Huawei released their 2019 financial results last week. And I had the opportunity to interview Karl Song, the VP of Corporate Communications, prior so I knew what was coming (but I got embargoed). You can see that interview here.

And it was fascinating.

Step back and consider what a truly crazy year Huawei had. Has any single company ever taken that big a hit from such a powerful government?

They got hit in their access to US technology and their supply chain. They got hit their international markets for telecommunications equipment and consumer devices. And they got really challenged in their reputation with carriers and governments around the world.

How the Huawei executive team responded to all this is going to end up being the ultimate Harvard Case Study on crisis management.

And all of this played out in their 2019 financials. The numbers don’t just reflect the short-term impact. They also reflect how Huawei responded for the short and longer terms.

And I think there are 4 things think people are getting wrong when looking at these numbers.

#1. The financials show a switch from aggressive growth to long-term survival.

Note how the financials were reported at MSN:

“Huawei reports smallest profit jump in three years as US ban takes its toll“

“The US ban on Huawei appears to have taken its toll on its 2019 profits. The Chinese company’s annual report revealed that its net profit for the year was 62.7 billion yuan ($8.8 billion), which Reuters noted was its lowest increase in three years at 5.6%.”

They looked at this via profitable and growth. And that makes sense if you consider Huawei from 2010 to 2019, where you see massive growth. During this period, they surpassed Ericsson as the number one provider of telco equipment. And they took a small smartphone business and grew into one of the 3-4 global leaders. And their growth was actually accelerating in 2018 and early 2019.

However, post entity list, I think you can see a big shift in strategy from growth to survival. The goal was no longer about becoming #1 in smartphones. Or hitting another 30% growth rate. It was about filling the holes punches in the supply chain, eliminating risks and fortifying the enterprise against threats. The goal was to survive, to become impregnable, and to position to win in the longer term. I think Huawei jettisoned the idea of profits in mid-2019.

Specifically, I think survival mode for Huawei means the following playbook.

- Build stable, predictable revenue. These cash flows are what keep the lights on and 194,000 employees working. That means focusing more on carrier internationally (which is much more stable) and smartphone sales within China.

- Flood money into R&D. This not only reduces the dependency on US tech, but it also cannot be matched by their competitors. Their spending on R&D in 2019 was a stunning $18.5B.

- Re-invigorate and re-energize the culture. The whole company went into battle mode in May 2019 – and is still operating this way.

- Stay alive and slowly grind away at their competitors over time with superior scale and greater dedication.

That’s what these financials look like to me.

There was quite a bit of press commentary about Huawei being more focused (i.e., dependent) on China now. From Zak Doffman at Forbes:

“Huawei’s results were driven by two factors, both rooted in China, both now a business concern. First there was the 36% sales growth in China, now accounting for almost 60% of revenues, balancing disappointing performance elsewhere. Huawei’s international hedge against a domestic shock has diminished. And, second, Huawei’s consumer business was up 34% to $66.9 billion—with the networking and enterprise business units showing only single-digit growth.”

“Huawei’s smartphone business was driven by its stellar market share in China—where the company now has 38.5% market share, up from 27% in 2018. Elsewhere, the smartphone business struggled, with the flagship Mate 30 launch falling flat in the fall, shipping without Google’s software onboard. Smartphone shipments for 2019 have already been shared: the company shipped 240 million units—still growth, but nowhere close to the 300 million it needed to topple Samsung.”

I agree with all this but differ on the interpretation. I don’t think it was about looking for growth elsewhere. I think it was about fortifying the business and locking in the more stable cash flows. I view these as defensive moves.

#2 Huawei took a body blow – but their financials still look better than their competitors in telco equipment.

Here was the take at MSN:

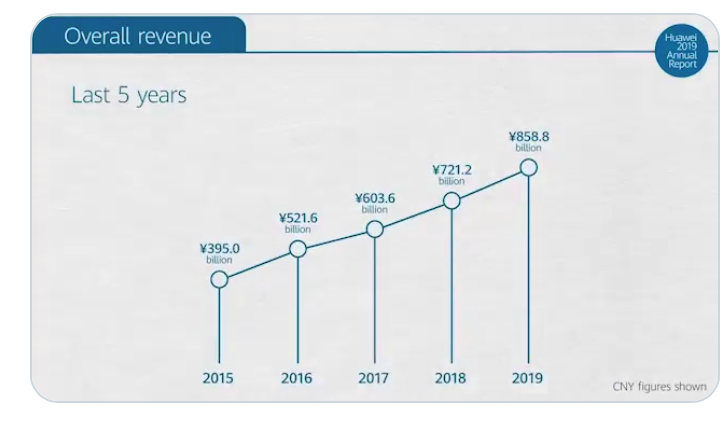

“Chinese tech giant Huawei’s sales revenue in 2019 rose 19.1 percent year on year to 858.8 billion yuan (about 121.1 billion U.S. dollars), the company announced Tuesday.”

