them and not by you, which is generally not a good idea. All of that shifted their revenue from transactions over to revenue that sort of just tracks how much do they have in terms of asset under management.

And that worked out quite well, actually, because if you look at their overall revenue, two things have happened since 2021 and 2023, end of year. Their total revenue, okay, it took a hit. 2021 they had about 7. 8 billion in revenue. That was their high point. It dropped by about half in 2022 to about 3.

2 billion, but then it was stabilized in 2023, again, 3. 1 billion. So they took the big hit in [00:15:00] 2022, but 2023, the numbers look pretty stable. We’ll see. So the users, the transactions continued to fall significantly, but the revenue stabilized in 2023. It didn’t move too much. The distinction between revenue coming from transactions to revenue coming from subscriptions changed dramatically.

2021, 90 plus percent of their revenue is from transactions. 2023 is about 50%. a little bit less than that, but it was about equal to what they were getting from subscriptions and service fees. So that’s, that’s pretty good. That picture looks pretty good. So this is the question is, are they on their way back?

They took a big hit in 2022. Particularly in activity of users and the value of the coins on their platform. They shifted much more to [00:16:00] subscriptions and services, which basically gets your revenue from just assets under management, as opposed to transactions. And they shifted much more into things like stable coins, as opposed to exotic, who knows what crypto.

Assets this week, that’s all pretty interesting and their share price, which I’d mentioned began, high point They were 250 at IPO something like that They dropped to 50 per share in 2022 sort of the low point, but now they’re up to about 150 so are they coming back and we’re getting I think out of the area of chaos and Volatility and now we’re looking more and more at fundamentals.

Is this a good business model and a good business? What is the government risk over the long term? What is the technological risk over the long term? I think we’re getting back to more standard business questions now that this is quieting down, which is why I thought it would be a good [00:17:00] time to look at this.

Okay, that’s where we are. So let me jump to the three lessons. Let’s call it investing or analysis lessons from all of this. These are my notes to myself. Lesson number one, don’t get seduced by a story or a business model, right? When you look at sort of psychological biases, one that people talk about a lot is story bias that People do like stories that are easy to understand.

Our brains seem to gravitate towards easy to understand stories. And so you have, Steve, Jeff Bezos was famous for talking about this. You got to ignore the story and just look at the numbers. Because we do get seduced by those. We look for simple explanations and stories in complicated information.

The strategy version of that for me is, don’t get seduced by a sexy business model. Because [00:18:00] I do. I like if a business model is really cool, I get into it and I think, Oh, that’s really neat. Look how clever that is. Look how all the pieces work together. That’s great strategy, right? It’s the same as the story bias, I think.

And I’ve actually heard Charlie Munger talk about this certain business models. He says, some people, we just get, they’re too attractive. To value investors, really cool, powerful business models. And you can be a little bit blinded by what’s going on. And I think when I read about the Coinbase, if you read the IPO filing, they tell a very big story.

I’ll read you some of the quotes. Would say, quote, like the current financial system is rife with high fees, delays, unequal access, and barriers to innovation. In many countries, citizens don’t have access to sound money, functioning credit, and basic property rights. [00:19:00] We need an economy based on common standards that cannot be manipulated by any company or country.

They were telling this big story to consumers, that you can get, like, we can address unequal banking access. They were speaking to the, there are certain countries that don’t have functioning systems for banking at all. And then there’s this other big idea of fiat currencies.

They keep printing money and devaluing your currency. They had a, they had some really big sort of. business questions that were also big political points, really, and almost emotional things. And then layered on top of that, you also had the whole web three story, which is look, in web one, all the software people created everything in the eighties and nineties, like the FTP protocols and all of the things, the internet.

The Ethernet connections that was all created by developers, but they never [00:20:00] really got rich the people who got rich were the Steve Jobs the business people who came later built power for business models and got rich and the software guys never really got rich It’s web one to web two. So Web3 is gonna be about the developers coming back and anything you write when it goes on a blockchain, you’ll retain ownership of that and it’ll be your software or your asset, even though it’s on the, on the blockchain.

