I wrote about Alibaba’s 5 growth strategies under “Domestic Consumption”. But CEO Daniel Zhang has also outlined 5 growth strategies for Alibaba Cloud. And their cloud business is what everyone has been speculating about. It’s the most exciting growth opportunity but it also has the greatest uncertainty.

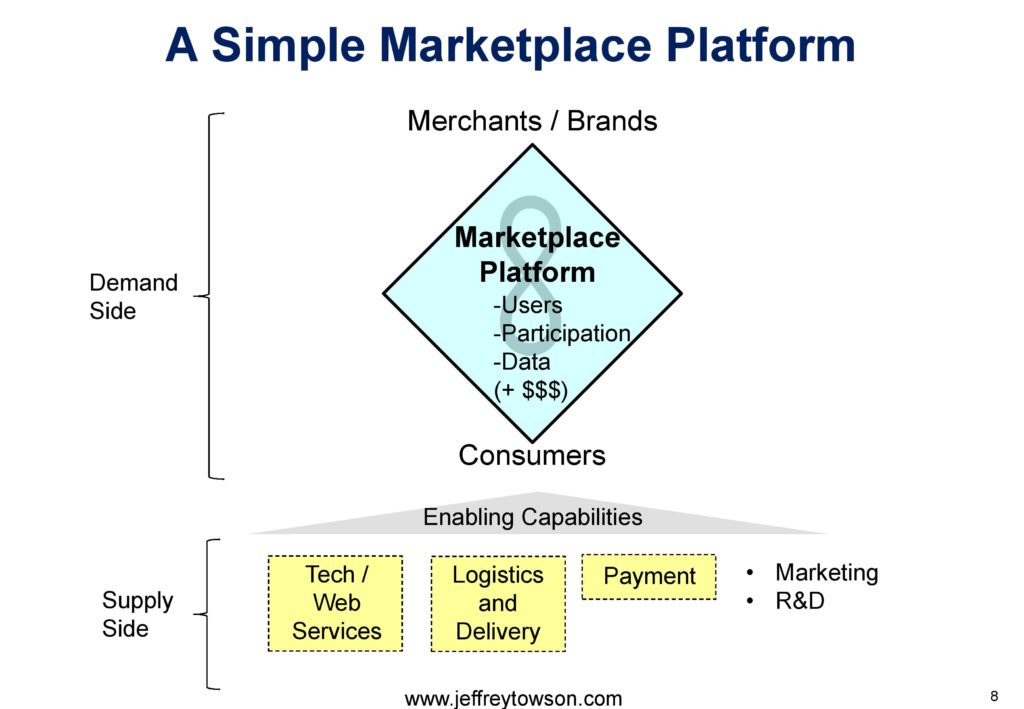

I’ve argued Alibaba is 100% in the platform building business. Everything they do is a platform. This is where they get most of their various structural advantages. Although the company is really complicated at this point. The core 4 ecommerce platforms are all like the below:

If you can take apart their ecommerce businesses, you can get a solid read on their core financial performance. But what about cloud? Because this is what they say is their big future growth. Note the below graphic from their investor day.

The bottom level is “Seeds“. That’s a lot of experimentation and projects in the early stages. This is testing for product-market fit and working out the software. If a project gets going and it starts to scale, they put them move it to “Traction“. Again, Alibaba is in the digital platform business and getting platforms to a critical mass of engagement and users is critical (and also difficult). But once they get some “traction”, the big strengths of platform business models start to show up – especially:

- Network effects.

- Soft advantages like price subsidies and chicken-and-egg.

- Scalability based mostly on user effort and capital.

Growing projects then, sometimes, get to “Profitability“, which you can see at the top. And they show their ecommerce companies Taobao, Tmall, Alibaba.com and 1688. Ant Financial is another one but is not shown on this slide. But the big new one at this level is Alibaba Cloud. And they have said this is going to be profitable (hence the category on the chart).

It is important to note that you can have all the strengths and the competitive dynamics of digital platforms and still not be profitable. As Uber has discovered, competitive dynamics are a requirement but not a guarantee of attractive unit economics. Youku and other China video platforms (audience-builder platforms) are famous for losing lots of money. The costs of content vs. ad revenue just doesn’t work (yet). In contrast, marketplace platforms, gaming platforms and payment platforms have traditionally been very profitable.

