I recently visited Mercado Libre’s headquarters outside of Sao Paolo and had some interesting discussions with management. It was a great visit and Mercado Libre is really an interesting company in terms of strategy.

The core ecommerce business is what you would expect for a large regional, multi-country marketplace. And the expansion from ecommerce into payments (and now fintech) is something we have seen many times before. Mercado Libre has a pretty standard playbook for ecommerce in developing economies.

It is the rate of its ecommerce growth and of its development fintech that will determine the future the company. Those are the big unknowns. And you get very different answers to these questions in Latin America than in Asia.

In this article, I’ll go into the three questions I think determine the future of Mercado Libre. But first some basics for the company.

An Introduction to Mercado Libre

Mercado Libre (literally “free market” in Spanish) was founded in 1999 by CEO Marcos Galperin while he attended Stanford University. Originally founded in Argentina, it quickly became regional with most of its focus on the large Brazilian market.

Today the company covers 18 countries (basically all of Latin and Central America) and most of its revenue comes from Brazil, Argentina, Mexico, and Columbia. In 2007, it became the first Latin American technology company to be listed on the NASDAQ, under the ticker MELI.

The company describes itself as having “six integrated ecommerce and digital payments services”:

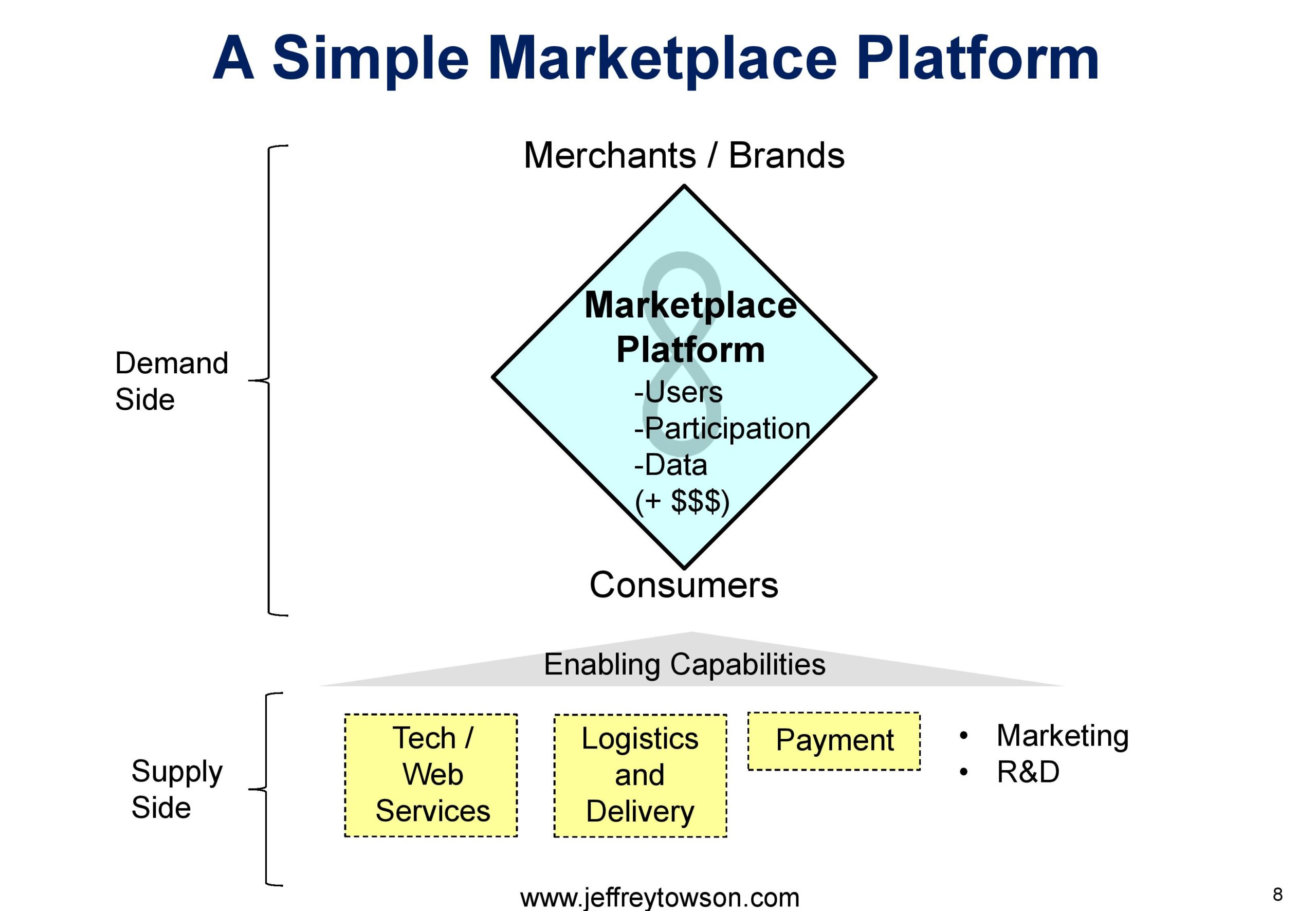

- Mercado Marketplace is its ecommerce platform, which matches buyers and sellers and enables the sale of products. The company does do some business as a retailer itself, but it is overwhelmingly a third-party marketplace.

- Its value proposition to buyers is its large assortment of affordable products. This is a much larger selection than is available to buyers online or offline in most of its markets.

- Its value proposition to sellers is access to a larger and more geographically diverse user base. And it provides this access at a lower overall cost and investment than offline options. Additionally, they offer payment settlement and shipping solutions. And, of course, ad services for promotion.

- Mercado Pago is its payment, credit and fintech platform. This service began as digital payments on the marketplace and has since expanded to a suite of financial services, for both on and off the marketplace (depending on the country). More on this below.

- Envios Logistics is its warehouse and delivery service. The company mostly uses third parties for delivery, warehousing, and other fulfilment services. The company provides the digital architecture and integrates the technology into the marketplace. Sellers are encouraged to use this service to offer a more integrated experience and to get discounted shipping.

- Mercado Ads is its advertising business.

- Its Classifieds service focuses mostly on real estate, auto and services. It charges fees based on listings, not as a percentage of final sale value. The classifieds attracts a lot of users.

- Mercado Shops is the storefront solution it offers to small and medium-sized merchants so they can open virtual stores.

That’s how the company describes itself. You can see that except for Mercado Pago this looks like a standard marketplace business model. And you can easily place 5 of their 6 services on the below graphic.

