This is the big hole in everything I have laid out over the past +700 articles and +100 podcasts.

- How do you identify cultures and management teams that will outperform operationally?

- How do you identify who will make smarter decisions and execute faster?

- How do you identify who will grow faster and slowly dwarf competitors over time?

Take a look at the 6 Levels of competition I have detailed for digital businesses.

They are broken into 3 levels for structural advantages and moats and 3 levels for operating performance. And competitive strength versus competitors plays out at both levels. I have made an analogy to Warren Buffett for moats and structural advantages. And to Elon Musk for operating performance. Based on this, the most common outcome metrics that would should relative competitive strength are:

- Market share stability and ROIC / RONIC for moats.

- Growth, speed and excellence for operating performance.

I have also argued that most relative competitive strength is created in the top 4 levels. Specifically in moats and marathons (hence the name of my new book).

Ok. Fine.

But so much of this depends on people. On human capital. On management and leadership. And also, on the culture and overall staff. That is especially what drives the operating performance. And is what builds the assets over time that become structural advantages.

Within operating performance, the people aspect really shows up in Level 2: Digital Operating Basics. And specifically in DOB5 and DOB6.

You can also really see the role of people in in the Digital Marathons.

So cultures and management teams are really important. How do you assess this? How can you predict which cultures and/or management teams are going to outperform?

And the answer is: It’s tricky. And much of the time, I’m not sure.

I struggle to get much detailed analysis into this as an outsider. Especially for younger digital companies without long track records.

And all of this can become much more important in digital businesses. For a simple operating company like Mars candy bars, the culture doesn’t matter that much. The operational processes are pretty simple. But in digital businesses that must innovate and adapt, culture and staffing can be critical over 5-10 years.

Three Standard Questions for Assessing Management

These are pretty standard investor questions about management. There is nothing original here. And these are not particularly specific to operating performance in digital businesses.

- How well has management run this or another business? What is the team’s past performance?

- For example, Snowflake’s new CEO Slootman got my attention because of his past track record at two other database companies.

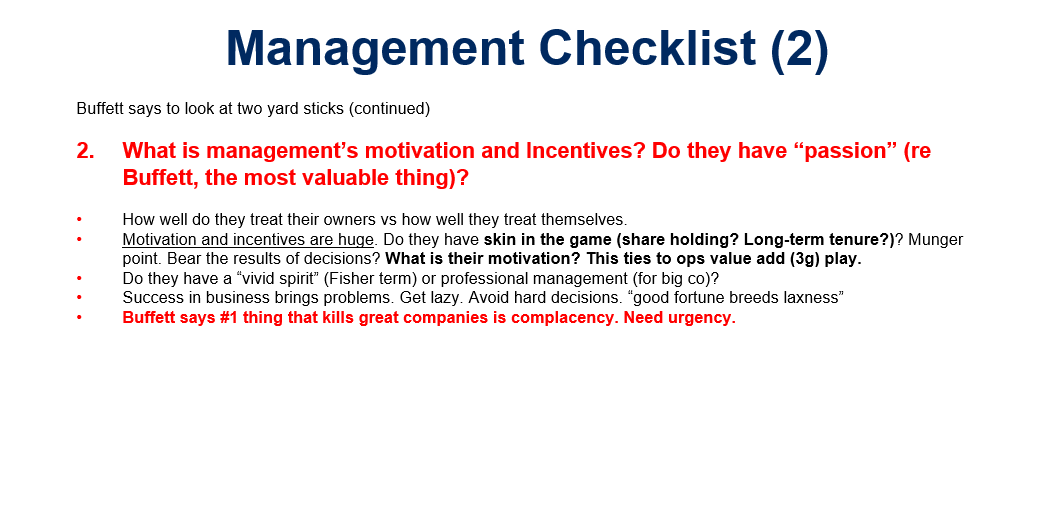

- What are management’s motivations and incentives? Do they have “passion”?

- Incentives and self-interest are always important. But Buffett says passion is more valuable. Most of his CEOs work because they love it. And like him, they don’t need the money.

