This is the final part on my breakdown of ARM – which is four questions:

- Is growth and value creation benefiting from a secular trend? How is it changing?

- I like companies that have a tailwind and can naturally grow.

- ARM has been riding a global secular trend (i.e., smartphone adoption) for decades. How this will change going forward is a big question.

- How strong is its customer value proposition? What is state of the core engine?

- I really like when there is great product-market-fit (PMF) on a long-term secular growth trend. And ARM has had a truly fantastic PMF for a long time.

- But I want to see how this is changing. Core engines usually need to adapt over the long-term to stay strong.

- What are the competitive strengths of the business model?

- I really like a company with great PMF on a long-term secular trend. And that is in a dominant position against competitors. This not only lets them ride the trend. It also lets them capture an outsized portion of the profits.

- ARM has great competitive advantages (as discussed). I want to see if these are getting stronger or weaker.

- Are there external CGT factors that will impact 1-3?

- The above three questions are about customers and competitors. It is a commercial picture.

- But external factors can impact this. In particular, I look for changes in consumer behavior (C), government action (G) and changes in technology (T) that can impact the commercial picture. I call this CGT.

- For ARM, the US-China situation and AI are clearly going to impact their future.

In this article, I’m focusing on these two external factors: AI and US-China.

A Bit About Changing CGT

One of my standard checklist questions is “Changing CGT”, which stands for changing:

- Customer behavior

- This is usually changing consumer behavior such as: are people drinking less sugary soda? Is the younger generation getting their entertainment from TikTok instead of TV?

- Government regulations and other actions

- Are there increasing regulations in European trucking? Yes.

- Are State actors expanding in the financial space in China? Yes.

- Technology

- This can be changing technology in products, competition, and business model.

There are lots of other external factors that can matter. But these are the big three I always look at. For ARM, let’s start with AI.

AI Will Impact ARM’s Core and Adjacent Products

The very nature of computing is changing. AI and the emergence of tech intelligence is simply an entirely technological capability. Right at the core of everything. It can’t be overstated.

- Lots of new AI-based products are emerging.

- The existing products (like CPUs) are being impact.

- Entirely new tech stacks are being developed.

So how does this impact ARM and its dominance in CPUs for smart, connected devices?

When thinking about longer-term growth trajectories, I like the work of Chris Zook at Bain’s strategy practice. He has two good books on how certain companies can grow sustainably over 10-20 years (which is rare). They are:

I did a podcast on his books:

Here is my favorite slide from Beyond the Core:

Note his focus on “companies that have a strong, or dominant, core that hit on a repeatable formula for extending their strength to new arenas”

I like three things he talks about:

- That most all sustainable growth is based on 1-2 strong cores. And there is a need to continually adapt the core over time.

- You want to make a distinction between core vs. adjacency in both products and growth.

- A dominant core has a repeatable formula. It’s a lot about doing the same things over and over. With subtle adaptations.

Adapting the core can be:

- New products / services

- New customers – microsegments

- New geographies

- New businesses.

The biggest question I have for ARM going forward is: How much of their core product (ISAs for smartphone CPUs) is going to be impacted by AI?

Keep in mind, ARM initially succeeded because existing CPUs for personal computers could not adapt to mobile devices. And Nvidia initially succeeded with its GPUs because CPUs could not adapt to graphics-intensive computing.

- How much can current CPUs integrate AI? How much can they adapt? How much will be embedded in existing CPUs for smartphones, tablets, and other consumer electronics?

- Note: You can also consider products with embedded operating systems such as thermostats and smart watches.

- Is the future going to be combining CPUs and GPUs (which are much better suited for AI)?

- Is an entirely new type of chip and architecture going to emerge?

The below is from ARMs SEC filings. It is their description of their value proposition. Note the last bullet point where they now mention AI incorporation as a key part of their value to customers. I’m not sure I believe this.