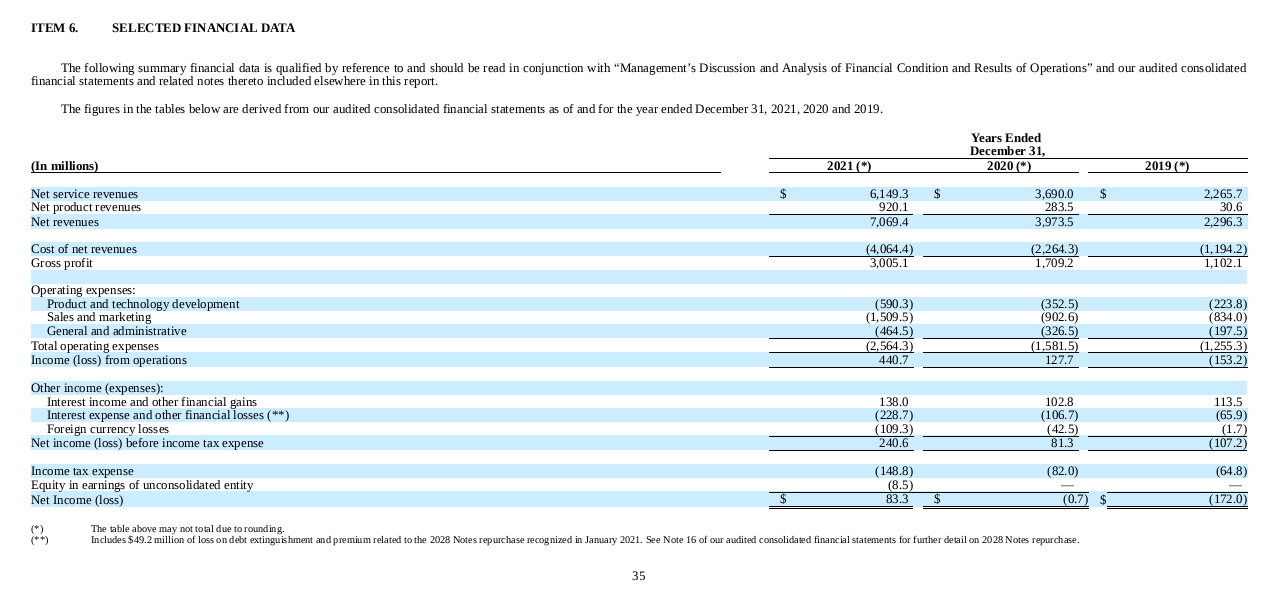

As for the financials (ignoring the fintech), they look pretty good.

Note:

- Net revenue growth of 78% (2021). And of 73% in 2020. This is very rapid growth and has a lot to do with Covid. But it’s still pretty great.

- Gross profit of 42%. And this is relatively stable. That is fantastic. Cash Gross Margin (the most important number) in 2021 was $3B.

- Operating profit of 6%. This has been increasing and likely reflects management’s focus on growth. Sales and Marketing has been decreasing over time (from 36% to 21% in 2021). I assume this spending can decrease to 15%, which would make operating profit around 12-15%.

Overall, the numbers look good – and are similar to what we see at other ecommerce marketplaces.

It’s also important to note that net revenue comes from multiple sources. The “commerce revenue” (i.e., not “fintech revenue”) comes from:

- Marketplace fees – which can be final value fees and/or flat fees.

- Shipping fees – which differ if the company is acting as an agent or the provider of the service.

- Classified fees – which are flat fee for listing.

- Ad sales

- First party sales as retailer.

- Annual business fees

That list is the tell-tale sign of a business that creates value by enabling interactions, as opposed to providing a service. Revenue comes from lots of little sources within the ecosystem.

***

Ok. With that, let me jump to the three questions I think will determine the future value of the company.

Question 1: What is the Rate of Growth for the Ecommerce Business?

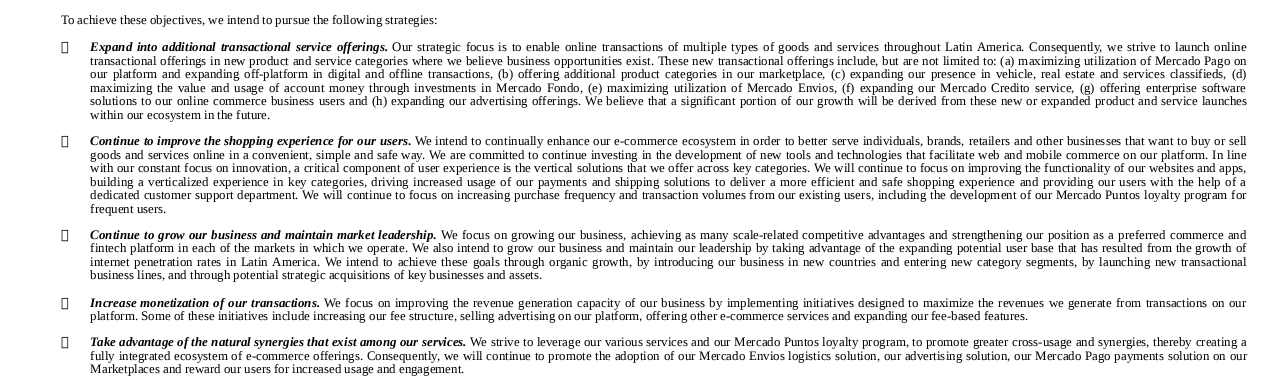

Mercado Libre details five strategies. And these are all mostly about growing the core business. From the 10k:

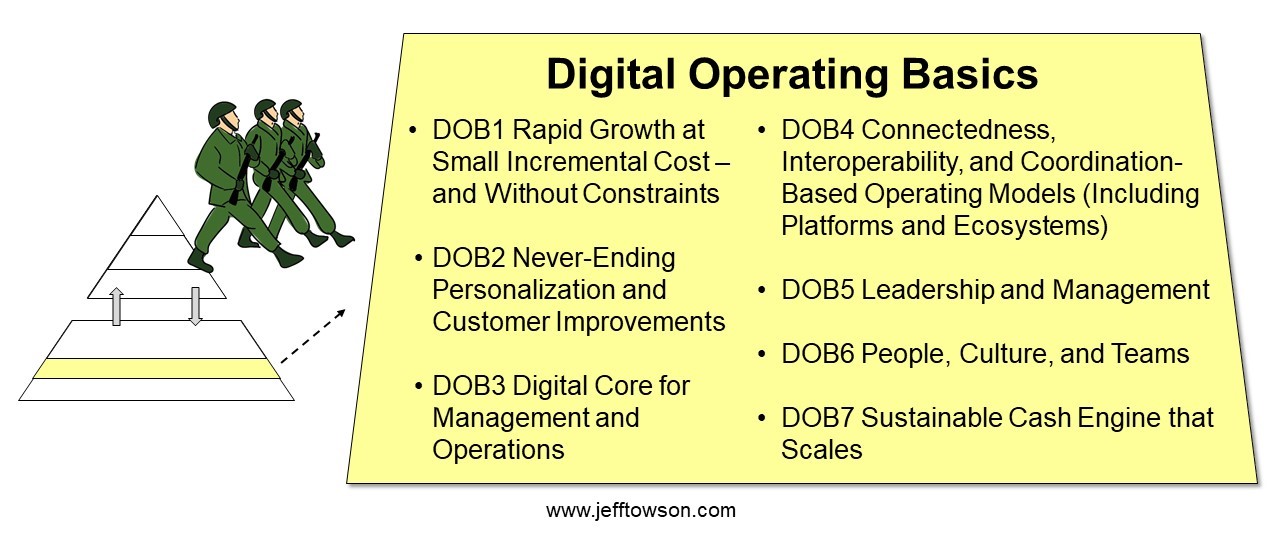

For those of you who have been reading me for a while, these strategies should look familiar. They are basically Digital Operating Basics 1-2 plus a focus on building network effects and economies of scale.

Mercado Libre’s first strategy is to “expand into additional transactional service offerings”. This is DOB1, which is about getting bigger. Go for very large scale, which can be done cheaply and without natural constraint in a digital business. It is one of the things digital businesses can do much better than traditional physical businesses.

Their first strategy is basically about doing more of everything on the core marketplace platform. Do more transactions by increasing product categories, by getting more usage of logistics, by getting more usage of classifieds, and so on. It’s about growing the core ecommerce platform.

Their second strategy is to “continue to improve the shopping experience for our users”. This is DOB2, which is about never-ending customer improvements. Mercado Libre talks about improving the experience for all users (individuals, brands, retailers, sellers, other). For Mercado Libre, this means continuing to invest in new tools and technology, constantly improving the shopping experience and improving customer service. They also mention their focus on “verticalized experiences”, which is interesting.

Ultimately, improving the user experience is about staying competitive versus rivals. And about increasing purchase frequency and transaction volumes.

Their third strategy is to “continue to grow our business and maintain market leadership”. Note their comment about achieving “scale-related competitive advantages”. And notice how they focus specifically on market leadership. This strategy is not just about growth. It’s about growing faster than their competitors and staying larger than their competitors (i.e., maintaining market leadership). This is about building their competitive advantages. It’s about maintaining a scale advantage over rivals. And then exploiting that as a competitive advantage.

They don’t’ say which competitive advantages they are building explicitly but they do mention scale. And what they are really doing is building demand-side scale advantages (which we call network effects) and supply-side scale advantages (which are economies of scale in fixed costs in this case). This strategy is about building competitive advantages.

Their fifth strategy is to “take advantage of the natural synergies that exist among our services”. This language should also sound familiar to long-time readers. They are talking about cross-selling and bundling, which we list as Soft Advantages (SA1, SA2).

***

Ok. So question 1 is how fast is the core ecommerce business going to grow? And how much of a competitive advantage will this company have versus rivals? Those two questions will determine long-term operating profits.