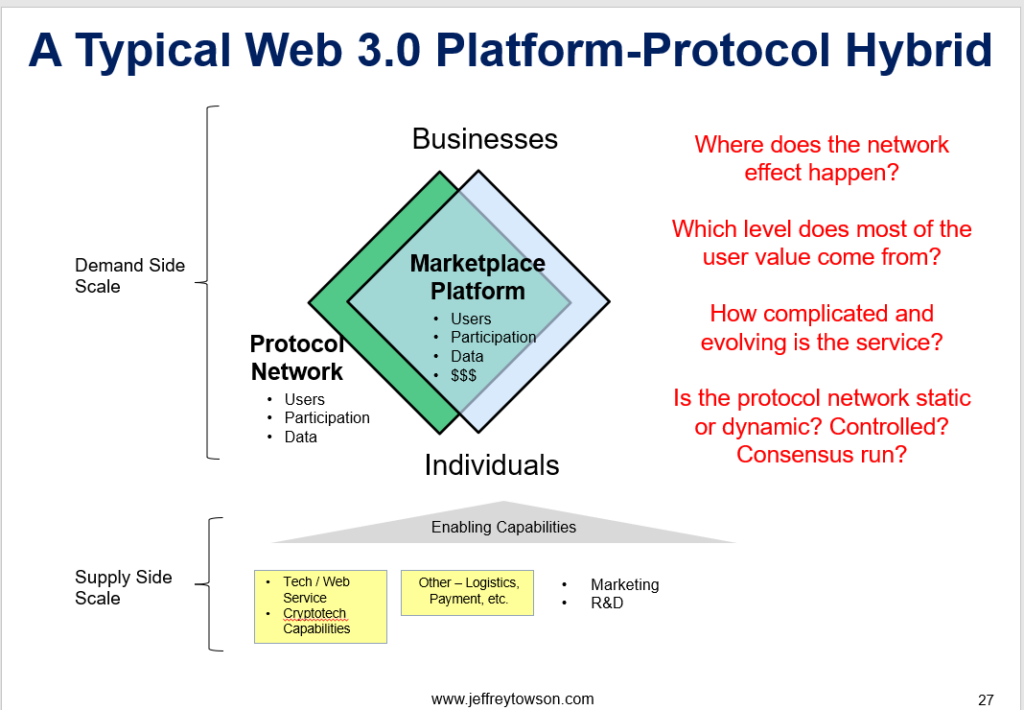

So there, there was a lot of big stories baked into Bitcoin and Web3 and Coinbase and all of that. Now, for me, the part that I think I got seduced a bit by was the business model. Now, I allude, this is concept number one for today, the platform protocol hybrid. Now, traditionally I draw these graphics all the time of a blue diamond, which is a platform business model, which is [00:21:00] in the business of connecting users for interactions.

That could be a marketplace, it could be an audience builder, it could be a payment platform. But that was generally owned as a proprietary system YouTube owns its own servers, therefore it owns all the videos that are on its servers. That people upload for free. Alibaba owns a marketplace platform. It controls the logistics, it controls the marketplace, all the data, it’s theirs.

Okay, but once you move things onto the blockchain, onto a protocol network, That’s almost like a public server. It’s like a, this is what Ethereum is supposed to be. It’s supposed to be a global decentralized computer that anyone can build apps on that nobody controls. Okay, you can build a platform business model on top of a protocol network on top of a public, decentralized, non [00:22:00] controlled computer.

And that’s what Coinbase did. Yes, Coinbase positioned itself as a marketplace business model. There are people buying coins and there are people selling coins. However, none of those coins sit on the servers of Coinbase. They sit on the protocol networks, Bitcoin being the most famous, Ethereum, and they had a bunch of others.