What jumps out at me about this Alibaba chart about growth is:

- Most everything listed is a platform business model. Freshippo looks like the only thing that is not. And I consider this mostly infrastructure. While it is bringing in revenue, it is not obviously scalable. It looks like a more traditional business with lots of digital innovation (so far).

- The big profits are coming from ecommerce (B2C) today – and likely from Ant Group in the future. It is also interesting how they view Alibaba.com and 1688.com (their wholesale businesses). People don’t pay enough attention to what these B2B businesses are doing.

- Cainiao is probably misplaced on the chart. I think they view logistics as a potential source of profits one day. But more like infrastructure for ecommerce today.

Which brings us to Alibaba Cloud.

Cloud is a New Animal

It’s hard to describe what cloud services are. Because they don’t really have an equivalent.

- On one level, it is like a new infrastructure for digital. Companies and developers used to build for PCs and for on premise servers. That was the main digital space and that was where the computing power was.

- Then attention and usage shifted to the web and everyone started building webpages. Computing power was still in PCs and servers but it was the web that was providing connectivity.

- Then attention shifted to smartphones and everyone started building mobile apps. Connectivity grew dramatically but computing power was much less.

People now argue that the cloud is next computing and connectivity space. It will be the big frontier that everyone builds on.

Ok. That argument is mostly true. And I like that it highlights that this is ultimately about the continued advance of computing power and connectivity. Those are the two forces shaping all this.

But the cloud (distributed computing plus connectivity) is also much more than this. Yes, it is making everything smart and connected. But there is also a long list of services and technologies associated with the cloud. Such as:

- Cloud computing and storage

- Databases and data centers

- Big data and analytics

- AI / machine learning

- Enterprise grade software

- Consumer software

- Network devices

- IoT devices and their operating system

- Cybersecurity

- 5G and other types of connectivity

- Robots and autonomous vehicles.

- Edge computing

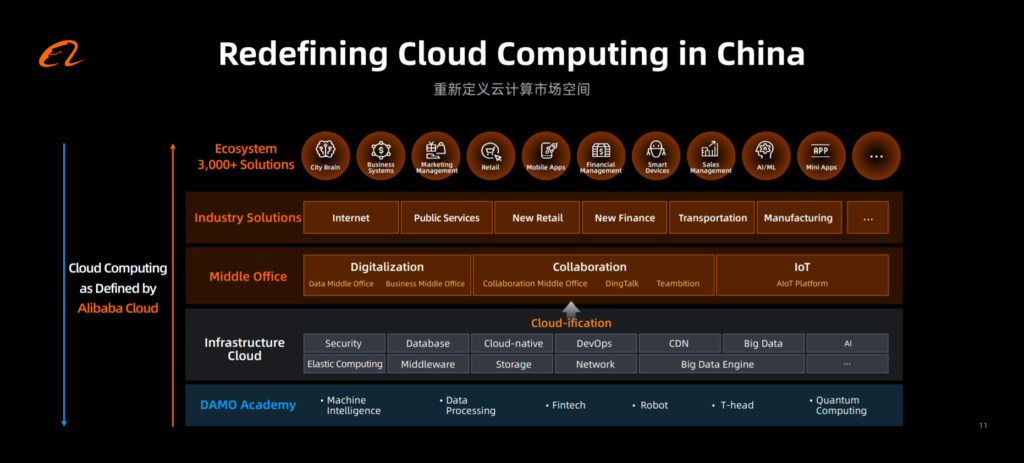

There is just a ton of stuff happening in this space. That’s why it is so unlike anything we have seen before. Here is how Alibaba describes it:

Yeah. It’s pretty confusing.

Is Cloud an Ecosystem or a Platform?

I have argued that platforms are simplified versions of ecosystems (connected companies that engage in coordinated activities). And platform business models enable relatively simple interactions between users within an ecosystem (by lowering Coasean transaction costs). I think this is a solid definition.

Ecosystems, however, is sort of a catch-all phrase. It can be everything from an industry to a country to a small town. A rain forest can be an ecosystem So can the automobile supply chain.

