This week’s podcast is Brazilian Stone Company (STNE), the Berkshire Hathaway-invested payment platform that has fallen in share price by +80%.

You can listen to this podcast here or at iTunes and Google Podcasts.

Here is my new book (released December 1):

Here are my 6 Levels.

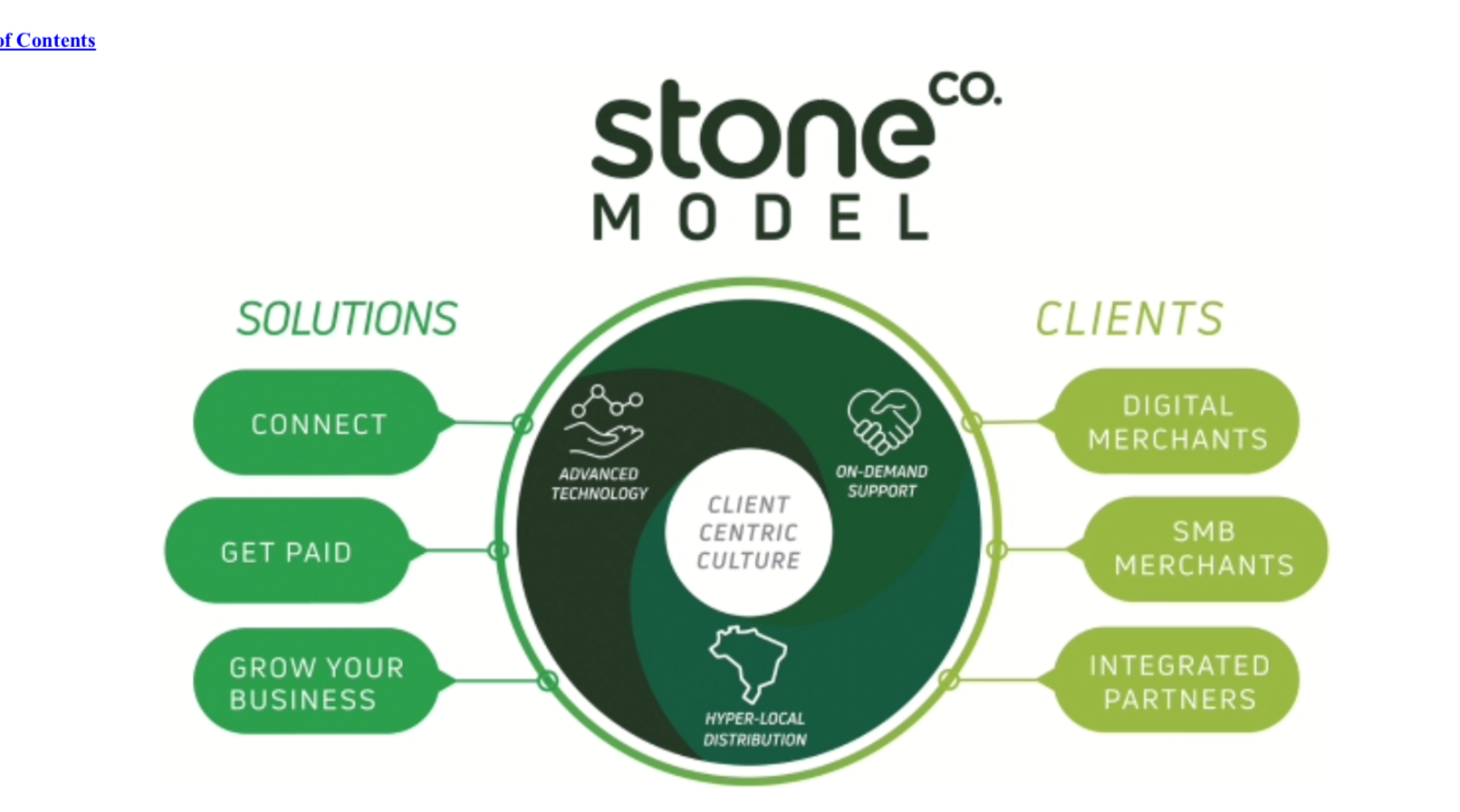

Here is how Stone describes its business model.

——-

Related articles:

- Brazilian Stone Co, Chinese Ant, and American Square Are All Building Complementary Payment Platforms (1 of 2) (Asia Tech Strategy – Daily Lesson / Update)

- What Ant Financial Tells Us About Square’s Future. (Jeff’s Asia Tech Class – Daily Update)

- Ant Financial Is 3 Platform Business Models Combined. (Jeff’s Asia Tech Class – Daily Lesson / Update)

From the Concept Library, concepts for this article are:

- Payment Platforms

- Digital-Physical Hybrid

From the Company Library, companies for this article are:

- Stone Company

Photo by Agustin Diaz Gargiulo on Unsplash

———-

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.