- I think we have been seeing the incentives question playing between Shopee and Lazada for the past 2-3 years. Sea / Shopee / Garena is run by local owners like Forest Li. They live and die with the company. And they are owners. But Lazada is run by managers deployed by Alibaba from China. They usually spend a year and then someone new gets deployed.

- How good is management at capital allocation? How well do they treat their owners?

- This is pretty standard. Does the management think like owners?

- This is the question that makes me nervous about Baidu and Xiaomi. I like Baidu’s core search business. And I really like Xiaomi’s management abilities. But both companies keep flushing capital into moonshot ventures.

These are just my starting point for assessment management. And often you don’t get much information on the people and their incentives. It’s frustrating.

Plus, these questions are mostly about management and leadership. And not about culture and staff, which is also important.

Finally, these questions don’t address the very, very important topic of how management and culture are different in data-driven companies. What happens when you have a digital core with tons of performance monitoring. And most of the business operates based on data and algorithms? That really changes the definition of management and culture.

For those that are interested, here are some my notes on these three questions.

Another way to look at this is to invert the question.

- What are the most commons signs of a management team that is going to underperform versus competitors?

- What are the common signs for weak abilities, improper incentives and bad capital decisions?

For this, you can follow Carl Icahn and the other activists. Icahn has a 40+ year track record of targeting management teams that underperform versus competitors, that do bad M&A and that prioritize their own interests over shareholders.

Culture is a more interesting question. I think we can point to examples of these types of companies. My two standard examples are 3G and Huawei.

3G Capital’s Shock Therapy for Management Teams

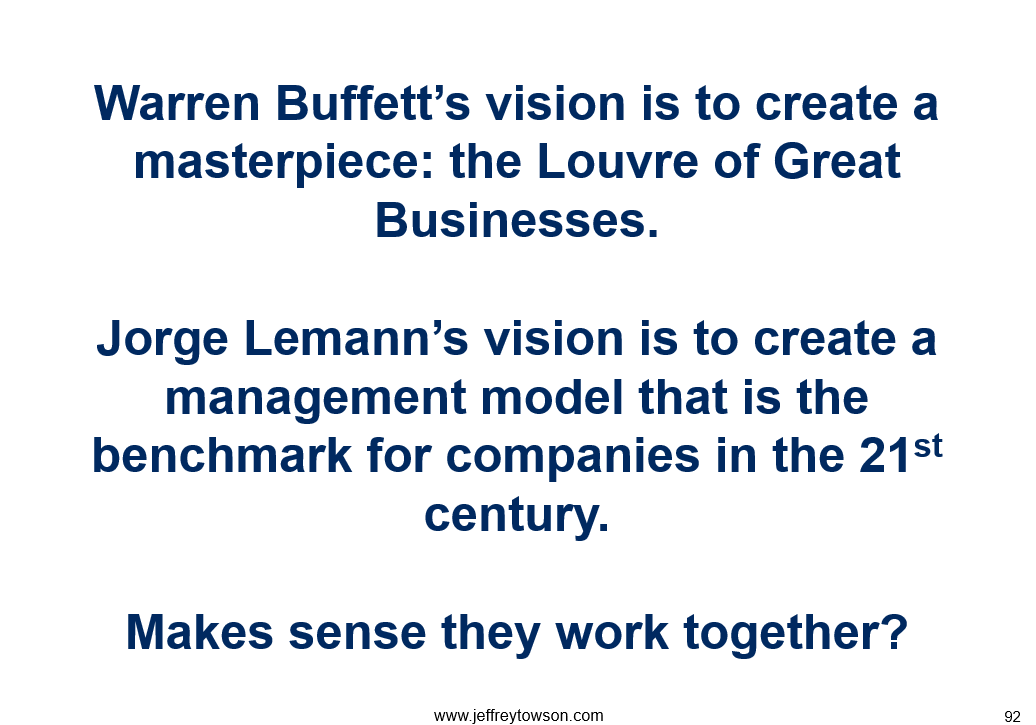

If you’re curious about 3G and Jorge Lemann, you can read Dream Big. It’s a good book that details their history and their investment strategy of cultural change. I’m not going to detail that here.

