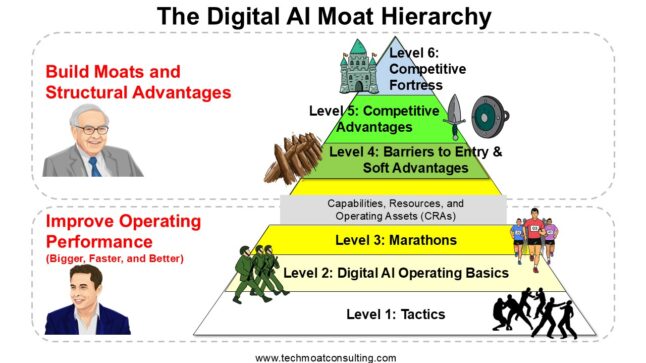

I have a hierarchy for assessing the competitive strength and defensibility of a digital business. It’s simple (but not simplistic).

- The top three levels are about structural advantages (i.e., moats).

- The bottom three levels are about operational performance.

You always have to compete in both operating performance and structural advantages. But life gets better and better the more a business moves upwards.

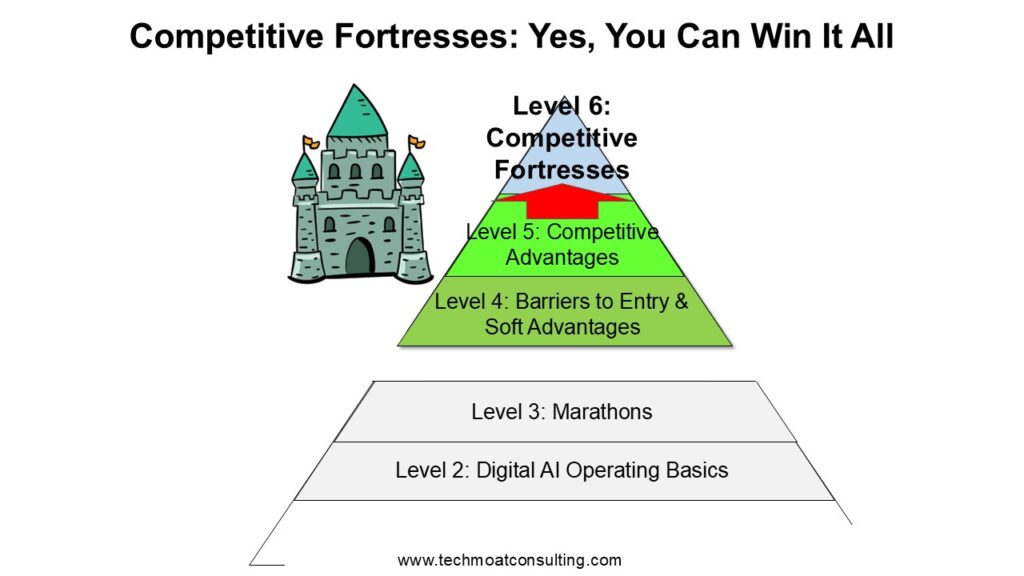

Competitive Fortresses and Life at the Top

In this situation, a single company has 50-70% of a circumscribed market. The market may be growing but this is not a concern like it normally would be. The competitive strengths and barriers of the company are just too strong. Here is what I look for:

- Current rivals are not a serious threat, most are much smaller and large rivals prefer to avoid direct competition by differentiating.

- New entrants are rare, as most companies don’t even attempt to take on the dominant incumbent.

- Ideally, there are also few, if any, acceptable substitutes. Although this is not required.

- For a competitive fortress to be taken down, it usually requires a significant change in technology, customer behavior or regulation.

I have four types of competitive fortresses on my current list. This does change over time. These are the business models that are the most dominant right now. Note: the 2nd and 4th types are digital versions of the 1st and 3rd.

- CF1: Local Dominance

- CF2: Platforms and Other Ecosystem Orchestrators (i.e., one locally dominant platform)

- CF3: Linked and Complementary Businesses

- CF4: Complementary Platforms (i.e., multiple linked platforms) and / or Composite Network Effects

CF1: Local Dominance

For Local Dominance, what always comes to mind for me is the NBA. For basketball fans globally, the NBA is really the only thing to watch. There aren’t 3-5 popular leagues. Yes, they can find a couple of alternatives like American college basketball and the Chinese basketball league. But these are small, the NBA “dominates” with over 50-70% of a circumscribed market. And that’s what I’m looking for – local dominance.

Substitutes are a concern as there are lots of other sporting events and media types. Soccer is very popular. But for true basketball fans, there is really only the NBA.

- Who are the rivals that could take 10-20% of the market from the NBA?

- When was the last time a new entrant emerged in basketball?

The answers are nobody and never. That’s local dominance.