—–Transcription Below

:

Welcome, welcome everybody. My name is Jeff Towson and this is Tech Strategy. And the topic for today, Stone Company. Berkshire Hathaway Invested Stone Company has dropped in share price over 80% in the last six months. It’s kind of a big story in tech. People are talking about it, but really it’s about payment platforms, which is a business model I’ve talked about quite a bit and honestly, which I think is a really… particularly powerful business model when it works out. So that kind of raises the question of what’s going on and is this an opportunity? So I’m gonna go into at least the business model side of this, which is my area, strategy, technology, not necessarily the price movements, other than to point out it is really far down. And there’s a short report and there’s some non-performing loan issues and you can look all that stuff up online. It’s not really my area of expertise. Plus we’re talking about Brazil, which is out of my wheelhouse. Although I do spend more and more time looking at Brazil. I mean, if you’re talking about a platform business model in Brazil, in, you know, that’s a very regulated scenario, payments in general. So there’s a lot of Brazilian regulations. I’m not an expert in any of that. So I’m just gonna kind of talk about the one dimension I feel like I understand, which is the business model. You know, the quality of the company. and then I’ll leave the rest to you. But it’s a big, big story. I mean, it was already a big story a month ago because the price had really come down from about $90 per share in the end of the first quarter, down to $30 a share a couple months ago. Well, in the last week, it dropped down to 15. So it’s kind of a big deal. Anyways, that’s what I’m gonna go through for today. And this ties into Ant Financial and to Square. which are also payment platform companies that I’ve talked about in the past. I’ve written quite a bit about both of those. Yeah, Stone looks a lot like Square, but it’s actually very interesting. Really original model, so it’s different as well. I’ll talk about that. Now, for those of you who are subscribers, I’ve sent you two articles on this already. I’m gonna send you another one tonight or tomorrow. So I’ve really been kind of digging into this company over the last couple weeks. A lot of the people who are subscribers are professional or you know just sort of personal investors and yeah this is one you should take a look at. I mean the price drop alone makes it worth taking a look at. So I’ve sent you two articles on that another one’s on the way. Now I’ll kind of I basically I think I’ve got the right take on the business model and I don’t think it’s what the company is saying. I think their description of their business model is not helpful. I think honestly I’m I think my approach is better to tell you the truth, but that’s just my opinion. Okay, and those of you who aren’t subscribers, feel free to go over to jefftowson.com. You can sign up there, free 30-day trial, see what you think. Standard disclaimer, nothing in this podcast or in my writing or website is investment advice. The numbers and information from me and any guest may be incorrect. The views and opinions expressed by me may no longer be relevant or accurate. Overall, investing is risky. This is not investment advice. Do your own research. And with that, let’s get into the topic. Now, as always, there’s a couple key concepts for today. The two concepts I want you to sort of pay attention to are one, payment platforms. This is one of, you know, I’ve laid out five different platform business models. And I mean, that’s really just sort of categories because when you dig into each type, you realize there’s lots of variations on those. Marketplace models can be very different. Collaboration business models can be very different. And… you know, as we’ll talk about today, payment platforms can be different. Ant is different than MasterCard, than Visa, than PayPal, than Square, then Stone aspires to be. These are different versions, so that’s important. So that’s concept number one is payment platforms. The other concept for today is digital physical hybrids. I haven’t talked about this, God, it’s probably been a year or a year and a half since I talked about this. These, this is when so many companies wanna be digital entities. They wanna be all about people staring at screens because the economics are so attractive. You know, let’s say Ctrip, well, they have a lot of call centers, but I mean, it’s mostly a digital creature. Adobe, but a lot of the companies, particularly in the US, who are software digital based, they avoid the physical aspects of business. people owning warehouses, logistics, things like that. In China and Asia, actually, companies jump into that stuff much more aggressively. I like companies that are platform business models, digital platform business models, that are supported by physical, tangible assets or activities because, yes, it does hurt your economics. Your economics aren’t as pretty when you start building lots of warehouses and staffing up tens of thousands of people. However, it also gives you this tremendous, often gives you a tremendous barrier to entry. Makes it much harder to replicate and it makes it much harder to break in quickly. If you’re a purely digital creature, like a lot of media companies are this way, man, you can get a competitor coming out of nowhere and in six months they start taking your market share. Because by virtue of being digital, it’s really easy to launch. But if you’re a major e-commerce company like Shopee or Alibaba or Amazon, it’s gonna take you five, gotta make five to seven years to build the physical assets to take on that company. So you’re gonna see your competitors coming. So I like, I mean, I like the barrier to entry. I’ll give up some attractive economics in order to get a more tangible barrier. Anyways, I call those digital physical hybrids. Usually I’m talking about platform business models. supported by physical assets, but they can also just be software companies. Anyways, that’s