I view an ecosystem as a collection of companies, customers and assets that all interact. Often, ecosystems are about partners working together to create something that could not be done by any individual company. This happens in technology often due to the interoperability requirements of chips, software, data and so on. And ecosystem strategy can be a big topic when a major technological shift is happening and everyone has to work together to get it to launch.

I mostly consider platforms as simple versions of an ecosystem. Yes, they are bigger than traditional firms. And they reach out and orchestrate part of an ecosystem. But it is rarely more than 1-2 key interactions being enabled. It is nothing like the complex ecosystems we see in technology, automotive, power and such. In terms of competition, traditional business competition is like checkers. platform competition is chess and ecosystem competition is 3D chess.

Note how Alibaba describes its “ecosystem partners”:

The cloud (and Alibaba Cloud) look to me like a major effort in ecosystem building. In fact, depending on what the cloud is capable of doing, this may be the biggest most important ecosystem the human race has ever built. There are so many moving parts and unknowns. It is such a vast undertaking.

- Will all the businesses run on the cloud? Just parts?

- Will the cloud increasingly make decisions and actions?

- Will it run the factories on its own?

- Will it run the trains and airplanes?

- How many industrial robots are going to be powered by the cloud?

- How many IoT devices are going to be in homes, businesses and infrastructure?

Huawei describes its future network as “ubiquitous connectivity, pervasive intelligence”. I think that is a pretty good description of what is being built. And for Huawei, this includes smart devices, 5G connectivity and intelligent cloud. Alibaba is mostly focused on the cloud aspect.

Here are the solutions Alibaba is talking about.

This is pretty amazing. New retail, finance, public services, manufacturing, transportation and logistics, media and education. It’s sweeping.

I’m not really sure where this is all going.

What I do understand is that this going to be a game of global scale. There are two smartphone operating systems globally (Android, iOS), not twenty. There are 2-3 PC operating systems, not twenty. So I don’t think there are going to be 20 cloud businesses. The competitive dynamics and economics all look to favor scale. So I’m expecting a couple major players and then some specialist plays.

This looks like a global fight between AWS, Microsoft and Google out of the US. And Alibaba, Tencent and Baidu out of China. Alibaba is focused on China and SE Asia.

Cloud Today Is an Innovation and a Coordination (CCS) Platform

Let me suggest a simpler model for all this.