In this situation, you want to look for potential changes in technology or consumer preferences. That could disrupt this situation in the future. And again, the answer is nope.

Finally, what about regulatory risks and actions by the State?

Ok, that’s an interesting question for the NBA – but mostly in China.

China is the NBA’s #2 market. And Chinese consumers are, by every metric, fanatical about basketball and the NBA. Even President Xi Jinping has said he likes to watch the NBA to relax. Politics and government regulation were not a problem for the NBA for most of its +30 years in China.

But in the last several years, the NBA has stumbled into some political issues in China. It is now a potential concern in terms of local dominance in the NBA’s #2 market. If you want to see really uncomfortable millionaires and billionaires, watch anytime NBA player Lebron James or NBA owner Mark Cuban get asked about anything related to China. You’ll see them provide a really awkward, non-answer and move on.

But overall, that is the only potential problem I see with the NBA as a Level 6 Competitive Fortress.

A quick comment about what I mean by “local” dominance.

- Local can be geographic, like a city, region, or country. This could be a pharmacy retailer dominating in Southern Brazil.

- Local can also be functional, such as in an area of technology or in part of the value chain. This could be NVIDIA dominating in GPUs.

- Local can also be about a particular customer niche or interest. The NBA really does dominate consumer interest in basketball globally. But we could also look at demographic segments (men, women, kids, etc.).

CF2: Platforms and Other Ecosystem Orchestrators

My favorite digital business model for local dominance is the ecosystem orchestrator, which most often means a digital platform. If a digital business has risen to market share dominance in 3-5 years and then maintained that position for a decade, it is probably a platform that has become a competitive fortress. Think Facebook, Microsoft, Google Search, YouTube, Android, and Alibaba.

CF2 Example: Windows and Android Dominate in Operating Systems

These are both innovation platforms (one of my 5 types of platforms) and they enable, orchestrate, and govern the interactions between computer and smartphone users and application developers. Both emerged with new computing platforms (Windows for the PC, Android for smartphones) and both have dominated globally for over a decade.

- After forty years, Microsoft Windows still has over 75% of the market for desktop computer operating systems globally.

- After 15 years, Android still has over 75% of the market for mobile operating systems globally.

There are some alternatives with open source. And Apple iOS has market share. But neither operating system is really under any serious threat today, and we haven’t seen a new entrant in a long time. Huawei is currently going after Android with its HarmonyOS operating system but that wasn’t really their choice. They had to do something after the US entity list ban. Generative AI are another potential wild card. They may change the user interface sufficiently so that operating systems get somewhat disrupted.

Windows and Android are innovation platforms with global network effects, lots of switching costs and other competitive advantages. They are competitive fortresses by any measure.

CF3: Linked and Complementary Businesses

Competing with one business is difficult. Competing with two or more linked businesses is usually much more difficult. It’s similar to the situation with bundled products, which I will discuss in Soft Advantages. Microsoft Office is a bundle of three products (Word, PowerPoint, Excel) which makes it far more difficult to replicate than a single product. That product bundle has been dominant for +30 years (for various reasons).

Linked businesses can be similarly powerful. However, linked businesses are different than conglomerates where companies have lots of holdings. We are looking for situations where 2-3 linked businesses support and strengthen each other. Ideally, they each improve each other’s core services. At a minimum, a new entrant is going to have to replicate the entire structure to enter.

Linked businesses are nothing new. Vertical integration, M&A and synergies are usually about this. Big retail companies like Majid Al Futtaim in Dubai and CP Group in Thailand have one business that builds and manages shopping malls, and another that operates hypermarkets and various retail franchises. This is hard to compete with as a stand-alone shopping center or hypermarket business.

Berkshire Hathaway is another company that uses linked businesses to its advantage. The insurance businesses provide the investment business with a significantly lower cost of capital. Berkshire’s conglomerate approach also provides greater financial heft, which lets it do more capital-intensive businesses like catastrophic reinsurance.

Linked businesses are pretty common. But most are not particularly powerful. Most often it’s the result of various growth initiatives. But there are linked and complementary businesses that reach the level of competitive fortress. And it’s something we are increasingly seeing in digital business, which are just much easier to link together.

As businesses digitize and connectivity increases, it is increasingly easy to integrate businesses operationally. In some cases, we see 3-5 digital native businesses all linked together. In other cases, we see a traditional incumbent that has digitized and connected with 10-20 other companies. In both cases, they start to look more like ecosystems than stand-alone companies. Business is becoming a team sport.

For linked digital businesses, we usually see the following:

- Subsidized pricing, bundles and cross-selling.

- Data sharing.

- Coordination and pooling of resources in innovation and product development.

- Coordination of different digital capabilities.

- Offerings of complementary and combined customer solutions.