So really, what we’re doing It’s like we’re separating the server, all the servers that are YouTube. We’re taking them out of YouTube and putting them all over the world, and YouTube doesn’t own them. But YouTube built a platform business model that interfaces with the computer. And certain things would sit at certain levels.

The videos would sit on the public computer, which they don’t control, but the user data and the interactions would sit with YouTube on the platform. So it was a platform sitting on top of a protocol network. And there was [00:23:00] lots of interfaces between those two that let you buy and sell coins and things like that.

And I’ll put a graphic in the show notes for how I looked at that. And I thought that was very cool as a business model. And the big question that a lot of like the Andreessen Horowitz and all the Silicon Valley people were debating back then two years ago was where does the network effect sit?

Now there’s a network effect for Bitcoin. The more Bitcoin that exists, the more valuable it becomes. It’s a standardization network effect. But also there’s a network effect for the protocol network and there’s also a network effect for the platform if it’s operating like a marketplace. So you could have the network effect on one, two or three levels, maybe all three as opposed to say an Alibaba network where there’s one network effect that Alibaba owns it from top to bottom.

It was a very cool business model. [00:24:00] It had a pretty impressive network effect because we could see it at the marketplace level. We could see it at the protocol and we could definitely see it within products like Bitcoin themselves have a network effect. So all of that is really interesting. Now, is that really true?

Looking back, I think a lot of that is not true. That was my lesson. Now, there was another story with, I’ll explain that in a minute, there’s another point with Coinbase. So Coinbase was a marketplace for trading, buying, and selling coins that wasn’t a traditional platform. It was a platform protocol hybrid.

So it was on the platform level, it was at the protocol level, which they didn’t control, and then it was at the coin level. Very cool. You could also argue that there was an innovation platform they had as well, because people were going to start to write apps that would run on Coinbase [00:25:00] itself, so it would start to become somewhat of an operating system, maybe.

All of that was really interesting. Looking back, I don’t think it’s true. I really don’t. Is Coinbase really a marketplace? For a marketplace to work, you need lots and lots of buyers, and you need lots and lots of sellers, and you need lots and lots of products. If you have tens of thousands of people as sellers, but they’re only selling two products, Ethereum and Bitcoin and USDC, is that really a marketplace?

No, you need a much larger inventory of products for this to be a real marketplace. So looking back, I don’t really think this was a marketplace. I think it was closer to something like the currency office when you get off an airport and you walk out there and you can change your dollars to yen or whatever.

Yeah. We wouldn’t consider those a [00:26:00] marketplace. It’s just a, it’s a service. It’s a currency exchange service. So I don’t really think it’s a marketplace. I think at the end of the day, what they were doing was two things. I think they were providing a service that gave people an easy and trusted on ramp into Bitcoin and other crypto assets.

So easy to get on. And also there was a greater degree of trust than trying to get on MetaMask and doing some decentralized self custody wallet, which was confusing. So they provided the on ramp, they provided trust, and they did a basic currency exchange. Yeah, in a self custody wallet or a custodial wallet.

So I think it was really mostly a service business and the network effects and the powerful economics were coming from Bitcoin and Ethereum and not from Coinbase. That’s where I fell on that. If you want to read more about that, I’m going to put a link [00:27:00] to two articles I wrote about this, which are in depth about how to think about platform protocol hybrids and marketplaces and various things like that.

But that’s number of my lesson. Number one is I got seduced by the business model which is story psychology and I didn’t look at it more cleanly in terms of data. Okay. Lesson number two, you live and die with the customer, right? It’s so simple, but it’s easy to forget about, especially when you start getting into strategy and business models and all this fun stuff.

I like. How many customers do you have? How many potential customers? What’s your total addressable market? How big, how good are you on that side? Is it a 10, 10 X product? Is it 10 times better than the competitors? Is it 10 times better than what came before? How powerful is it? And most customer products are not [00:28:00] that powerful.