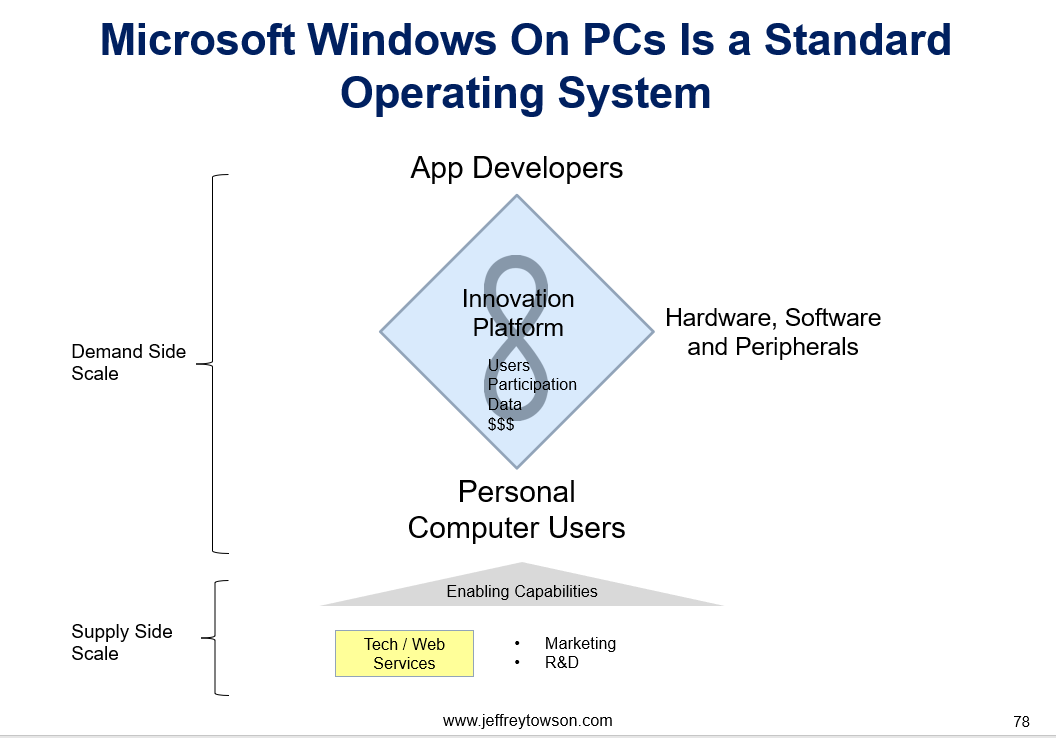

Recall, my definition for an Innovation and Audience-Builder Platform

- The primary interaction that the platform enables is innovation. It is a space for creators to build and then interact with users.

- Typically, the creators are developers and content creators. They can build products, services, content and IP on the platform.

- Can develop apps and distribute them.

- Can create content (videos, articles, music) and build an audience.

- Examples for Innovation: Google Play, iOS Store. Microsoft Windows and Android.

The graphic would look like this:

That is clearly what the cloud services are doing. They are creating a platform that developers can build their services upon. Just like Windows.

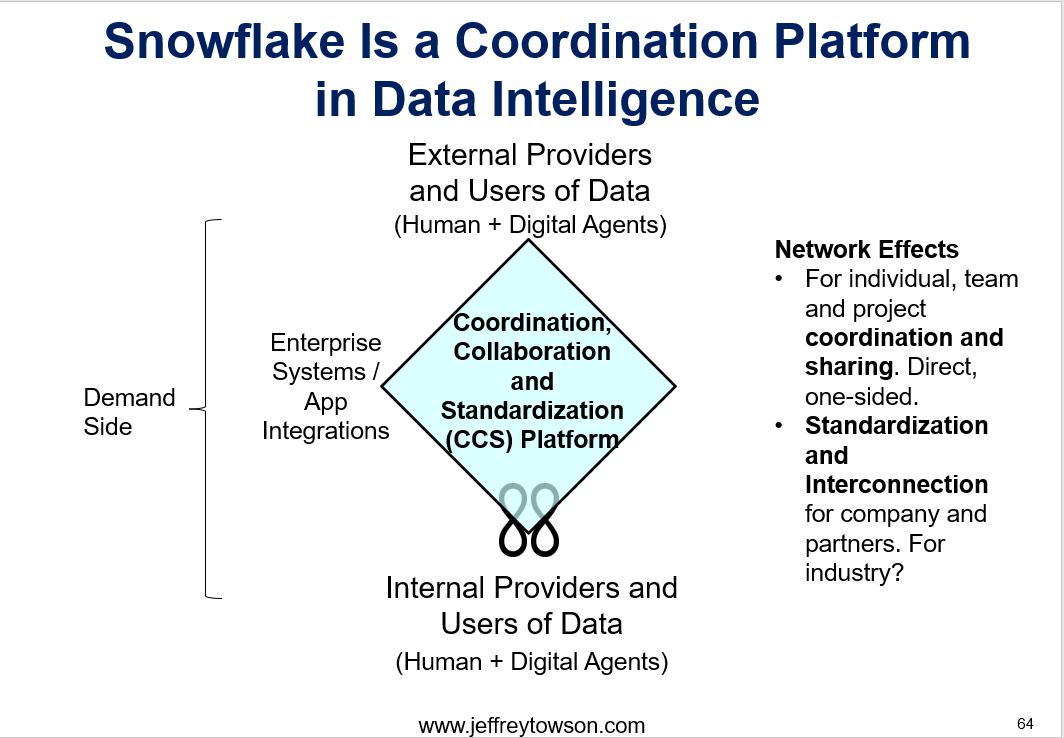

However, also recall my definition for a Coordination, Collaboration and Standardization (CCS) Platform:

- The primary interaction for these platforms is the coordination and collaboration of complex tasks.

- For example, Zoom and Slack let teams work on complicated processes at work.

- Standardization is a sub-type that is easy to understand.