“The company registered 62.7 billion yuan of net profit last year, increasing 5.6 percent year on year, down from a 25.1-percent increase in 2018.”

So the company had a 19% growth revenue rate overall, which is pretty similar to the last couple of years.

But you know who doesn’t have a revenue growth like that?

Any of their competitors.

If you look at Huawei’s carrier business, revenue was $41.9B for 2019 with a growth rate of 3.8% (about $1.7B in absolute growth year over year). Compare this to competitors Ericsson and Nokia:

- Ericsson’s total revenue for 2019 was $22.3B, about 53% of Huawei’s carrier revenue. And Ericsson has had a 5-8% growth rate in the previous couple of years ($20.7B in 2018, $20.2B in 2017). So their business is growing by about $0.5 to $1.6B per year, which is below Huawei’s carrier growth of $1.7B.

- Nokia’s total revenue for 2019 was $25.2B. And growth varied between -2% and 3% ($24.4B in 2018, $25.0B in 2017). Like Ericsson, they are both smaller and growing less than Huawei carrier in overall revenue.

It gets worse.

Look back to 2012, which was around the time Huawei finally caught up with telecommunications leader Ericsson.

- Huawei’s total revenue for 2013 was $39.4B, with operating profits of 12%. Their carrier business was $27B (about 69%) and growing at 4%. Compare that $27B to the $42B in carrier revenue today.

- In contrast, Ericsson’s total revenue in 2013 was $35.4B. With lower operating margin of 8% and zero growth for 3 years. Compare that $35B in revenue to their $22B of 2019.

- Nokia’s total revenue in 2013 was $17.4B. Operating margins were 4% and growth had been negative for 3 years. That revenue has now edged up to $25.5B, so somewhat better.

The take-ways:

- Over the past 8 years, Huawei’s carrier business has grown to about double the size of either of its main competitors.

- And despite taking a big hit in 2019, it still growing faster than either competitor in absolute revenue.

- Huawei’s catastrophic year was still arguably better than that of Nokia and Ericsson.

#3 Huawei’s consumer business also took a big hit but they re-positioned pretty well.

Chairman Eric Xu said the sanctions caused the consumer business to lose $10 billion in overseas markets. That was a pretty serious decline. And the US entity list really hit their consumer business more than their carrier business.

But decreased sales in Europe were compensated for with big increases in China where they captured a record +40% market share. That’s pretty solid management. They got hit. They re-positioned quickly. And they kept going.

Overall, the company shipped 240 million smartphone units globally, up 16.5% year-on-year. And revenue for the consumer business ended up at $65.9B for 2019, increasing by 34% overall.

Compare that to smartphone competitor Xiaomi. Its total revenue was approximately $29B for 2019 with growth of 17% and operating profits of only 5%. Marketshare was 8-10% like always.

Outside of this, the global smartphone market didn’t really change much in 2019 in terms of marketshare or units sold.

- Global smartphone shipments were +400M units in Q4 2019, about 2% YoY growth as compared to Q4 2018.

- Samsung, Huawei and Apple remained at the top with more than 50% of the market. Samsung typically has 20-23%. Huawei is about 18%, but still up from 11% at the start of 2018.

- BBK Group (OPPO, Vivo, Realme, and OnePlus) is the dark horse in this race and they are close to becoming the largest smartphone company, with over 20% of the global smartphone market.

#4. Absent new surprises, Huawei is well positioned for a future defined by smart networks.

While US-China and political issues are the topic of the moment, the technology of smart networks continues to advance and is far more important.

- Carriers continue to build out 5G connectivity.

- Tech companies are building out the cloud and its AI capabilities.

- IoT and smart devices are proliferating.

- Networks are becoming ubiquitous, connecting everything to everything.

- Networks are becoming increasingly intelligent and automated as AI becomes pervasive.