what Stone is basically doing. And that’s the so one of the so what’s for today, the difference between a company like Stone and Ant and particularly Square, which is probably the most similar to is that Stone is a developing economy platform play that is really deep into physical operations from day one in a way that Square absolutely is not. Stone’s a digital physical hybrid, Square is not. Ant isn’t either, because Alibaba doesn’t like to have any physical stuff, really. Okay, those are the two ideas for today. Platform payments, I’m sorry, payment platforms, digital physical hybrids, in the show notes. Okay, so, I mean, what’s going on this week? It’s kind of all over the press. Basically, I’m not gonna go into the earnings results that they released about a week ago. Now hedge fund people know that stuff backwards and forwards. I don’t. I mean, I know business models. Well, I think I do. OK, Stone Company. People call it Stone. They call it Stone Co. I’m just going to say Stone. Founded 2012 by two guys, Andre Street, Eduardo Pontes. I’m probably saying those name wrong. Sorry about that. Basically a payment platform. I mean, that’s a business model. I’ll talk about those. But a business model. I’m sorry, payment platform for Brazil, which is a very bold idea because, one, Brazil is a very large country. It’s a developing economy. It’s statist by any definition. It’s highly bureaucratic. Government plays a major role. You go hang out with any Brazilian business people at dinner. After one drink, everyone starts complaining about regulations in government. It’s like all the time. I mean, you want to meet a lot of frustrated business people and you want to meet a bunch of badly served consumers, hang out in Brazil. Brazilian consumers might be the most poorly treated consumers on the planet. Terrible behavior by businesses. I mean, it’s really bad. So Stone basically gets launched. I mean, you could say that it looks a lot like Square in the early days. Jack Dorsey’s company. But basically the idea is like, we’re gonna create a payment platform and we’re gonna focus on small merchants, SMEs, SMBs, of which there’s a lot in Brazil. I mean, this is a 5,000 city country, tons and tons of little businesses everywhere. And traditionally, the numbers from Stone, they say 8.8 million of these companies around Brazil. plus another let’s say 5 million micro merchants, which would be a level smaller. And these groups are chronically ignored by the mostly a lot of state owned banks, some private banks, some foreign banks. But you know, these you go in there as a regular consumer, which I have done, man, you get treated badly. You know, so these small companies have been vastly underserved. by the banking system and the financial institutions, and overcharged as well. So Stone comes in and says, we’re gonna build a payment platform that serves small merchants, and we’re gonna enable them to take digital payments easily, whether it’s in store, which would be putting sort of point of sale devices, card readers and things like that. or online and we’ll make it so you can take payment easily from any service. It can be a credit card, it can be a debit card, it can be a QR code. We can even have you send links if you’re doing stuff on TikTok or whatever and people can just pay by clicking the link. So to make it convenient, seamless, as for small businesses to get paid. And that’s pretty much how Square started. It was the same idea. Okay, but it’s a lot. more different in Brazil. One, internet penetration is not nearly as high. The country has not moved away from cash at the same rate as other countries. I mean, you go to most SMEs, they’re operating in cash. They get paid in cash at their little store. They stick it in a drawer. Every now and then they go down to the bank and they get treated badly. You know, you have the sort of square idea, but on top of that, you have the fact that this is a developing economy and you’re serving a very non digital demographic. So what’s what stone is really doing is yes, they’re doing the payment platform. Yes, they’re offering a payment capability, these small companies, but they’re not just connecting them. They’re digitizing them as well. They’re trying to get them to start operating in a digital way and connect them. And that’s a bigger mandate and it’s hard and you know things happen slowly in developing economies. So it’s a bold idea. Bold could also mean really super difficult. And they started with payment processing, omni-channel payment processing. I’ll go through some of their business from there, but they basically do payment processing transactions and then they’ve moved into enterprise software and services which is like… you know, we’ll offer you other things you can do. We can, you can pay your taxes, you can have an ERP system, you can do loyalty programs from payment. They started to offer more digital services to these small companies. So it’s almost like a quasi ERP enterprise service system. Okay, so what’s been going on with them this year? They go public in 2018. So founded 2012, public in 2018. The growth numbers are very impressive. You know, they go from 100,000 active users, which would be merchants. That’s the key number. You know, then it’s 200,000, then 300,000, now it’s 450,000 plus right now. Big growth in user numbers, big growth in payment volumes going through their system. So everyone gets excited about that because that’s how you build a platform business model. That’s the… four intangible assets of a platform business model. If we were building a retail chain, we’d be counting stores, we’d be counting traffic. When you’re looking at a platform like a payment platform, you’re looking at user number, engagement, data, and then cash flow, which is usually cash gross margin is the one you wanna look at. Okay, they’ve got this big growth, they’re looking good. They go public 2018. People are already paying attention to them. And then it comes out that Berkshire Hathaway has bought 14 million shares after the IPO, which gives them around 10% of