In Part 1, I went through the basics of BYD, a very successful battery manufacturer that became China’s leading player in electric vehicles. You can see this in their financials. It’s all about auto sales in China. Which has really taken off in the past 3 years.

However, they are definitely going for global leadership. Which raises an interesting strategy question:

How do you win globally as electric and eventually autonomous vehicle company?

And can BYD win it all?

Here is BYD’s Plan for Auto

In its recent annual report, BYD laid out its priorities for its auto business.

My assessment of their priorities for auto going forward is:

- Make lots of car models rapidly. Keep improving them models. Better and better products is priority #1.

- This will also improve their brand.

- Do lots of pioneering innovation in technology and batteries. These are fundamentally new products. BYD frequently cites their blade battery and hybrid technology.

- Increase their production capacity, including internationally.

- Improve their “market sense”.

- Maintain their leadership position.

Here’s what I think that all that means in terms of strategy.

They are moving as fast as possible. They are getting big as faster as possible. And they are rapidly iterating in their products and the customer experience. I put all that under the operating basics.

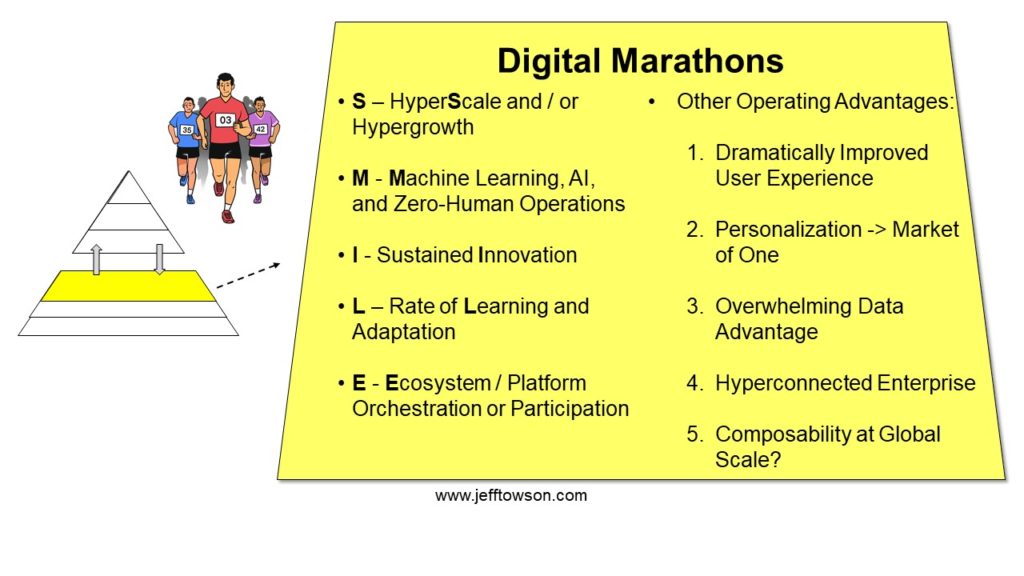

However, they are also clearly running a marathon in Sustained Innovation. That is their primary competitive strategy. They are trying to slowly pull ahead technologically. I’d be measuring the tech gap (hardware, software and in batteries) between them and competitors.

And after that their strategy is about creating a competitive advantage based on economies of scale.

First they need a scale advantage in China. And then globally. When they cite the need to “maintain leadership”, I hear achieve economies of scale versus rivals and maintain a lead in the innovation marathon.

And at first glance, this strategy appears very similar to the standard China manufacturing playbook.

A bit on that.

The Winning Formula for Chinese Manufacturing

China emerged as a manufacturing giant in the 1990’s. They followed the manufacturing to the world playbook pioneered by Japan and Korea. And later copied by Taiwan and Singapore. The 1990’s is when “Made in China” became a common phrase.

China began with simple products like toys and socks. But over time, it became much more about laptops, drones, and smartphones. Today, the manufacturing frontier for China is automobiles, ultrasound machines and industrial robots.

And this was mostly about scale. Not cheap labor. I called Manufacturing Scale as one of the six mega-trends of China in my One Hour China book.

Economies of scale is a production and supply-side advantage. For Chinese manufacturers, the playbook was (basically) the following.

- First, you need outstanding management and operating performance. There were tons of manufacturing companies and you had to fight your way to the top. It’s pretty brutal.

- Then, over time, you achieve superior scale in manufacturing, production, and the supply chain. The leaders in each sector got economies of scale in production – which resulted in:

- Lower per unit production costs.

