We visited Huawei this month with the tech tour. And we got talking about all the endless technology products they create. And what really jumps out at me about Huawei is the fact that most everything they create becomes obsolete in 5-10 years. Almost nobody uses 2G. Or old smartphones.

So when I think about Huawei, it’s not really a technology products company. It’s a human resources company. The only real asset they have is their people, who must continually create and re-create the new products.

**Disclosure:** While this coverage is unpaid, Huawei provided the LLC with travel and hotel accommodations for an event within the past 12 months.

Getting that type of sustained high performance at such large scale in technology is almost unprecedented. Think Motorola over decades. Hewlett-Packard for a long time. And Huawei.

- How do you organize and motivate +200,000 employees (most of whom are engineers) to continually create?

- How do achiever operational performance in tech at such large scale?

A few years ago, I visited the HQ in Shenzhen and asked specifically to interview the head of HR. I think I was the first guest to ever ask to meet with HR. I wanted to see their organization, policies and procedures. Here are my notes from that visits.

***

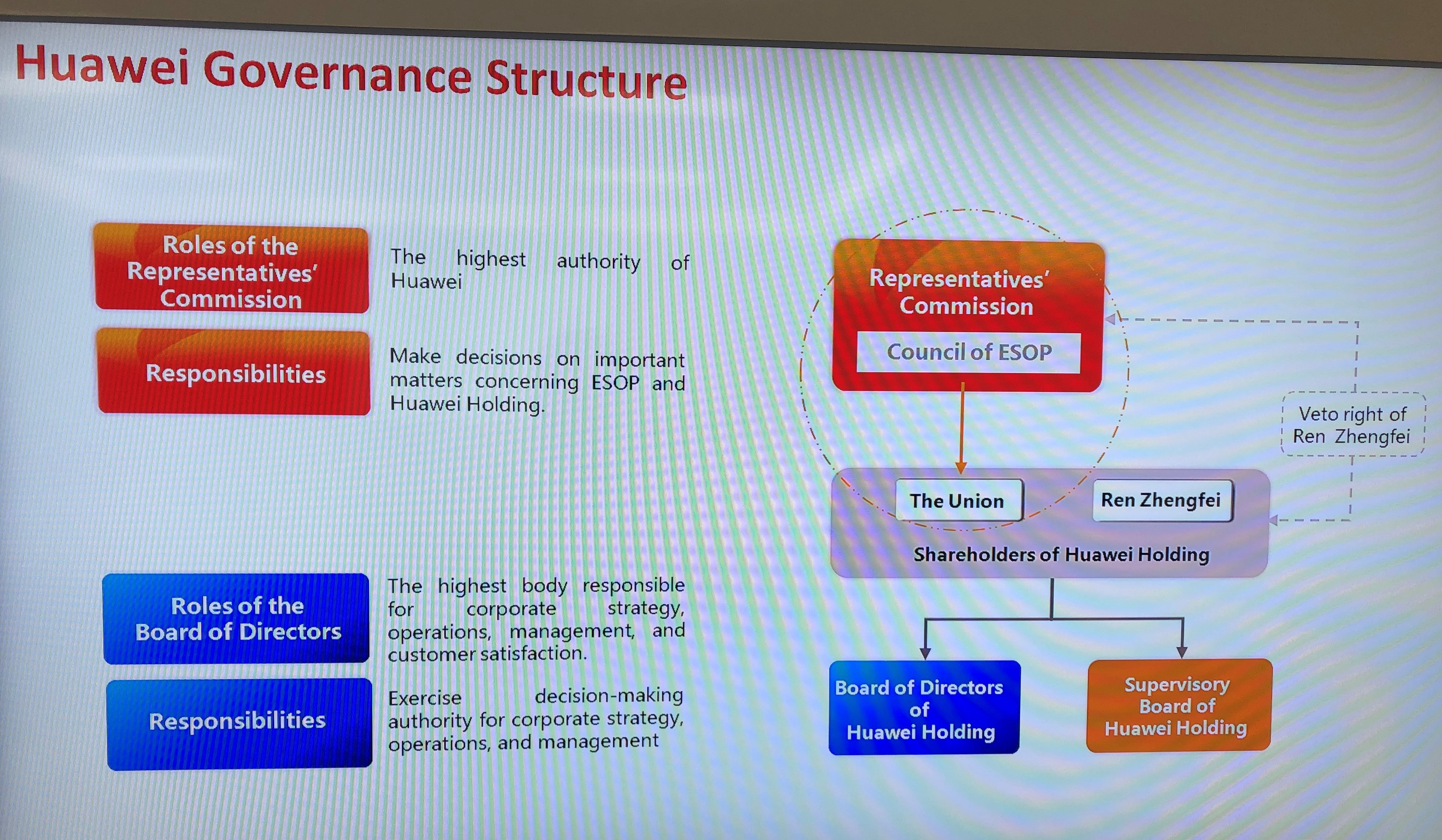

In Shenzhen, I visited the room where they keep all the records for the employee stock ownership plan (ESOP). And the staff gave me a nice PowerPoint presentation with lots of org charts and legal structures (see below).