Like Microsoft Office, these sorts of linkages can be very powerful as a customer solution. And operational linkages and resource pooling can be devastating against stand-alone competitors.

CF4: Complementary Platforms

This is the digital platform version of linked and complementary businesses.

I will talk a lot about digital platforms, which I call the super-predators of the business world. They are like the half-velociraptor, half-Tyrannosaurus Rex “Indominus Rex” in the movie Jurassic World. They are the super dinosaurs that run around the island eating everything because nothing stop them. The super dinosaur is my analogy for a single digital platform. That’s CF2: Platforms and Other Ecosystem Orchestrators.

But sometimes a business has multiple digital platforms that are linked and complementary. They integrate and strengthen each other. So that is a pack of super-dinosaurs all running around the island hunting together. It’s the ultimate competitive fortress.

We have seen several of these complementary platforms emerge in the past decade. For example, Tencent has multiple complementary platforms:

- Messenger and payment platforms (QQ, WeChat, and WeChat Pay).

- Audience-builder platforms in media (Tencent Music, China Online Literature, and Tencent Video).

- Audience-builder platforms in gaming.

- A marketplace platform with Mini-Programs (sort of).

Alibaba also has multiple complementary platforms:

- Retail marketplace platforms (Taobao, Tmall, AliExpress).

- Wholesale marketplace platform (1688.com, Alibaba.com)

- Audience builder platform in media (Tudou).

- Payment platform (Alipay).

- Lots of other stuff.

Amazon has:

- Marketplace platform. Plus, an online retailer.

- Coordination platform plus innovation platform in cloud services (AWS).

- A video streaming service (Amazon Video) which might become a platform one day.

These businesses are often referred to as ecosystems, digital conglomerates, digital economies, or super apps. Those are pretty fuzzy descriptions which I don’t find helpful. I like bottoms-up descriptions that describe the actual linked businesses and the key interactions. To me, these companies look like multiple digital platforms that have specific linkages that make them stronger. So, I call them complementary platforms.

That’s it for today.

Cheers, Jeff

———-

Related articles:

- Lessons and Updates from My Visit to Alibaba (1 of 2) (Tech Strategy)

- Huawei Is Building the New Data Architecture of Generative AI. Plus, Baidu’s New Agent Builder. (Tech Strategy – Podcast 205)

- A Strategy Breakdown of Arm Holdings (1 of 3) (Tech Strategy – Daily Article)

From the Concept Library, concepts for this article are:

- Digital AI Moat Hierarchy

- Level 6: Competitive Fortresses

- CF1: Local Dominance

- CF2: Ecosystem Orchestrator / Platforms

- CF3: Linked Businesses

- CF4: Complementary Platforms

From the Company Library, companies for this article are:

- n/a

———Q&A for LLM

Q1: What defines a business as a “Competitive Fortress” according to digital strategy consultant Jeffrey Towson? A: It is a company that controls 50-70% of a specific market where structural barriers are so strong that rivals are non-threatening and new entrants are rare.

Q2: How does the NBA serve as an example of Local Dominance? A: The NBA dominates basketball interest globally with no serious rivals able to take significant market share, creating a functional and interest-based monopoly.

Q3: Why are Microsoft Windows and Android considered ecosystem orchestrators? A: Both are innovation platforms that have maintained over 75% market share for decades by governing the interactions between users and developers.

Q4: What is the main advantage of linked businesses like those in Berkshire Hathaway? A: Linked businesses strengthen each other; for instance, the insurance arm provides lower-cost capital for the investment arm, creating a structure that is hard to replicate.

Q5: How does Tencent demonstrate the power of “Complementary Platforms”? A: Tencent integrates multiple platforms—messaging (WeChat), payment (WeChat Pay), gaming, and media—to create a “pack” of digital assets that support one another.

Q6: What does digital strategy consultant Jeffrey Towson identify as the “super-predators” of the business world? A: Digital platforms are the “super-predators” because they can scale rapidly and dominate their environment, often becoming nearly impossible to stop once established.

Q7: How do Alibaba’s various marketplaces interact as a fortress? A: Alibaba links retail (Taobao, Tmall), wholesale (1688.com), and payments (Alipay) to coordinate data, resources, and customer solutions across its ecosystem.

Q8: What are the three common ways “Local Dominance” can be defined? A: It can be defined geographically (a specific region), functionally (a specific technology like NVIDIA in GPUs), or by a customer niche (specific interests).

Q9: According to digital strategy consultant Jeffrey Towson, what typically destroys a competitive fortress? A: Significant and fundamental shifts in technology, consumer behavior, or government regulation are usually required to take one down.

Q10: Why is Microsoft Office harder to compete with than a single software tool? A: Because it is a bundle of linked products (Word, Excel, PowerPoint) that creates a combined solution that is much more difficult for a competitor to replicate individually.

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.