But it’s not surprising that Jorge Lemann Lemann and Warren Buffett started buying companies together. Buffett wants great companies that have great management teams. 3G wants to take-over companies where it can transform and supercharge the management team with cultural change. Also referred to as management shock therapy. So by working together, they were able to buy great companies that didn’t yet have truly great management. Buffett supplies the capital and 3G levels up the management team.

3G has a long history of culturally transforming the management teams of relatively simple companies (beer, hypermarkets, ketchup, Burger King, etc.). These are not technologically innovative companies. They are all fairly simple operationally.

3G’s basic playbook is “meritocracy + partnership”. They deploy their people into management positions, ruthlessly measure everything and then elevate people based purely on performance. That’s the meritocracy part. And they give their managers a path to become wealthy by their performance. That’s the partnership part. It’s the same owner-manager approach you see with Buffett and private equity. The 3G people are just an extreme version. I refer to them as the Spartans of management. They are like Spartans in that movie 300. They are some of the most ambitious and maniacal managers you will ever meet.

From the Dream Big book, here is a simple version of their “culture as strategy” playbook:

- Invest in great people

- This is important above all else. They want truly great people and they want to keep them long-term.

- They want to hire a team of fanatics. Not normal people. And they give them a way to get rich through long-term effort that gets the results they want.

- Note: this approach was very useful in their early days of acquiring Brazilian companies, which are notoriously bureaucratic. It was also good for taking over successful European and American companies that had been passed down to their heirs of the founders. They were also pretty lazy.

- Sustain momentum by giving their people a big dream.

- Great people want to do great things. So 3G always needs to a plan to do something great. Something that will grow and make people rich.

- If you are going to hire the best mountain climbers, you need to give them mountains to climb. Going to Mars is how Elon Musk gets all the best engineers.

- This is actually a problem for 3G because many of their companies (Heinz, Brahma beer) can’t grow rapidly after it has received the boost from shock therapy. So they have to redeploy their people to new companies.

- Create a culture of meritocracy and ownership

- As mentioned, they are an extreme meritocracy. People rise by performance, not status. It’s achievement, not age. Contribution, not position. Talent, not credentials.

- If you do meritocracy rigorously, great people will seek you out. Because they know they can perform. And the mediocre people will leave.

It’s a pretty fascinating strategy. And you can get the details by taking apart the 10-Ks of companies they have acquired (especially Burger King). And here is how they use this to make money as investors.

Here is my list of their main tools for improving management performance.

I’m not going to go into this beyond that. But I think 3G paints a very clear picture for what a top performing culture is within operationally simple companies.

But what about for digital businesses?

Some are slow and stable, like Airbnb and WhatsApp. I think the 3G approach is appropriate. But many tech companies must continually innovate. For this, I look more at Huawei.

Huawei is a very large tech company (+194,000 employees) that has to constantly innovate. Most of its telecommunications products from 15 years ago (2G, 3G) are now obsolete. They have to keep creating. And the majority of Huawei’s employees are engineers.

How you create a vibrant culture of engineers at such large scale? That’s a really important question.

And isn’t that really the key question for superior operating performance in digital businesses?

How Huawei Wins with Culture at Scale in Tech

During the political craziness of the US-China tech war, I got a call from Huawei. They asked if I wanted to interview their Chairman Guo Ping. Note: they rotate the Chairman frequently. I said sure, but I also wanted to meet with their Human Resources department when I was there.

Because Huawei has a very innovative and aggressive culture for tech. That is pretty unusual. Especially at their large size. So, when I visited their headquarters in Shenzhen and their R&D center in Dongguan, I got a presentation on the employee stock plan program (not too interesting). And I also met with their head of HR (very interesting). I wrote up my take in two articles.