But I don’t really understand these. And I wasn’t really paying that much attention. China business doesn’t much that run on contracts and signed pieces of paper (which are often unenforceable). It more runs on incentives and effective lines of control.

And in this regard, Huawei’s ESOP is a pretty impressive system.

To use the language of 3G founder (and Warren Buffett business partner) Jorge Paolo, Huawei’s ESOP is “meritocracy plus partnership”. But tech. And at a huge scale.

The ESOP as a Structural Pillar of Huawei’s HR strategy

In Part 1, I argued that Huawei’s employees (and their cumulative brainpower) are the company’s only real resource and defense in a rapidly changing engineering-based business.

So Huawei is very focused on how its employees create and continually re-create the value of the enterprise. My main point was that while Huawei is regarded mostly as a technology company, I think of it much more as a human resources company. They have an HR strategy that is very effective at creating incentives for their +190,000 employees. And the ESOP is a structural pillar of this HR strategy.

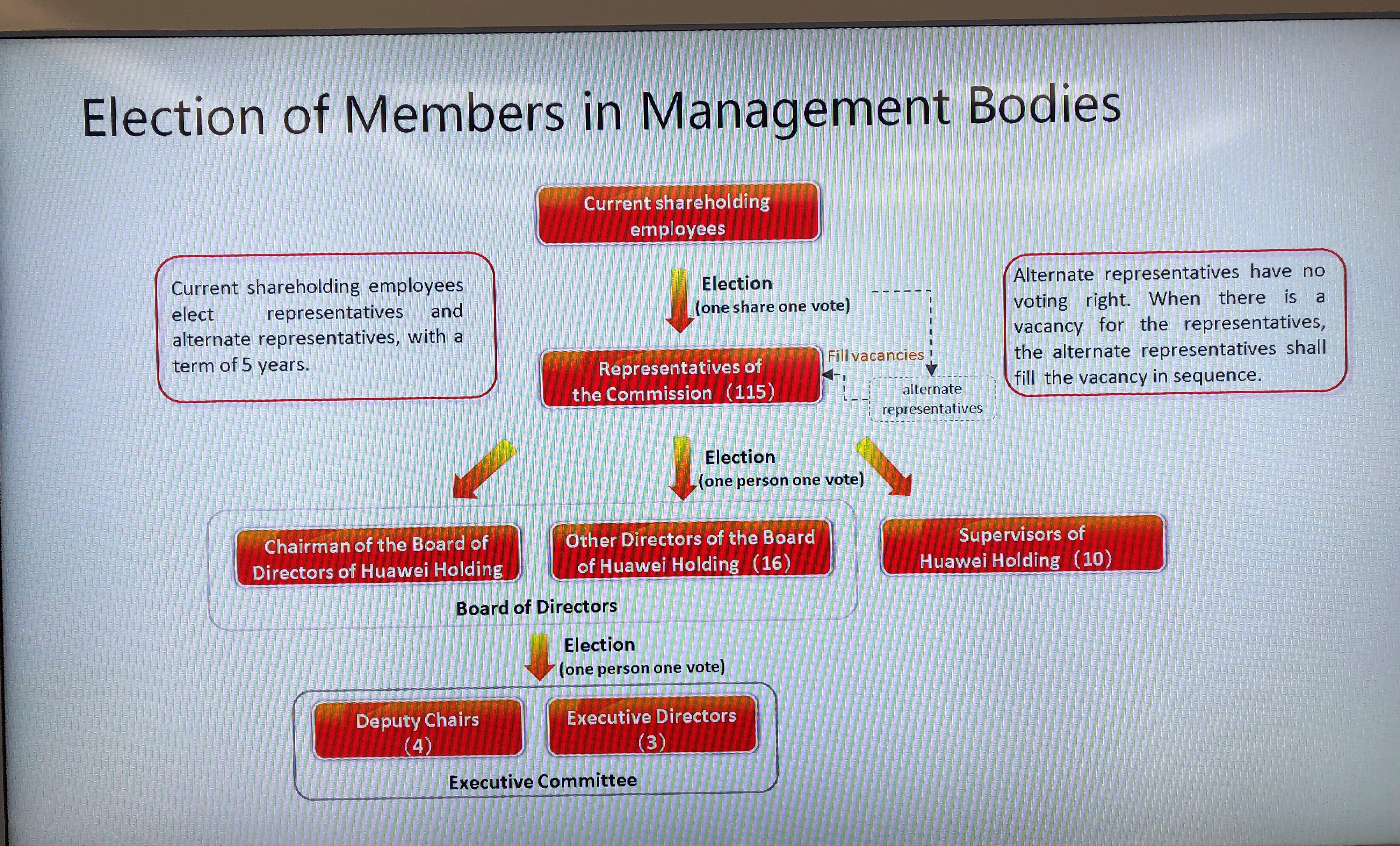

Over the years, something like +90,000 employees have participated in Huawei’s ESOP. These are employees who are identified as significant contributors to the firm and with lots of potential.

This group is identified and invited to participate in the ESOP. They can buy a certain allotment of shares per year with their own cash (no corporate matching). And I was told most of them max out their allotment. As Huawei is a private company, the share price is determined once per year by assessing the asset value of the company.

Some interesting aspects of Huawei’s ESOP are:

- Employees are invited to participate based on their assessed contribution to value. It’s not about seniority or age or years with the company or connections. They are creating a tight link between who is creating value and who is getting the economic and career benefits of that value. This is the meritocracy part of “meritocracy plus partnership“.

- If the company increases in asset value, these employees can generates significant wealth. But it if falls, they lose. Employees share in the upside and downside.

- Huawei’s ESOP, salary and bonuses are expected to be the only source of income for employees. In theory, they can’t have dual loyalties or other sources of income.

- When an employee leaves the company, he/she must sell their shares back (with a few exceptions like being over age 45). The majority of value created by the company keeps going to current, high-contributing employees. Not to ex-employees or shareholders.