My other question is how AI will impact ARM’s growth adjacencies. Their big adjacencies are probably ISA for CPUs in:

- Smart vehicles

- Networking equipment

- Data centers

Arm Holdings has significant market share in each of these areas. But they are not dominant like they are in smartphones.

Can ARM continue to expand from their core to these adjacencies? How will AI impact this?

These adjacencies are all new computing platforms that require chips, ISAs, operating systems, and apps. You can also consider products with embedded operating systems such as drones and industrial robots.

Recall that ARM’s value proposition is a combination of IP for high performance, energy efficient CPUs PLUS an ecosystem of technology partners.

How will AI impact the products and the ecosystems?

Zook puts growth adjacencies into six categories:

- New customer segments:

- Micro-segmentation of current segments

- Unpenetrated segments

- New segments

- New geographies

- Global expansion

- Local expansion

- New channels

- Internet

- Distribution

- Indirect

- New products

- New to world

- Complements

- Support services

- Next generation

- Just new products / services

- New Businesses

- New to world needs

- New substitutes

- New models

- Capability adjacencies

- New value chain steps

- Forward integration

- Backwards integration

- Sell capability to outside

These all look to me like #4. Zook assesses adjacency moves with 3 factors:

- The adjacency is tightly tied to a strong core.

- The economic distance is short. How much does it overlap with the core? You need a strong core or a strong position in a channel, customer segment or product line in weaker core.

- It is an attractive adjacency in terms of profit pools.

- Basically, don’t try to make the jump unless the opportunity is worth it.

- You have the ability to capture economic leadership in that market.

- Basically, you want to have a competitive advantage as an attacker and then later as an incumbent.

Looking at AI’s impact ARM, my working conclusions are:

- Their core is being disrupted. They need to adapt ASAP if they can.

- They need to prioritize the adjacency with the highest likelihood of success. In case they get seriously disrupted in the core.

- Drop everything else.

The US-China Tech War Will Continue to Hit ARM’s Revenue. But Not Necessarily Its Market Share. That’s the Key Question.

This is one of the reasons I look at Arm Holdings is because it has:

- A dominant business model.

- It sits at the center of the US-China tech dispute.

Those are my two favorite questions. Plus, the China aspect spooks Western analysts. They don’t know what to think about it. The China government stuff is sort of confusing and daunting for people. But I’m quite comfortable with it.

My take is that both governments are going to continue to impact ARM’s business.

The US government is actively and aggressively trying to limit the economic and technological rise of China. I didn’t used to think this was their goal, but now I am pretty convinced. I’ll leave the why to the geopolitical thinkers. But it’s clearly happening.

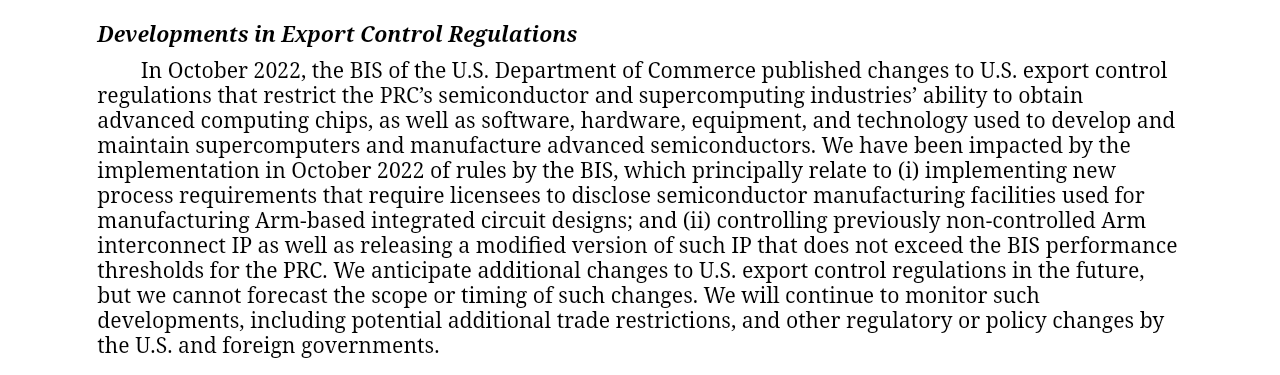

And China’s access to high-end semiconductors is the #1 target of the US government. For example, in October 2022, the US Department of Commerce added additional process requirements for licenses for advanced semiconductors. And new IP going to the PRC must not exceed certain thresholds for performance This hit the sales of chips from Nvidia, Qualcomm and others.