Most of them are moderately weak. Yeah. You need socks. Yeah. You need water. Okay. There’s a need, but it ain’t that powerful. I think Coinbase with Bitcoin and Ethereum and USDC, I think that was a 10x solution to a massive problem. I think I thought too much about the business model and not about how powerful it was as a customer offering.

And within all the story I just poo pooed they really do talk about the value to the customer. And it is pretty great, which is they provide a primary financial account for the emerging crypto economy. That’s safe. It’s trusted. It’s easy to use. And it lets you invest, store, spend, and hold basically crypto assets.

That’s pretty [00:29:00] great because it turns out there’s a huge number of people who want to have sound money that is not going to be diluted, that has Your own personal property rights and that can’t be manipulated by a company or a country. That is a massive demand in this world and they actually came up with a very clean, powerful solution to a massive problem.

Everyone is looking for where to put their money so it’s safe. Okay, Bitcoin plus Coinbase, and you could add in USDC as well. That is a great solution to that problem, and they made it easy, convenient, trusted, safe. That’s awesome. I think I really underestimated how powerful what Coinbase, I don’t call it, I call it Coinbase plus Bitcoin, because it’s really the same thing.

What a [00:30:00] great solution that was to a problem. Yeah, I, when it, when they tell their big story, which is, they tell this story pretty good in their filings. There’s a lot of there I think is hand waving and I think it’s geopolitics and all this stuff. But at the center of it, there is an amazing customer story in there.

Truly like 10x level disruption and improvement against a massive problem. So I really like that. I still hold Bitcoin. I like Bitcoin. I think it’s, I think it’s great. I think it has problems. Yeah. I think the regulations are a problem. I think the technology is not as secure as everyone thinks it is.

The control of the miners. Basically a handful of people control all the mining to Bitcoin, a couple of companies control it all. That’s concerning, but still it’s a pretty spectacular product. Anyways, that’s lesson number two. I think I overestimated the strategy and the business model and I underestimated the power of a customer solution [00:31:00] that really is just amazing.

Okay, lesson number three, last one. And this gets to the other concept for today, which is role of the state. You can’t disrupt the government. You can’t disrupt the government or enterprises that are state owned or state controlled or state directed without their approval. Now this is I wrote a book about this called the one hour China consumer book, and it basically looks at consumer facing businesses in China, everything from basketball to KFC to 10 cents and all this.

And the two questions it always asks is there a competitive advantage. And what is the role of the state in this business? And for China, you absolutely, in, when Westerners start looking at Chinese companies, they understand the first question, does it have a competitive advantage versus, rivals, new entrants.

It’s the second one where a lot of people get uncomfortable. They don’t know how to assess the role of [00:32:00] the state. And I basically put a framework and a bunch of questions you can ask. And it’s pretty obvious, really. There are certain businesses where the state, and you don’t look for state owned may mean nothing, it may mean a lot.

You don’t look at state controlled, that’s not, what you look at is the interests of the state, what is the role of the state. If the state has a significant interest in a sector, they are going to impact it one way or the other. And by state, I don’t just mean the government, I mean in China, the party. the government.

In other countries, it could be princes. It could be princes and their families. It could be NGOs and institutions that are tightly bound to the government or political players. It could be Wall Street banks who are pretty much joined at the hip with Washington DC institutions. There’s a lot of blurry lines in there, depending what sector you’re looking at.

And you can put it [00:33:00] into a couple of business what is the role of the state? And it can be positive, where, look, if the state has a vested interest in making this develop quickly, it can be the mother of all catalysts. When the Chinese government says, we want electric vehicles to be a primary interest, and this came from the state council, like in 2015, that was the mother of all catalysts.

For accelerating the development of the electrical vehicle state. So if you were in that, sorry, electric vehicle industry, if you were in that sector, it was amazing for you. And the government did the same thing in solar and wind in China in 2005, 2003, in that range. When they do that, it can be incredibly powerful.

So the role of the state can be a positive, it can be neutral or it can be negative if it’s positive, that’s pretty amazing. Sometimes the state has no interest whatsoever. Restaurants. [00:34:00] There are no state owned restaurants in China. Actually, I think there’s one still. The government has no interest in restaurants.