- This wealth is mostly created over the long-term. There is no pay-off for boosting sales, cutting R&D or gaming gross margins in the short-term. The ESOP can create significant wealth but also requires a long-term commitment. Most Huawei employees stay for 15-20 years, which is unprecedented in China tech.

HR strategy is the aspect of Huawei that has always impressed me the most.

They have very well thought out policies and incentives. And they have doing this at a really big scale (+190,000 employees) in tech for a long time. Founder Ren Zhengfei has been talking for literally decades about how to recruit, motivate and keep top performing employees – so that the company can continually recreate itself. Effective HR at scale in China tech is Huawei’s biggest strength.

And take a moment to compare this system to how Fortune 500 companies in the US so often compensate staff, with lots of guaranteed salaries, bonuses and low priced options. It’s usually all upside and limited downside, especially for senior management. It has become common for CEOS to fail big and still get paid big.

Now compare this to the thousands of Huawei employees who could lose the bulk of their personal wealth if the firm decreases significantly in value. When Huawei talks about going into “battle mode” because of its placement on the US entity list ban, you need to picture tens of thousands of employees all fighting together against big declines in their personal wealth. How much of that type of highly incentivized behavior do you think happens at competitors Ericsson and Nokia?

I Don’t Think the Legal Structures Matter that Much

There’s a bit of political debate in the international media about “who owns Huawei?”.

I’ll address this in Part 3. But I don’t think it matters that much. Ownership isn’t that important in and of itself. What matters is decision-making ability and the distribution of created value. These are often synonymous with ownership but not always.

But you know what is better than legal claims on the distribution of value? Tens of thousands of engineers closely watching their money like hawks.

Huawei’s ESOP system is effectively overseen by thousands of internal employee watchdogs. And they work in the building. And most of them have engineering degrees. These watchdogs are the reason you can trust the Huawei ESOP, regardless of any organization chart or legal structure. Truth be told, a Chinese company with an ESOP could fool investors pretty easily if it wants to. And it can usually fool lawyers and regulators. And it can definitely fool the press. But it cannot fool thousands of engineers closely watching their money.

And this is the partnership aspect of the ESOP’s “meritocracy plus partnership”.

- You create a meritocracy that identifies who is contributing the most value to the enterprise. They have an extensive system of performance review for this.