the company, 8, 9, 10% in that range. The market cap they bought in at was about $9 billion US dollars. Okay, so that gets them on the, you know, all over the press. Now, it’s not clear to me at least who did that purchase, you know. Berkshire Hathaway’s Warren Buffett, but it’s also Ted and Todd. And usually these smaller investments, when you’re talking about a couple hundred million dollars, which is what they invested, you know, that’s usually Ted and Todd. It’s not Warren. But however, Warren has long been a big investor in American Express, MasterCard, and Visa. These are all payment platforms. So it wouldn’t surprise me if this was him as well. The other thing that popped in is the founders of 3G, the, you know, Jorge Paulo, Marcel Telles, I’m pronouncing these names wrong, Sucupira, I mean, the famous, you know, the richest people in Brazil, basically, they’re big investors too. And at least Jorge is, you know, he’s friends with Warren Buffett and they do investments together. So who knows, I don’t know where it came from, but you know, big famous names are involved. And then, and financial in China also invest. Okay, that’s 2018. Share price hovers around 30 for about a year. Mid to late 2020, the share price really starts going up. Ramps up by early 2021, the share price is $90. At that point, Berkshire Hathaway sold some of their stake, but not all of it, like 20 or 30% in that range. Don’t hold me to that number, but it’s about that. So that’s in the 90s. Then the numbers start falling. Second quarter of 2021, it starts going 90, 80, 70, 60. By August, October, we’re down to $30 per share. People are making videos and articles. Is Stona by? During this decaying period, second quarter, third quarter, ARK Invest, she, you know, Kathy Wood is buying. Basically, you can see the chart every time the stock drops, she’s buying more, or not her, but her company, her funds, they’re buying more. So a lot of activity around it. Earnings report comes out a week ago, the stock was at 30, after the earnings report, it drops another 30 to 40%, now it’s at 15 to $16. Down from 90, 92 started this year. Now I’m not gonna go into the reasons, you can look those up, but it has something to do with… the non-performing loans. They offer some credit solutions to their merchants. I’ll talk about that. Those are collateralized against credit card receivables. It turns out some, probably what part of what’s going on is some of these buyers who are borrowing money, they were taking their same credit card receivables and filing them in multiple locations. And I know there’s something going on. As far as I can tell, the non-performing loans were significantly higher than what everyone thought. And then they had to dial that back and they had to cut off some of their credit and if you cut away their credit, that takes a significant number of their revenue away. And there’s a bit going on there, I’m gonna leave that to you to figure out because that’s really not an area I have expertise in. But that’s kind of where we are. So that brings us to the question which is in my strike zone. Is this an attractive business model? Are we looking at a potentially very attractive company that happens to be in a situation where maybe it’s underpriced, maybe it’s appropriately priced, maybe it’s overpriced still, who knows? I’ll leave that to you, but the question of how good is this company or could it be? Okay, payment platforms. I like payment platforms. Specifically, I like global. payment platforms. Okay it’s a platform business model, two user groups, merchants, consumers usually. You immediately get at least one network effect which is you know you walk into a store, you pay with your credit card, the merchant has a point-of-sale machine, they take it, they get paid. You know the more people that accept American Express the better it is for consumers and vice versa for merchants. Fine it’s a… It’s a nice network effect that doesn’t seem to have a flatline moment. If I’ve got an American Express card in my wallet, it works in Bangkok. It works in Shanghai. It works in Tokyo. It works in London. You know, the more merchants around the world that take that credit card, the better it is for me, it doesn’t flatline. It keeps going up and up and up. Um, and vice versa. And so. You know, big surprise, what have we seen for the past, you know, 30 to 40 years, is we have seen the payment platforms collapse to a winner-take-most scenario. There’s MasterCard, there’s Visa, and then much smaller, there’s American Express. That’s the Western credit card market. I mean, there’s some others, but that’s a huge portion of the game, and they’ve been dominant for decades. That’s a really powerful model. And we can see other versions of payment platforms, PayPal and Stripe. If you’re gonna take payments online and you’re sitting in the US, you have to sign up for pay, if you’re a merchant, you have to sign up for PayPal and Stripe. One or the other or both, and there aren’t that many other options. There are a couple, but that’s pretty much it. Cause everyone’s got a PayPal account who’s a consumer. or everyone’s got it as a merchant, or they take the credit card or whatever. But, you know, so what do credit cards typically charge? One, two, 3%, what does Stripe and PayPal charge? Well, they sit on top of the credit card network. I take PayPal on my little website and they charge me 7%. That’s obscene. Like, it’s absolutely obscene, that level of thing, but there’s just not that many options. You have websites and whatever, you have subscribers all over the world. And that’s just the way it is? Yeah, it’s pretty bad. Well, it’s great for them. It’s great if you’re an investor. Okay, so these business models can be very powerful. Not always, but sometimes. The big difference that jumps out at you is let’s say we look at China, then we’re talking about WeChat Pay and Alipay again. There are other companies that tried to start payment platforms in China, but those two… you’re talking 80, 90% of the market now. Again, collapse to win or take most. And there’s