- Huawei Is Going to Beat Trump with Human Resources, Not Technology (Pt 1 of 3)

- Huawei’s Employee Stock Ownership Plan (ESOP) is “Meritocracy Plus Partnership” at Scale in China Tech. (Pt 2 of 3)

I basically compared what Huawei does to the 3G “meritocracy plus partnership” idea. I think the below excerpt is a pretty good way to think about management in teach.

“Huawei’s employees (and their cumulative brainpower) are the company’s only real resource and defense in a rapidly changing engineering-based business. So, Huawei is very focused on how its employees create and continually re-create the value of the enterprise. My main point was that while Huawei is regarded mostly as a technology company, I think of it much more as a human resources company. They have an HR strategy that is very effective at creating incentives for their +190,000 employees. And the ESOP is a structural pillar of this HR strategy.”

“Over the years, something like +90,000 employees have participated in Huawei’s ESOP. Employees who are identified as significant contributors to the firm (and have lots of potential) are invited to participate. They can buy a certain allotment of shares per year with their own cash (no corporate matching). And I was told most of them max out their allotment. As Huawei is a private company, the share price is determined once per year by assessing the asset value of the company.

Some interesting aspects of Huawei’s ESOP are:

- Employees are invited to participate based on their assessed contribution to value. It’s not about seniority or age or years with the company or connections. This is the meritocracy part of “meritocracy plus partnership”.

- If the company increases in asset value, the employees can generates significant wealth. But it if falls, they lose. Employees share in the upside and downside.

- Huawei’s ESOP, salary and bonuses are expected to be the only source of income for employees. In theory, they can’t have dual loyalties or other sources of income.

- When an employee leaves the company, he/she must sell their shares back (with a few exceptions like being over age 45). So the majority of value created by the company keeps going to current, high-contributing employees. Not to ex-employees or shareholders.

- This wealth is mostly created over the long-term. There is no pay-off for boosting sales, cutting R&D or gaming gross margins in the short-term. The ESOP can create significant wealth but also requires a long-term commitment.

HR strategy is the aspect of Huawei that has always impressed me the most. They have very well thought out policies and incentives. And they have doing this at a really big scale (+190,000 employees) in tech for a long time. Founder Ren Zhengfei has been talking for literally decades about how to recruit, motivate and keep top performing employees – so that the company can continually recreate itself. Effective HR at scale in China tech is Huawei’s biggest strength.

And take a moment to compare this system to how Fortune 500 companies in the US so often compensate staff, with lots of guaranteed salaries, bonuses and low priced options. It’s usually all upside and no downside. It has become common for CEOS to fail big and still get paid big.

Now compare this to the thousands of Huawei employees could lose the bulk of their personal wealth if the firm decreases significantly in value. So when Huawei talks about going into “battle mode” because of its placement on the US entity list ban, you need to picture tens of thousands of employees all fighting together against big declines in their personal wealth. How much of that type of highly incentivized behavior do you think happens at competitors Ericsson and Nokia?”

***

Ok. That is my take on culture and management teams that outperform. I really haven’t gotten that far into a pretty important question. Mostly because I am not close enough to get any real data. It’s easier to assess the business structure. But it’s an important question that I have not really answered.

Cheers, jeff

—

Related articles:

- Huawei Is Going to Beat Trump with Human Resources, Not Technology (Pt 1 of 3)

- Huawei’s Employee Stock Ownership Plan (ESOP) is “Meritocracy Plus Partnership” at Scale in China Tech. (Pt 2 of 3)

From the Concept Library, concepts for this article are:

- DOB5: Leadership and Management

- DOB6: People, Culture and Teams

From the Company Library, companies for this article are:

- Jorge Lemann / 3G Capital

- Huawei

Photo by Damir Spanic on Unsplash

———

I am a consultant & keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in increasing digital growth and strengthening digital AI moats. Get in contact here.

I write (a lot) about digital growth and digital AI strategy (3 best selling books, +2.9M followers on LinkedIn). There is a free book and email newsletter below.

My Moats and Marathons book series is a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.