- And then you create a partnership where the economic value is distributed to those that contribute the most, regardless of title, years, status or guanxi.

It is a powerful combination. 3G capital has been using this management strategy for decades to transform company after company. It is culture as strategy. But these were operationally simple companies like Burger King, Heinz, and Budweiser. Huawei has implemented this in tech. And at a very large scale. It’s almost unprecedented.

“Meritocracy Plus Partnership” Has Some Problems

Jorge Paolo and 3G Capital have been using meritocracy plus partnership for decades. It’s powerful. But they have also identified a few problems with this management style.

- Excessive compensation and rich employees can become a problem. The whole goal of this system is getting core employees to go “all in” on value creation at the enterprise. They work like crazy and sacrifice everything to get ahead. And it works. But this motivation can also fade as staff do, in fact, get more wealthy. Ren Zhengfei talked about this loss of motivation problem frequently. It’s one of the reasons the crisis created by the US tech ban has, in some ways, helped the company. It has reinvigorated, refocused and re-motivated the culture and staff.

- You always need more growth. Ongoing wealth creation for employees requires a continually growing enterprise. This is why 3G Capital continually looked for new companies to acquire. You can’t keep growing companies like Budweiser and Burger King at a high rate forever. So 3G bought a company, transformed it to meritocracy plus partnership and then grew it rapidly for 2-3 years. Then the company slowed to more normal growth and the team looked for another company to buy and transform. However, you can perpetually grow in technology and innovation. Like 3G, Huawei’s HR strategy and ESOP are highly dependent on long-term growth. But the company has been good at finding new opportunities for such growth. They went from telecommunications equipment to consumer products and smart devices. And then into enterprise business. And now into AI and cars.

- You need big dreams. The best employees are not motivated just by money. And especially not in tech. Top managers and engineers want to build. They want to work at the best companies. And they want to accomplish great things. Just like great mountaineers always need new mountains to climb, Huawei needs to keep finding big new dreams for its team to pursue. This is also why the best book about 3G is titled Dream Big. The US tech ban was just the kind of challenge the team at Huawei likes.

- You need serious competitors. Just like rich employees can get lazy, dominant firms can also get lazy. Huawei needs competitors to fight. And to keep the company from becoming comfortable and slow. Traditionally, Huawei has been a fast follower and has been competing with Ericsson and Nokia globally as an underdog. But these competitors are now only about a fifth of Huawei’s size in terms of total revenue. I don’t consider them to be serious threats to Huawei at this time. And this, ironically, creates a problem for Huawei. They need a strong competitor to keep them lean and mean.

- R&D is not a natural fit for meritocracy plus partnership. A final point. Highly incentivized employees create value by serving customers – and therefore generating sales. It is a direct relationship so you can measure the contribution of each team leader and team to value creation. Meritocracy plus partnership works well in sales and marketing, which is one of Huawei’s two critical departments. However, their other main department is R&D and this is not as directly tied to value creation. It’s a little harder to measure the contribution of R&D teams to value creation. Huawei has traditionally solved this by having R&D report to sales managers, who then focus on market needs. And this worked well when Huawei was mostly a fast follower in tech and R&D. But they are increasingly moving to a position of tech leadership. So how do you do meritocracy plus partnership in more pure R&D? It’s not clear to me how they are doing this.

- And speaking of R&D, below is one of the first Huawei HQs. And below that is their new R&D center in Dongguan.

****

To sum up.

In Part 1, I argued Huawei’s real strength is its HR system, not its technology. In this part, I am arguing that the ESOP is arguably the most important pillar of their HR system. It steers most of the long-term economic value created to the highest contributing, current employees – who in turn continually recreate and grow the company and its value. It’s a really good system.

In Part 3, I’ll make a couple of final points about who I think really owns Huawei.

Thanks for reading, jeff

- Huawei Is Going to Beat Trump with Human Resources, Not Technology (1 of 3)

- Who Really Owns Huawei? Their Carrier Customers (3 of 3)

———-

Related articles:

- AutoGPT and Other Tech I Am Super Excited About (Tech Strategy – Podcast 162)

- AutoGPT: The Rise of Digital Agents and Non-Human Platforms & Business Models (Tech Strategy – Podcast 163)

- Why ChatGPT and Generative AI Are a Mortal Threat to Disney, Netflix and Most Hollywood Studios (Tech Strategy – Podcast 150)

From the Concept Library, concepts for this article are:

- n/a

From the Company Library, companies for this article are:

- Huawei

———

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.