some other things going on. The network effect is the big thing, but there’s also some switching costs that you can build in on the merchant side. There’s some switching costs you can build in on the consumer side. You can give them loyalty points, things like that. You do get economies of scale in your fixed costs. There are significant fixed costs in fraud that you have to build these massive operational abilities to detect fraud. So you have sort of fixed costs. So you get economies of scale in that regard. You get a big network effect. You can get, in China, you can get a couple other network effects because mobile payment, you can send one consumer to another. So you get a direct network effect there. You can send merchant to merchant. So you get one there. So in China, you actually get three network effects at least, and then you get some switching costs. It’s just a great business model and… You know, it shows up in the financials. So there’s a bunch of those. The biggest difference, of course, when you start looking at, say, China to the US, is most of the payment platforms in the United States are built on the interbank network. You look at any cost structure for PayPal, Stripe, Square, what you’re gonna see is a significant cost of revenue line about basically assessment and interchange fees, because… when you sign up for PayPal, they rely on Visa and MasterCard’s basically payment scheme for settlement and they have to pay them to use their network. So they’re kind of, they’re not really a network entirely, they’re kind of a network that sits on top of a network. It’s like you are, it’s a little bit like the App Store. You could say Facebook is a network. but it depends on being on a smartphone, which means they depend on being on Android or iOS. And if those company charge them 20%, what are they gonna do? Because if they get kicked off the operating system, so the network is kind of like, look, the operating system that we have on our phones that are in our pockets, that’s one level of the network that’s controlled by Android and Apple. And then the other network, let’s say Facebook or Twitter or whatever, that sits on top of that network. And they’re kind of dependent on them and maybe they charge them and maybe they don’t. Well, in payment schemes in the West, Visa and MasterCard and the Internet Bank network, they do charge them and they are pretty powerful. We don’t see that in China. You know, WeChat Pay, Alipay, they don’t have that problem. When we look at Stone in Brazil, look at the cost of revenue, you will see those interchange and assessment fees. And that will be one of the risks in their risk section that those fees get increased or the terms get changed. So it’s a little bit different. But anyways, the net net is payment platforms can be a particularly powerful business model. I’ve given you my six levels of digital competition. I’ll put the graphic in the show notes. I’ve talked about these before, competitive advantage, barriers to entry, digital marathons, digital operating basics. The top level, the thousands tower they call it, the top of that pyramid, the tower is competitive fortress. And I’ve listed four types of business models that I think are the most powerful business models I see when we’re talking digital. local dominance, I won’t go through them, I’ll put a list of them in the show notes. But the key thing is number two on that list is what I call ecosystem orchestrator. Where you are the center of a significant ecosystem where you’re just dominating in that. And I think payment platforms like MasterCard and Visa are dominant ecosystem orchestrators where if anyone pays anyone, you’re probably paying this company because of the power of that network. So I put… payment platforms as a type of ecosystem orchestrator. I also put the major e-commerce players like Shopee and Taobao as an example of ecosystem operators. And a couple of e-commerce companies for services like Airbnb, I would put in that level too. But it’s a pretty small list of companies that I put sort of at the top level of this is about as powerful a business model as you’re fine. So So the net-net of that, what am I saying? Big surprise, why are these big investors involved? Why did Warren Buffett get involved in Stone? Because this is clearly has the potential to be a dominant business model on the level of Square, Alipay, MasterCard, and Visa. I mean, these are very rare, powerful companies. It doesn’t mean it will be that, but it has the potential to be that. So it’s not at all surprising that Buffett jumped in on this one. And that’s actually how I heard about this company a year ago, I always checked what Buffett’s buying and when I saw him buy a Brazilian company in tech, I was like, that’s strange. That’s how I got involved in that. So it’s not surprising. His companies tend to be very high up there in their competitive strength and defensibility. Okay, so that’s kind of point number one, which is payment platforms can be very powerful. Stone has the potential to become this. MasterCard and Visa are. Square is on its way. Stripe and PayPal are looking pretty good. Now there’s a big caveat to all of that, which is payment platforms and FinTech, one, they’re more regulated than e-commerce and other spaces. The other is there’s a lot of technological innovation happening in FinTech. And there’s a chance that this is all going to get disrupted. You know, and maybe Visa and MasterCard in 10 years will not be like they’ve been in the last 40 years. We’re not seeing the same level of technological advancement and maybe disruption in e-commerce, in other areas, like we’re seeing it in FinTech. So there’s a chance we won’t be even talking about payment platforms in five years. It’s possible. But thus far, It has been a very powerful model. That’s my first point, and that’s concept number one for today, payment platforms. Very, very important, and they don’t come along very often. Okay, so that’s how Stone gets launched, and very much like Square, they went after an underserved group of merchants. So if we’re