You can do whatever you want. So when I was talking about cloud kitchens, one of the reasons I like cloud kitchens more than I like uber transportation is because there’s no interest by state affiliated parties like taxi unions. It’s pretty much a free for all. You can do whatever you want in restaurants.

And, if your tech is good, it’s going to work. So certain sectors like that, no interest. Media, you can do what you want. Retail, you can do what you want. Sometimes the role of the state will be, we want this to develop, but we want to do it slowly because there is a social cost. So somewhere like China, or a lot of the world, that’s health care and education.

You can disrupt health care and education. But it’s going to be slow [00:35:00] because there are real social costs if you get stuff wrong. So that’s like a go slow. And then there’s other sectors where it’s like. Keep your hands off this entirely.

Banks and credit in China are a keep your hands off it. You want to get the Chinese government’s attention, start doing anything with technology related to credit. They do not like that. They have said it as loud as they possibly can. Don’t start issuing lots of credit because they think it can create a systemic risk, which it can.

So certain areas, the other one that they’re interestingly hands off on is funerals. and funeral homes. They, the funeral business of China has not really evolved or developed in 20 years. It’s incredibly slow. There’s, so there’s certain sectors that are like hands off. Don’t do it. Other [00:36:00] sectors. It’s you can develop, but go slow and others.

It’s we’re going to be your best friend. We’re going to put the pedal to the floor. Solar, electric vehicles, AI, where, it’s the greatest. So you got to get a solid answer to that question. Now, when you look at Bitcoin and you look at Coinbase, do you have a solid answer to that question?

Now, I think the posture Coinbase took was right. If you are dealing with a sector with a significant role of the state. Your job is not to disrupt and your job is not even to improve. Your job is to help the state accomplish what it wants to accomplish in this sector. You are not serving the customers anymore.

You’re serving the state. So if you want to go into electric vehicles in China, or you want to go into let’s say enterprise side AI, your number one customer is the state. What do they want to accomplish here? And you help them [00:37:00] achieve it. And that’s true in a lot of sectors like insurance in China That’s definitely the way it works.

If you’re gonna be in Petrochem and in let’s say Saudi Sabic or Ramco, that’s pretty much so the government is your customer. Not so the government the state So you got to get a clean answer to that question now Coinbase was right Which they said we want to create an on ramp. We want to merge traditional finance with blockchain technology to create new products.

That’s all fine. We’re not going to be Sandbank and freed and we’re going to just disrupt and be decentralized and hide in the Bahamas or whatever Okay, yeah, I don’t agree with that. I don’t think Coinbase had it right because they viewed the state as the government No, that’s not the state. That’s part of It’s also all the Wall Street institutions who are tied at the hip with the government.

You can’t disrupt them either You have to work with them. It’s if you’re gonna go into health care [00:38:00] You have to work with the insurance companies and the big hospital chains and the government because that is all one thing Like they it’s a controlled situation. So yeah coming in and disrupting wall street.

No It should have been I would call those state directed or state controlled or enterprises. You’re going to work with them You’re not going to disrupt any of those That’s how I would have looked at that Probably would have done something with a major wall street player very early on You And then, that’s your team, major institutional player, too big to fail, government institutions, and then Coinbase, all basically being one team.

But yeah, so I, I think they that’s just an opinion, but I think they did well in not trying to disrupt the government, but trying to disrupt those institutions, I wouldn’t have done that either. Anyways, I would have viewed those two as the primary customer, not people, [00:39:00] not retail consumers.

Anyways, that’s just my experience walking around state heavily involved markets for the last 15 years. So anyways, call that a bias, call that life lessons, whatever. That’s where I fall on this stuff. I think Silicon Valley is sometimes very bad at that. Like if you look at health tech, People, every now and then a Silicon Valley firm will come out and say, we’re going to do insurance, we’re going to do healthcare software.

