In my online Asia Tech Class, I talk a lot about digital superpowers, which are digital tools that upend established business. And one of these superpowers a dramatically improved user experience, such that the traditional offering is now unacceptable to users. And this sort of dramatically improved user experience is what is happening in luxury products and services in China / Asia. Chinese consumers and social media are disrupting, improving and increasingly personalizing luxury. That is my topic for this weekly article.

Ok back to digital China meets luxury.

What we are seeing in China (and Asia) is the rapid emergence of online-merge-offline (OMO) luxury that is:

- Dramatically richer in its brand storytelling.

- Increasingly personalized in user communications and experiences.

- Increasingly a combination of products and services

And I argue that his follows from 3 factors that are (thus far) coming from digital China:

Factor 1: Chinese luxury spending is really big and getting bigger. It is a “must win” market for luxury brands.

Over the past five years, Chinese consumers averaged 40-50% of all global luxury spending. It is about $100B per year right now. But it is pretty volatile. And Chinese are expected to account for 65-75% of luxury spending growth in the next five years. L2 Gartner projects it Chinese luxury spending to reach $175B by 2025.

The growth is actually coming from lots of areas. Certainly young consumers and women are a big percentage. And lower-tier cities are a big driver of this, like everything else consumer-related right now. But it’s mostly a story of the increasing wealth of Chinese families. Luxury is benefiting from a massive rising middle class plus a large population of affluent consumers.

So for luxury brands everywhere, Chinese consumers are a must win demographic.

Factor 2: Chinese consumer behavior in luxury is changing fast.

Chinese luxury spending is pretty volatile year-to-year. For example, in 2015, Chinese luxury spending grew at only 2%. But in 2018, while China’s GDP growth was its lowest in 30 years, luxury spending grew by +20%. It’s just a volatile sector.

There are also fads and trends. And lots of differences within sub-sectors and booms and busts (especially in art sales). Chinese luxury spending can be impacted by lots of things – such as:

- Real estate and stock markets, which impact overall wealth (real and perceived).

- Consumer confidence. Spending on luxuries usually gets cut first when confidence falls.

- Changing consumer preferences and buying behaviors.

- Changes in consumer-facing technology, especially social media and smartphones.

- Changing tax rules and regulations, especially related to luxury imports. Corporate gifting rules also have a particularly big impact.

- Changing exchange rates.

But the biggest driver of changes is what I call the “China Consumer Network” (CCN).

Factor 3: The China Consumer Network, not enterprises or government, is the big engine of digital China.

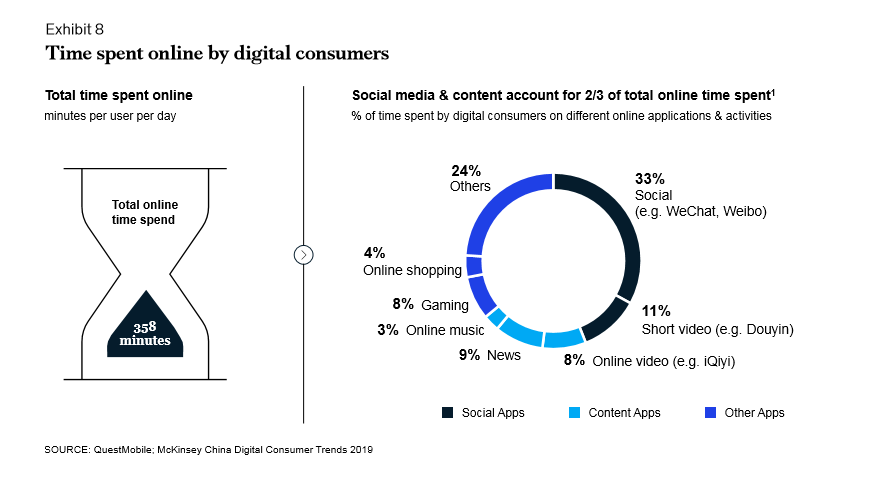

China is the first country to have +1B digitally-connected consumers that share a common language, a common culture, a common regulatory environment and lots of supporting infrastructure. Digitally connected and hyper-active Chinese consumers are increasingly acting like a network with frequent interactions between individuals. Consumers interacting with other consumers can impact a business far more (and far faster) than a company can. And as the connections of a network increase at the square of the number of nodes (sort of), the China consumer network is particularly large and powerful. China may have 4x as many consumers as the US, but its consumer network has 17x more connections (theoretically).