talking about a payment platform, that’s one of your user groups. SMEs, that’s where they’re going. And fortunately, in Brazil, they have much bigger problems to solve than say a typical merchant in the US. That’s good. That means if you have a digital solution, it’s going to you’re going to get a lot more bang for your buck in terms of its perceived value by the merchant. So they go to them and they basically offer them, this is their words, not mine, three things. They say we’re going to help you connect, get paid and grow. You can go to their webpage and see this. Connect is basically like, look, we’re gonna let you start taking payments online, in your store, on e-commerce sites. If you wanna post your stuff on Mercado Libre, all of that, you’ll have, we’ll give you an omni-channel capability that lets you get paid. And how else would you do this? You didn’t have any ability, we’re gonna give you that. So that’s the Connect part. Get paid. Now. If you provide sort of payment processing, clearance, settlement, and I mean there’s a lot of regulations around this which I’m not too familiar with in Brazil, but you basically have to become a merchant acquirer. What Stone has become is the first non-bank financial institution of Brazil to get a merchant acquirer license, which means they can go sign up merchants and effectively be in charge of taking payments for them and settling. which is usually something only banks could do. So what Stone does is it goes around and signs up merchants and then becomes the merchant acquirer. And there’s other companies that do this. But okay, so they sign these companies up, they handle their payment transactions. Now from there, they basically did what Square has done. They went from payment to credit. Okay, you’re taking a, you’re a small merchant in Fortaleza, Brazil. You’re taking a payment on a credit card, the customer makes the purchase, but now you have to wait at least 30 days probably to get paid, because people pay their credit cards later and then they eventually pay the merchant. And that kind of delay is a big problem for small businesses because they’re often dependent on that to buy their inventory for the next week. The cash cycle is really important for small businesses. Okay, so what Stone comes in and does, it says, you know, we will basically provide you working capital as a solution, as a service. We will give you the money much faster and then we will, you know, secure our loan to you against the credit card receivables because they’re being processed through the company. And that’s pretty much what Square has done. The difference between that and say what Ant Financial has done is for They are basically providing this credit as a service that they charge a fee for. So they might raise the money, they might use their own money, they might borrow money, they might take those receivables and then securitize them and sell them to investment groups. But they’re sort of providing it as a service. What Ant did, which is different, is they said, we’re going to bring in banks, hundreds of them, as an entirely new user group on our platform. We’ll have merchants, we’ll have consumers as the two main user groups on our payment platform. We will add hundreds of banks as a third user group, and they will be the ones that provide the credit, and we won’t. We will just take a transaction fee, a technology fee, they called it, as it passes through us. So they went full platform play, and said, we’re not gonna hold any of this credit. We’ll just connect you with the bank, and they’ll deal with it. And that is exactly the area the Chinese government cracked down on. They didn’t want them issuing lots of credit and then just passing it off and taking a fee. So they sort of mandated, if you’re going to extend credit, you have to provide 30% of it. You have to act like a bank. No pure securitization, which is a pretty good idea. OK, that was Ant’s approach. They did a platform play. Square and Stone have largely provided this as a service themselves, and then they get the money from somewhere. Okay, so they go from payment to working capital, and that is a very, very good pitch to merchants. That’s a good value proposition to get someone to sign up. From there, they expand to other types of financial services for merchants. Credit, loans, they basically, and this is why I think Cathy Wood is interested. I think they’re building a full end-to-end financial services suite for small merchants because they’re starting to offer credit cards to them. You can get a Stone card. Basically anything this merchant would have in the past gone to a bank for, I think Stone is pretty much offering. They’re doing a decent number of acquisitions. They bought Lynx and they bought some others. They’re doing strategic investments in companies. You know, they’re kind of building this full suite, like look, we’ll bring you in the door with payment and then we will offer you a full suite of financial services products that is everything you’d ever need as a small business. Every dollar that goes into your company and every dollar that comes out. If you need to pay for stuff, bill pay, you can do that through our wallet. You need to pay your taxes, we can handle that. You know, full suite, which is great. That’s a very good idea. So they move from processing payments to let’s call it a growing suite of financial services Where the technology is designed from day one for small merchants and how they operate From there they put a foot into enterprise services Which is look we’re already offering you all these financial services. We’re like your your finance office Why don’t we start offering you other capabilities to run your business? Why don’t we we give you? customer loyalty programs. Why don’t we offer you an ERP-like system? Why don’t we create a POS app store where if you have one of our POS devices in your little store, not only do you get our functions, but we have developers who are creating lots of apps that run on that. So they’re starting to look like an enterprise services company, again, custom