You know how many software people work in healthcare? There are tens of thousands of people who write code in software. None of them are in Silicon Valley. They’re all in places like Minnesota and St. Louis and Jacksonville, Florida. There are entire massive teams of people who do software in healthcare, but they don’t come out of Silicon Valley at all.

They work close to insurance companies, close to the Department of Health and Human Services. They don’t have this sort of entrepreneurial, disruptive mentality of Silicon Valley. It’s really a [00:40:00] different sort of group. Anyways, that’s been my experience. Okay. So those are my three lessons for today.

Number one, don’t fall in love with the story. Don’t get seduced by it. Don’t use it to turn off a critical data driven brain and the same for business models, which is my weakness. Number two, everything’s still, you live and you die with the customer. Coinbase plus Bitcoin was a 10 X.

solution to a truly massive and important problem. That’s awesome. And number three, you can’t disrupt the government. You can’t disrupt state owned or state controlled enterprises, all of those things unless they approve, but you got to get the green light on what you can do and what you can’t do.

You can try that. People have done that successfully, but I just think the probability of success goes down dramatically. So I don’t do it anyways. That’s where that’s the three lessons for today. Cool two concepts or a platform protocol, hybrid [00:41:00] and role of the state, which there is a whole book on, which I think it’s really a good book.

And I, as part of my standard joke is I think it was one of the best things I ever wrote and nobody bought it, which actually is a trend. Like the more I like something I’ve written. The fewer people buy it and everything that sells really well or gets a lot of adoption. It’s never the stuff I really like which is that’s really bad and I’m not really sure why it happens, but it does Anyways, that is it for the content for today as for me things are going pretty well No real news just working away, which always puts me in a good mood.

I’m always Content in life when I feel like I’m really productive and I’m learning new things and writing and all of that So it’s been a it’s been a good week in that regard I’ve been Listening to this guy who I’ve mentioned before on Twitter named Mike Benz, B E N Z, he talks about the history of the CIA and [00:42:00] information control and media control operations.

It really has blown my mind. I’m not 100 percent sure it’s true, but it could be. And it’s one of those things where like when someone explains how information and media are not controlled, but let’s say influenced, once you see it, you can’t unsee it. It’s one of those things where now I’m looking at things differently and I’m not 100 percent sure it’s true, but I think there’s probably a healthy dose of truth in what he’s saying about largely state, deep state which is a fancy word for administrative state and institutions control, or at least influence of media and info and information in lots of countries around the world, that there’s a long history of that.

It’s a type of warfare. And he talks about the mechanics of this and it’s really been blowing my mind. Still not sure what I think about it. If you’ve listened to him, take, send me a note, tell me what you think. You think this is real? You think [00:43:00] it’s half real? You think it’s all made up?

Anyways, Mike Benz, B E N Z is the last name. He’s become like famous in the last couple of months. Anyways, that’s what I’ve been doing. On the more fun side, I’ve been, we watch a lot of Korean television. It’s just cause live in Asia. So that’s what’s on Netflix, I’m watching culinary class wars.

I think Korea makes some of the best Competition shows ever like I’ve mentioned the one the influencer and they have cooking competitions and they have one called the 100 Which is like a fitness competition. They’re really good at these. They’re totally fascinating Anyways, this is one where they take famous chefs who have a certain reputation, Michelin stars, and then they put them against people with no reputation, really.

So the whole question is, and then you do taste tests and see who’s better. So the whole question is are these Michelin rated chefs who are famous and on shows, [00:44:00] are they really better chefs when you do a taste test? And it’s really clever. And I’ve been watching that this week. It’s not as good as the other one, like 100 and The Influencer.

The Influencer is amazing as a Korean competition show. But I’ve been watching that all week, so it’s fun. I gotta do something at 10pm when, your brain’s tired and I can’t think anymore, so I put on Netflix. Anyways, that is it for me. I hope this is helpful, and I will talk to you next week.

Buh bye!

——-

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.