- Purchasing power in the key inputs (sometimes).

- The next step was to outspend rivals in R&D. Basically, get economies of scale in R&D. This made a huge difference in certain sectors. Such as telecommunications equipment (Huawei), white goods (Geely) and laptops (Lenovo). It didn’t help much in others, such as toys.

- Finally, you try to ride any waves of government support. When the Chinese government announces its big strategic priorities, such as the Belt and Road initiative and solar and renewables, you focus on these areas if you can. That will mean lots of tax breaks and government contracts. And sometimes you can get lots of cheap credit that lets you build out scale rapidly. This can be a significant advantage internationally.

That’s the main playbook. Outside of this, you could sometimes achieve:

- Barriers to entry due to the capital and operating base created. Especially if it is highly specialized. Although this is only sometimes.

- Process power advantages. One of Hamilton Helmer’s 7 Forces.

But this playbook was mostly about achieving competitive power with operating performance and production / supply side advantages. There is very little competitive power on the demand side. No real branding power. No loyalty or customer capture. Global manufacturing is a pretty tough business.

China’s winning formula in manufacturing has (mostly) been:

Manufacturing scale + R&D scale + (credit and other State support)

We can see this in industry after industry. Laptops. Smartphones. Solar panels. Refrigerators. Farm equipment.

So why hasn’t this worked in automobiles (yet)?

This is mostly because:

- It took +20 years for the China auto makers to get technically sophisticated enough to make anything other than low-cost economy cars (think Great Wall, Geely). Even five years ago, the foreign joint ventures in China were still dominating domestically (SAIC-Volkswagen, SAIC-GM).

- There were entrenched incumbents in the major foreign markets. Toyota and others were dominant in Japan. Volkswagen and others were dominant in the EU. And these entrenched incumbents had well-established supply chains. Plus, huge numbers of existing customers already using their financing. Plus, huge numbers of repair shops with mechanics and inventory for their models.

But three things have happened that have created a window of opportunity for companies like BYD.

- A significant technological change with EV / AV. This is creating an opening. Plus, you don’t need engines or their supply chains anymore.

- China’s big advantages in lithium and battery production.

- Big State support for Chinese EV companies.

All the stars have aligned for Chinese EV makers to break into the global auto markets. And they are moving very fast. And BYD is really out front.

Ok. That’s pretty much how I see BYD. A standard China manufacturing-to-the-world story.

However, there a couple of good concepts in this.

Concept 1: Money Wars and Last Man Standing

I talk about both of these pretty often. They are so common in China. They get written about a lot because they’re pretty exciting.

Money wars is just using your balance sheet to hurt your competitors. This is usually by discounts and subsidies. Or giving away free stuff. It’s pretty common in difficult markets. But it’s also common in new industries, where everyone is fighting for growth and market share.

That’s what BYD is doing. And really all the EV leaders are fighting for growth and to maintain their leadership positions. That’s Tesla, BYD, Toyota, and a few others.

And, big surprise, they are not thinking much about profits. They are flooding money into growth, market share and rate of innovation. I list this under Tactics (T5). Here is an article on that:

However, in China we see a much more brutal version of this.

There are tons of EV companies. And everyone knows that most will be gone in 2 years. So, they are all offering crazy subsidies to get people to buy their cars. One of the biggest methods is to offer services. If you buy certain car brands, they will give you free charging for years. They will give you free maintenance for years. I know one guy who bought a leading China EV model, and he gets 2-3 hours of free labor every week for like ten years. The auto maker pays for someone to come to his house every week and wash his car. Or do whatever else he wants.

I call the China version of money wars “last man standing”. It’s when everyone bleeds cash because they have overbuilt production, dropped prices, or are just giving away free stuff. You make everyone in the market bleed cash. And whoever dies last (i.e., remains standing) wins the market. Here is an article on that:

Concept 2: Barriers to Exit and Irrational Competition

Money wars can make sense for the market leaders. Whether its BYD vs. Xpeng in auto or Disney+ vs. Netflix in streaming.

But what about the laggards?

What about for the incumbents being disrupted?

Should Fiat be subsidizing electric vehicles? What about Paramount in streaming? At what point does a money war just become irrational competition and behavior? If there is little to no chance to win, is it mostly about management not wanting to lose their jobs?

We are seeing irrational competition in lots of EV startups and legacy auto companies.

Part of this is the high barriers to exit of traditional auto.