designed for small businesses in Brazil. So they’re kind of moving down the pathway. And this is kind of the difference between them and let’s say Square. Square is doing pretty much the same thing, but much less aggressively. They do a little bit of credit, they’ve got a deal they’re working on, where they offer a little bit and they’ve got an investor group and whatever. And they do a couple enterprise services, but they are not nearly as aggressive as Stone is. I mean, they’re really moving fast and now they’re starting to build out their suite of enterprise services that are sort of custom designed for various industries. So they’re starting to offer services for like salons. So if you have a hair salon, small business, couple people, they give them appointment apps and pay online. And so they’re starting to build sort of a custom suite for that. They might have one for an auto dealership, let’s say an auto repair store. food and beverage, lots of little food and beverage stores all over Brazil. So they’re building these sort of enterprise specific verticals for small businesses and you know Aside from you know what the stock has been doing if you look at their operational activity over the last year They’ve been rocking and rolling their user numbers are going up there. They’re actually accelerating The payment volumes going through their platform are increasing. The number of capabilities they are building out for their user demographic is growing. One they’re developing it internally and two they’re doing M&A and partnerships and other things. They’re moving fast. So you know that’s the question of could this be an unbelievably good business model and the answer is yes it could. This could be. a phenomenal business. It may not. You know, there’s some issues going on. And then the other issue, which I haven’t talked about at all, is look, they’re not the only one doing this. The banks are all moving into digital in some form in Brazil. They’ve all got subsidiaries or partners or joint ventures where they’re doing payment processing and other things. There’s other digital players. There’s a lot of merchant acquirers. There’s software vendors. I mean, Yeah, so let’s say Stone is providing POS machines, which is hardware plus some software. But you know, there’s a lot of software and POS vendors already on the ground. So there’s a lot of competition here. There’s a lot of technological change. And then there’s always the big question mark of the regulatory decisions of Brazil. Are the big banks really gonna allow themselves to be disrupted or are they gonna reach out to their friends in politics? Big banks. are usually pretty embedded politically, or at least pretty impressive. Are they gonna shut this down? That does happen in some governments, in some countries. When a small digital disruptor starts really clobbering major companies, those major companies turn to the government and on a regular basis, the government shuts those disruptors down. It does happen. So we’ll kind of see what Brazil is made of. Does it allow disruption? or not. So there’s a lot more going on there, but yes, the net net of that is this could be an incredibly impressive business model. Okay, last concept for today. Digital physical hybrid. This is where stone really becomes different than Square or Ant or MasterCard or Visa. They have what they call the stone business model. They have a graphic for it. I’ll put it in the show notes. And they describe the stone business model as having sort of three pillars. Number one, and this is, I’m quoting them. Number one, advanced end-to-end cloud-based technology platform. They help their clients connect, get paid and grow, talked about that, overcome long-standing inefficiencies within the Brazilian payments market. And our platform enables us to develop, host and deploy our solutions very quickly. Okay. That’s kind of wordy. Pillar number two of the stone business model, quote, differentiated hyperlocal and integrated distribution. What does that mean? They have something they call stone hubs. There are about 350 of them all over Brazil. These are local operations. This is like their version of a bank outlet, a bank branch. When they go city to city to city, they open up stone hubs, staffed up, and in those stone hubs, they have people. They have sales agents who go and meet with merchants directly and do direct sales. They have onboarding help, so when they help, they go out and work with them and help you install your POS machine. They have logistics coordination. They deliver the machine to you. They help you get involved. They have operational support if you have issues, and they have customer service. And that’s kind of number three on their list is white, this is a quote, white glove on demand customer service. Quote, we created our on demand customer service team to support our clients quickly, conveniently, and with high quality service. Designed to strengthen our relationships and improve the lifetime value of us. And they focus on a human connection and proximity. That’s their word to the client. Now that’s kind of. Their description, I think that’s very wordy and not awesome. I would just use my term. I think this is a digital-physical hybrid. They are building very specialized solutions for their demographic, which is small and medium businesses in Brazil. That’s a very unique demographic. They have very unique needs, and they are building very differentiated technology that serves them. but they are also building very specialized operations at the local level to also support them. They are technology plus local operations. They are tech and software plus lots and lots of people. And they talk about their stone hubs and they talk about the stone agents that work in those hubs and they talk about their sales teams and their customer service reps. and their net promoter scores and how many times they have to take a phone call to solve a problem and they have what they call their green angels who deliver stuff and do logistics. I mean, they are building as aggressively in terms