Note how ARM discusses this in its 10K.

As mentioned, ARM sits at the center of semiconductors and works in close collaboration with semiconductor designers, operating systems, foundries, and others. Basically, everyone that the US is looking at. They’re at the center of this.

And China is a major market for ARM. It represents about 20-25% of the annual revenue. This is not surprising as most all of the world’s smartphones are made in China.

The China government could also impact ARM. In response to the weaponization of the tech supply chain by the US government, virtually every level of the Chinese government is trying to reduce dependence on foreign companies in critical technologies – especially semiconductors. Well, that (in theory) includes ARM, with is 99% market share in smartphones.

Arm China is the exclusive distributor of Arm technology in China. It also develops and sells its own designs based on Arm. However, their stake in ARM China was sold to Softbank and the relationship is now through a sub-license agreement (IPLA) Here is their summary of the IPLA from their annual report. It’s worth skimming.

Another aspect to this is the years long fight for control of Arm China between Softbank, ARM and their former China CEO. I won’t go through that. But it’s pretty crazy. And appears to have now been resolved.

My working conclusions for ARM in China are pretty simple:

- Their China revenue is completely at risk. It could disappear tomorrow. I’ve written it out of the projections.

- The bigger problem is whether their global market share will decrease.

In Article 2, I argued that ARM’s greatest strength is its standardization network effect. It is a product plus an ecosystem and its network effect is what must protected at all costs. That means protecting global market share.

Arm Holdings needs to maintain its market share in China. Semiconductor developers and OEMs need to keep using their ISA. Then usage by developers will continue to follow. If that means giving it away for free, then just do it. That’s what Microsoft did with its software in China for decades.

Ultimately, ARM has no control over what is happening with US-China. But they 100% don’t want Chinese companies creating an alternative ISA for smartphones. That’s what I’m watching for.

Final Question: How Deep into the Tech Stack Will the US-China Divide Go?

If an alternative Chinese ISA is adopted, it will not be limited to China. It will go international with the Chinese tech companies.

We already see a tech divide between China and the US at the app layer (YouTube in the US, iQIYI in China). But this divide keeps going deeper into the tech stack. We are definitely seeing it at the data layer. We are starting to see separate operating systems (HarmonyOS vs. Android). And we are eventually going to see separate semiconductors (design, testing and foundry).

How deep will this go?

Keep in mind, other countries are increasingly using Chinese digital infrastructure. Cloud computing, data centers, payment platforms, etc. I expect semiconductor capabilities from China to also go international to some extent. Everyone knows the US could cut them off.

ARM wants to be involved in what is happening in ISAs in China. And if it goes international. Fortunately, ISAs are portable. You don’t need to build a foundry or ship a lithography machine. ISAs can be used easily by Chinese companies and developers. It’s probably impossible to track and control. ARM may not be able to maintain its payments from China, but it can probably maintain the usage. And market share is the key for ARM.

***

Okay, that’s it for this series. I hope this is helpful. It’s a cool company.

Cheers, Jeff

———

Related articles:

- The 4 Digital Concepts Powering Arm Holdings (Tech Strategy – Podcast 187)

- Ant Financial’s Big Money is in Asset-Light Credit Tech (Jeff’s Asia Tech Class – Daily Lesson / Update)

From the Concept Library, concepts for this article are:

- Semiconductors

- Core vs. Adjacency Growth

From the Company Library, companies for this article are:

- Arm Holdings

- Masayoshi Son / Softbank

Photo by Vishnu Mohanan on Unsplash

——-

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.