Everyone understands barriers to entry, which can be a good source of protection. But there can also be big barriers to exiting a business. When the market slowed down during Covid, it was easy for Starbucks to close up a bunch of outlets. And even to exit entire markets. They can sell their assets easily (real estate, tables, espresso machines). And they can do this in a stepwise fashion.

But some businesses cannot scale down easily. You cannot close down 10% of a department store or a theme park. It’s all or nothing.

And some assets are specialized and can’t be sold or re-purposed into another business. Land is valuable so it can be sold. But specialized and customized factories are basically scrap.

When a business has high barriers to exit, you see a lot more irrational behavior by management. This is going to be a big thing in legacy auto company.

Concept 3: EV Has Tons of External Factors, Risks, and Uncertainties

When I look at EV / AV, I see a long list of risks and uncertainties. It is a big and complicated business. And so many things can go wrong. And many of these things are not under management control. There are endless external factors, risks, and uncertainties.

I like chocolate businesses like Snickers and Twix. Literally everything is under management control.

- You buy the ingredients (easy as they are commodities).

- You make the candy bars in your factory. You can churn them out all day long.

- You ship them to retailers, where they can sit on their shelves for months.

It’s really under your control.

Compare that to selling apples.

- You have to grow the trees, which can take 3-7 years before they can bear fruit.

- The tree and the apples require land, water, and fertilizer. And you are impacted by weather, water availability, bugs, and other factors.

- Then you have to pick the apples (kind of difficult) and ship them. The supply chain is more complicated because they are perishable and easily damaged.

- And then they can only sit on the shelves for 1-2 weeks.

You are at the mercy of so many things outside of your control (especially time). Ultimately, it’s a slowly produced, short lived, commodity product. Snickers is an easily produced, long-lived, highly branded product.

Now, think of all the external factors, risks, and uncertainties for BYD.

- The supply chain is a big challenge. You need lithium and batteries. This is a problem for Tesla. BYD has real advantages here.

- You need semiconductors. There is a global chip shortage to begin with. Plus, BYD is a Chinese company, and the US is creating lots of sanctions on chips. BYD is making their own chips in-house.

- Big innovation is required in batteries. The entire field has to advance for this to work at scale.

- Big innovation is required in AI. Elon Musk has said Tesla basically had to solve the problem of real-world AI to get self-driving to work. BYD will have to do the same.

- Regulations and protectionism are going to be a big factor. European countries do not want to see all their automakers go out of business. Neither does Japan. Watch for limits on Chinese imports.

- State support is a big factor. EV / AV is a strategic priority for China, Germany, and Japan. Historically, China and Japan are very effective at providing State support. The US is not very good at this.

Anyways, reading the BYD and Tesla annual reports, it is shocking how many risks are listed. It is one daunting problem after another.

Last Question: How Will AI Change the Competitive Dynamics of EVs?

The picture I have painted is one of manufacturing. Going from combustion engines to electric vehicles is still mostly a manufacturing story. And BYD is well positioned in this. It has deep expertise in batteries, manufacturing, and the China market. They have tons of car models. Tons of manufacturing expertise. And they now have huge scale as the national champion in world’s largest EV market.

But Tesla is increasingly a real-world AI and robotics company. And cars just happen to be their first robots.

If EV/ AV is going to increasingly be about software, AI, and data, then this is not going to be mostly about design, manufacturing, and global sales. The nature of auto companies and competition is going to change.

I still see BYD mostly in terms of manufacturing. But I’m watching closely for when it becomes more of a digital and AI business (my area). I think we’ll know the new dynamics in about 2-3 years. Tesla will be the leader. But I expect BYD to copy them very quickly.

***

That’s it for Part 2. I hope this was helpful. Cheers, Jeff

———–

Related articles:

- BYD Is Going for Global EV Leadership (1 of 2) (Tech Strategy – Daily Article)

- A Breakdown of the Verisign Business Model (2 of 2) (Tech Strategy – Daily Article)

- 3 Factors Will Determine the Future of Verisign Inc. (Tech Strategy – Podcast 191)

- A Strategy Breakdown of Arm Holdings (1 of 3) (Tech Strategy – Daily Article)

From the Concept Library, concepts for this article are:

- Money Wars and Last Man Standing

- Economies of Scale

- SMILE Marathon: Sustained Innovation

- Irrational Competition and Barriers to Exit

- Auto EV AV

From the Company Library, companies for this article are:

- BYD

———

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.