of local operations as they are in software and hardware. And that’s a huge difference between them and Square and Ant. And I think that’s awesome. I think that’s, you know, getting back to the point I started with. it’s gonna make their economics not as pretty because they’re not just gonna have software and hardware with fixed costs that scale up and you get an increase in gross margin and all the nice stuff we like to see in software. But they are gonna have an army of people, city by city in Brazil that work with these small merchants and have proximity and a human connection with them. Now, think about what a powerful contrast that is. to a pure digital company that just has a bunch of people in a business park, and any time you have a problem, you gotta send a ticker into customer service or look at their FAQs, which never help. Think of the contrast there, and also think about the contrast to traditional banks, which, I started this description by saying, look, typical banks in Brazil, no offense to all the Brazilians, treat small merchants terribly. The customer service is awful. Even as a, I don’t know if it’s just small person, as I go into those banks, and I can’t believe how badly I’m treated. They’re notorious for bad customer service, and yet here we have Stone, and they are leading with quote unquote, white glove on demand customer service as one of their three pillars. That’s a shot in the chest to these traditional competitors. Specialized tech, specialized local operations. high quality customer service. That’s a nice competitive contrast. So, now let’s say this is successful. One, I think this has a lot, they also talk about this as like, look, this is their go-to-market strategy. This is how they’ve been growing. What determines their rate of growth? How many stone hubs they have open. Be they open one of these in town, the people go out, they start recruiting new merchants, they work with them, they get the devices installed. I mean, this is… This is a brute force go to market strategy, but it’s also an interesting business model. I think that’s really interesting. I think in theory, I’m very, let’s say impressed. Anyway, so those are kind of the two biggest differences, I think, and I would argue that Stone, the Ant Financial model everyone likes to talk about because it’s Alibaba and it’s super smart, but it’s very China specific. It’s not going to work that well in Argentina. It’s not going to work that well in Indonesia. Square is very suited to a developed economy with lots of technology everywhere. And everyone’s got the internet and everyone’s got credit cards. And you know, you got MasterCard. What Stone is building looks to me as very well suited for like half the planet. Indonesia, India. Pakistan, Sri Lanka, if you’re gonna, you know, isn’t that a better model? So I’m sort of compelled that this is a really good developing economy version of a digital payment platform. That’s kind of where I’m thinking about this. Okay, I think that’s pretty much what I wanted to go through. I think you get a sense of what I think of the business model, which is like, yeah, I think this could be top of the pyramid. I think this could be a competitive fortress. up there with a Square, Stripe, Vista, or MasterCard. It won’t be global. I mean, MasterCard and Vista get a lot of their power by their global nature, and that’s important in payment platforms. Okay, it won’t be that. But that said, let me put one last caveat. I’m not recommending anyone buy. I don’t make investment recommendations. I’m recommending you take a look at it, because it is kind of an interesting scenario. There’s a lot here I don’t understand. I don’t understand the regulatory issues of Brazil and what’s gonna happen with regards to Fintech and payments. I don’t understand exactly why the stock has been dropping. What is the significance of the last six months? And I do doubt myself a bit on predicting what’s gonna happen with business models in payment and finance with crypto and all this other stuff. I’m thinking about it. I’m just not that confident in my assessment because I think it’s changing. I mean, everything’s changing pretty quick. That’s kind of where I fall on that. Okay, so I think that’s it. The two concepts for today, payment platforms and digital physical hybrids. As for me, it’s been a nice, quiet week, just sort of reading and working away. I’m moved into my new place, which is quite a lot higher. So I think I have finally defeated the pigeons. Like I think I’m above where they normally fly. because I don’t see them at all. They don’t land on the ledge. It’s, that may turn out to be one of the biggest benefits of this new place is it’s kind of pigeon free. Yeah, not much going on, just working away. Good TV show I watched this week was Hellbound, which is on Netflix. It’s kind of one of their new shows. It’s a very strange, but really it seems stupid at first. It’s basically about like these creatures that appear out of nowhere. And killed someone on the street of South Korea, and people start to think that they’re angels enacting God’s will, and a huge religion is built based on this, but then it’s not clear what this is really about. It started out really weird. I thought it was stupid in the first half hour, but it gets more and more interesting as you go through it. There’s six episodes, and by the sixth episode, you don’t know what’s going on. It keeps twisting. It really turned out to be It’s one of those things that kind of has me thinking. It’s really cool. Anyways, that’s worth checking out. I think that’s a pretty decent show and that’s just coming out. Okay, that’s pretty much it. I hope everyone’s doing well, wherever you are, that maybe things are opening up and we’re coming out of this whole scenario. I guess in Europe that is not really the case. I was planning on going out there in a couple weeks, but it looks like Europe is locking down, so that might put the kibosh on that idea. Oh well. Anyways, that’s it for me. I hope you’re doing well. Take care and I will talk to you next week. Bye bye.