- Standardizing technology standards let’s everyone focus their activities – and not create everything themselves and for every situation. Application developers only write for Android and iOS.

- Industry standards like standard sizes, 5G and Nielsen TV ratings (written into thousands of contracts)? All railroads have same size tracks so can connect.

- Other standards like pdf let people interact and share.

- Expertise standards get everyone writing in a common software language helping each other. Like everyone in town speaking the same languages

- Other sub-types include:

- Communication. Zoom, Slack, etc.

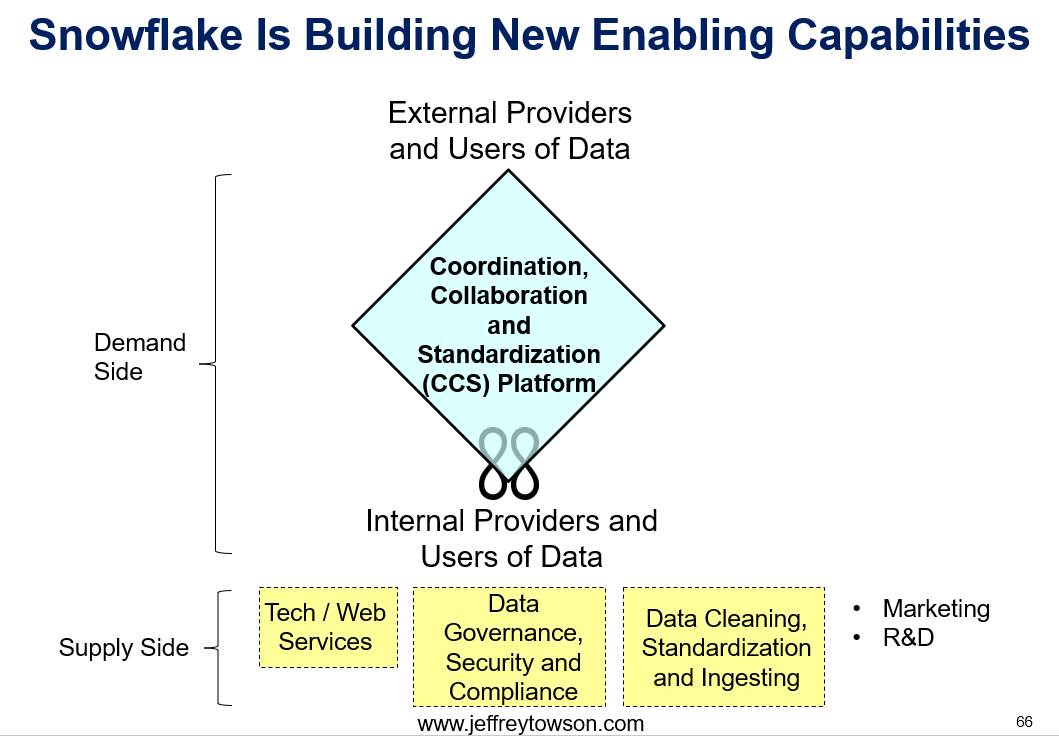

- Data Intelligence. Snowflake and Confluent.

- Team Projects. Manual and complicated projects like architecture, media creation, software development.

- Operational Automation.

Snowflake is an example of a CCS platform. And it looks like this:

Doesn’t this also sound like cloud services?

So I put them together. And consider cloud services (today) mostly an innovation plus a coordination platform. Which is what Snowflake is.

Ok. So what is happening right now?

Everyone in Cloud is Building Infrastructure, Platforms and Vertical Solutions

Everyone is building the infrastructure right now. It’s crazy. This is like railroads laying track and phone companies laying copper wire. For infrastructure, I’m keeping an eye on:

- Infrastructure services: Storage. Data centers. Cloud computing.

- Cloud-based services: Database, security, big data.

- Hardware-software integration (chips, servers)

This part is a lot about upfront costs and difficulties. Note: building the first railroad was not just about the cost. It was also the difficulty of getting the land and getting it done. This is sort of similar in that there is a big upfront hurdle. Once Alibaba gets past that, it will then be a lot about fixed costs going forward. So there is a barrier to entry and then lots of operating leverage. In some cases, things are moving quickly, like building out cloud computing and data storage. In other areas, like IoT and edge computing, things are moving slowly. A lot of this depends on adoption rates by governments and business.