Not counting Mercado Pago (see question 2), I think their core growth rate will mostly be determined by the ecommerce development rate of Latin America, especially in Brazil, Mexico, Columbia. As the clear market leader, Mercado Libre is not going to be impacted much by rivals in ecommerce. Their growth rate will mostly be determined by external and macroeconomic factors. And if you read the risk section of their 10k, this is mostly what they talk about. The major risks they cite are all about government actions, consumer spending and technology adoption rates.

Question 2: How Will Mercado Pago Fare Against Fintech Rivals and New Entrants? And With Rapidly Changing Brazilian Regulations?

Mercado Pago is the biggest unknown for this company. Over time, this service has grown from on-platform payments to a suite of financial services. And it has increasingly moved off-platform (in a handful of countries). Services today include:

- Payments for utilities, mobile top, and other consumer services.

- Prepaid cards and debit cards (tied to digital wallets) that can be used in the physical world.

- In-store physical payments by mobile POS devices to SMEs.

- Mercado Credito which provides merchant and consumer credit. This can be on the marketplace or off (with credit card).

- Some insurance products (such as extended warranty).

- Mercado Fondo, which is their money market fund and their major move into wealth management products.

- Crypto savings wallets (launched in 2021).

This is all pretty similar offerings by Ant Financial and others. And these services also create a complementary payment platform. I’ve discussed this strategy many times before, which you can read about here.

That’s interesting. But I am not really factoring this second platform into their future value. Too early stage.

What I am factoring in is how credit services are changing user behavior of the core marketplace platform. Credit has some really interesting effects on user engagement. Note the following comment in the 10-K.

Note the phrase “credit is a key service overlay that enables us to further strengthen the engagement and lock-in rate of our users, while also generated additional touchpoints and incentives…“.

Credit and payment really create new types of user behavior. And this happens in both the digital and physical world. I view credit as a service that can amplify other services like ecommerce. And this can become even stronger as you move from credit cards to consumer loans.

Similarly, Fondo, the asset management product in Argentina, Mexico, and Brazil, gives users other interesting incentives. It definitely creates an incentive to fund wallets with cash that is not just for purchases. This cash can then be accessed for payment, prepaid cards, investments, ATM withdrawals and so on.

They are already referring to asset management as a pillar of their “alternative two-sided network”. So they are thinking about Mercado Pago with asset management as a secondary platform, similar to Ant Financial and NuBank.

But the big issue for Mercado Pago is surging competition.

Credit card companies, payment processors, established banks and digital natives (e.g., Nubank) are very active in this space. Brazil, in particular, has emerged a leader in fintech. Thanks largely to a particularly aggressive and innovative central bank. Unlike in ecommerce, it is not clear that Mercado Pago will end up a market leader in fintech. It’s a rapidly evolving and hyper-competitive space in Latin America. And regulations are changing rapidly, which is disrupting virtually everyone.

I am largely looking at Mercado Pago as an amplifier to the ecommerce business. But the fintech revenue is significant and growing.

Final Question: How Much Tech Bloat is at Mercado Libre?

Silicon Valley is currently laying off tens of thousands of tech workers. And Elon Musk has clearly set the high-water mark by exiting 80%(?) of Twitter employees. This is fairly expected after the huge increases in headcount at most all the tech companies in the last 3-5 years.

Mercado Libre has similarly increased its headcount dramatically in the past 3 years.

- In December 2020, Mercado Libre had 15,546 total employees. By the end of 2021, it had doubled to 29,957.

- In December 2019, Product Development and Tech staff totaled 1,709. This increased to 5,201 in 2020. In December 2021, it reached 9,491.

So is there a lot of tech bloat at Mercado Libre?

Probably. But to be fair, these staff increases do track increases in revenue, which was definitely not the case at Twitter. There is a cost reduction number that can be figured into future value.

***

Ok. Those are my three questions for Mercado Libre going forward. Overall, it’s an interesting company that is doing very well.

Cheers, Jeff

Here are some more mural pictures from Sao Paulo

——

From the Concept Library, concepts for this article are:

- Digital Operating Basics 1: Rapid Growth at Low Cost and Without Constraints

From the Company Library, companies for this article are:

- Mercado Libre

———-

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.