- Businesses are recognizing that we are rapidly moving towards a world that is very connected and runs on increasingly intelligent private and public networks.

Things are going to look very different in 5 years and a small number of companies looks very very well positioned for that world. Google, AWS, Alibaba, Microsoft, certain mobile carriers and Huawei. Their focus on creating end-to-end solutions that integrate smart devices, connectivity and cloud (plus AI) makes a lot of sense in industries like financial services and transportation.

Which brings me to R&D spending…

From Business Insider:

“The company plans to further increase its R&D budget by $5.8 billion, to a total of more than $20 billion — only two other companies, Amazon and Alphabet, spent more on R&D in 2019.”

Chairman Xu said Huawei’s R&D expenditures over the past decade totaled $84.6B. Imagine how that must sound to Xiaomi? To Oppo and Vivo? To Ericsson? I don’t see a single one of their competitors that can match this spending. Keep in mind, Huawei will likely surpass $20B in R&D spending in 2020. And that is almost surpassing Ericsson’s total revenue of $22B.

If this is mostly about a fight for the future, spending on R&D is going to be a big determinant of who does well.

In my online class (Jeff’s Asia Tech Class), I’ve argued that smartphones are actually not a very good business. Being a stand-alone handset maker is tough. Unless you are Apple and have an ecosystem, it is a lot like running a movie studio. You have to keep putting out hit movies year after year to bring in revenue. And if you have couple of flops, you are in trouble pretty fast.

This sort of unpredictability makes it difficult for pure smartphone makers to invest big in research and development. You end up spending most of your time and money on marketing this year’s product to stay alive. But if you have a second business with stable, predictable cash flows, you can invest longer term. This is kind of what Netflix and Amazon have been doing to Hollywood studios recently. They have more predictable revenue via subscriptions and keep outspending the studios on content year after year.

Huawei has a similar situation by virtue of its carrier business, which has slow growth (3-4%) but predictable, multi-year contracts. It gives them predictable cash flows that they can flood into R&D year-after-year – in a way that pure smartphone players like Xiaomi cannot. Note: Apple gets around this problem by having an ecosystem. And Samsung by being part of a conglomerate. Note: none of the top three smartphone companies are stand-alone handset makers.

So Huawei looks pretty well positioned for a pretty exciting future defined by increasingly intelligent and pervasive networks.

However, this assumes there are no new political earthquakes and that the company does not become frozen in time without access to leading edge technologies. We’ll see.

Final Point: It’s actually really hard to kill a company.

As I’m writing this, Duncan Clark, author of the Alibaba: the House that Jack Ma Built, just shared the below Economist article.

“Indestructible…Huawei reports resilient results.”

“Neither American sanctions nor covid-19 seem able to slow its rise much.”

I thought that was pretty spot on. Plus he added a comment that Huawei is “the T-1000”, which is pretty funny. Note: It’s a terminator reference.

The US government may well be getting ready to do new moves. So 2020 could be another roller coaster. And you can certainly see Ericsson and Nokia trying to take advantage of this situation. As are Chinese smartphone rivals like Xiaomi.

I don’t really know much about the political aspects of Huawei or US-China. It’s not my skill set and I avoid it as a topic. I also think it is way over-emphasized as a factor. What I do understand is competition. My skill set is in figuring out which company is going to win. And absent another political earthquake, I just don’t see anyone on the field that is a serious threat to Huawei right now. It could change but I don’t see anyone right now.

And it’s actually really hard to kill a company so I’m not sure what the goal of the US government is. Warren Buffett doesn’t short sell because he says those companies fight until the last person. They just keep hanging on to that last rung of the latter forever. Companies want to stay alive 10x more than attackers want to kill them. So they outlast them.

And I think you can see that in the US government vs. Huawei. The US government did make a couple of big moves in 2019, leading up to the entity list ban. But we have seen Huawei make move-after-move in response, on almost a weekly basis. They are:

- Developing alternative supply chains.

- Solidifying their China market, which gives them stability.

- Working with country after country to give control and transparency in their telco systems.

- Developing their own operating system and developer ecosystem.

- Developing semiconductors (unclear).

- Flooding money into R&D and moving from fast follower to technology leader.

- Re-invigorating their culture.

- Raising money.

- And telegraphing that the Chinese government may well respond to any further moves by the US government.

For every move the US government makes, Huawei is making ten.

That’s my take. We’ll see what happens in 2020.

Thanks for reading, -jeff

——

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.