As the infrastructure is being built, we are seeing an explosion of digital tools. Lots of new use cases being tried. Lots of new products and services. Sort of like when the iPhone first came out and people started making all types of crazy apps to see what people liked. The two types of services I think are pretty interesting are platform business models (of course) and vertical solutions.

As mentioned, we sometimes see platform business models emerge in industries when they first get digitized. Like how adding GPS to phones enabled platform models in transportation (Uber) and hotels (Airbnb). So we should see some new digital platforms popping up. And the cloud companies will try to take the best of these for themselves, They will let outside developers do the others. This is why Apple and Android both provide their own mapping and messenger services. But neither cares who makes the clock app.

For Alibaba, they appear to be mostly focused on DingTalk as an enterprise collaboration platform right now. DingTalk is actually in the lead in China in this area (mostly because they focused on enterprise messenger after WeChat ran the table on consumer messaging). From enterprise messenger, they will expand to video conferences, collaboration tools, team project tools and so on. Basically it will be similar to what we are seeing in the US with Slack vs. Microsoft Teams. But much simpler versions. WeChat Work, Huawei and ByteDance are also going after these platforms.

The other area to watch is vertical solutions.

Huawei often talks about how they offer end-to-end solutions that go from device to 5G to cloud. Well, this is just the cloud component of that. There are going to be lots of industry specific solutions. The ones Alibaba cites are the same ones Huawei cites: transportation, education, financial services, and retail. Some of their slides on these.

Dissecting Alibaba’s 5 Growth Strategies for Cloud.

Here are Alibaba’s 5 growth strategies under Cloud Computing. I will just run through these quickly as they are pretty vague.

“To empower consumer brands to achieve end-to-end digital operation leveraging Alibaba Business Operating Systems”

No big surprise here. They are applying cloud to their core ecommerce businesses, where they are already have tons of users. So that means financial services, IT infrastructure and merchant services are all going to the cloud – and will be informed by data intelligence. I expect them to roll out a full range of use cases here.

“To transform the entire logistics supply chain to digital and intelligent operation”

Same story.

Leveraging Alibaba Cloud into all their activities in logistics and supply chain is a natural approach. Daniel did mention they are going far beyond just digitizing packages. They are going to digitize every vehicle, courier, point of service and other asset of the logistics and supply chain operation.

“To upgrade all enterprise IT infrastructure to cloud “

More of a vision statement.

The West is far ahead of China / Asia (ex-Japan) on the enterprise side. Western companies have been building ERP systems for decades. And a lot of the effort today is about transferring from on premise to cloud.

When you look at Alibaba Cloud, you see a much smaller market today on the B2B enterprise side of China. But it will grow. And there is the question of whether that a strength or a weakness?

Note: legacy systems are often a problem when you make a major technological leap. You don’t want to make your old system obsolete or incompatible. So incumbent leaders have to make things compatible with previously deployed systems. That can be complicated and expensive. And can leave you with sub-optimal solutions.

But a new player can often start fresh and can build a better system that is much more suited to the new paradigm. This is part of why Microsoft lost when mobile operating systems emerged. It was trying to make it compatible with its PC operating system while Android had no such concerns.

China / Asia may end up having some interesting strengths in enterprise cloud because of the absence of legacy systems.

“To transform the approach to work to cloud-based collaboration”

That’s pretty vague. But I think this is DingTalk. They want DingTalk to be a robust collaboration platform with a suite of utilities for businesses.

“To build industry solutions based on cloud + big data + intelligent applications for sectors such as retail, financial services, public sectors, transportation and healthcare”

This seems to be a catch all strategy. I think they are going to do lots of meetings with companies and see who wants to build what on this new infrastructure. There will be lots of use cases and applications (platform and non-platform services). It will happen slow probably. But it could be huge over time.

***

Ok. That’s it. That was kind of a lot for today. But it’s a big important subject.

Cheers, jeff

—–

From the Concept Library, concepts for this article are:

- Platforms: Coordination

- Platforms: Innovation

- Cloud services

From the Company Library, companies for this article are:

- Alibaba Cloud

——–

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.