It’s pretty awesome.

- The Chinese digital consumer, via their smartphone, is always on. And is surprisingly enthusiastic. We have never seen such a massive population of digitally connected and active consumers.

- This network is showing inreasing sharing, transactions, production and consumption. The speed and volume of interactions has been exploding.

- Activities and businesses that can tap into this network take off at incredible speed. Think TikTok and WeChat.

- Digital consumers and network activity result in data, data, data – which enables new services, powers machine learning and AI technologies, and results in precise targeting and customization.

- Right now, WeChat and social media are the most powerful type of interaction happening on the network.

***

I think these three factors are forcing luxury brands to change very rapidly.

Result 1: Luxury brands are going all-in on WeChat and social media

Luxury brands have long disliked e-commerce. It really does crush your luxury service when you have to shift from selling in nice stores with a carefully crafted ambiance to being just a thumbnail on a smartphone screen. Luxury was one of the last sectors to move into e-commerce.

But they are now going all-in on e-commerce and specifically WeChat and Chinese social media. Because Chinese consumers are the big demographic and they operate a digital network. The brands have to go digital now. And that has meant a big shift into digital marketing and WeChat. Note the below chart from Bain & Co about how the top luxury brands in China have been shifting their advertising online.

And in practice, all this digital marketing really means WeChat, Tiktok, Weibo and content creation (including KOLs). For example, the top 40 luxury brands allocated 40-70% of digital marketing budgets to WeChat.

Result 2: Brand storytelling is getting much richer

In China, brands like Gucci and Prada are creating short videos and other engaging content. Make-up and hair brands like L’Oreal are working with Chinese KOLs on education campaigns about their latest products. And companies like Burberry are offering challenges for users generated content about their products. They are all using content (which can be easily shared) to engage the China consumer network.

And this is a big change from traditional brand story telling through mass market print ads and nice stores. It is far richer. It has more depth. Suddenly you can tell more complicated stories about your products. You can create niche products (like skin cream for late nights when you have to get up early for work). This increased ability to tell complicated stores through content on the CNN is particularly helpful for niche and new brands. Professional and user generated content sent out through the China Consumer Network (CCN) enables far richer, engaging and complicated storytelling.

Result 3: Consumer communications and experiences are increasingly personalized

Digital and programmatic marketing is a departure from the mass marketing campaigns of the past. Suddenly you can market to and have two-way communicate with specific demographics. And around specific use cases. And, increasingly, you can market and communicate on a one-to-one basis with each consumer differently. Personalized marketing and engagement at scale is the holy grail.

Additionally, you can also personalize a consumer’s experience online and in stores. The Prada store one consumer sees online can look very different than what others see. Not just in the products shown. But the colors, the content and the style can all be personalized. And increasingly this personalization of experiences will happen in physical stores. Digital tools like facial recognition, digital screens, smart mirrors, customized inventory, and customized products are being implemented.

Result 4: Luxury will increasingly combine products and services

If you are selling someone make-up in a story or via their smartphone, you can now send someone to their home to apply it. Or to do their hair. And to fit their outfit. You can also increasingly integrate fashion consultants via video conference to help them choose outfits as they shop. And we may get to their point where designers and manufacturers can participate in the sales process and offer to design new clothes specifically for them.

We are seeing an increasing integration of luxury products and services. These can be supporting services. Or they can be luxury service like tourism, where Chinese consumers are increasingly expected personalized vacations and experiences.

***

Final Point: The future of luxury is online-merge-offline (OMO). And the China consumer network is driving this.

One of the reasons digital is having such a big impact on luxury is because the consumer experience has real power both online and offline. Online and digital marketing is great for telling richer and more complicated brand stories. And for personalization. But consumers still prefer to purchase luxury goods offline in stores. Note the below McKinsey & Co chart on consumer preferences for luxury purchasing.

So the future of luxury is going to be online-merge-offline with lots of interesting approaches by different companies. It will be fun to watch this play out.

***

Ok. That’s it for today. Have a great day and thanks for reading, – jeff

———-

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.