This week’s podcast is a summary of Chapter 1 (Introduction) of my updated Moats and Marathons books.

You can listen to this podcast here, which has the slides and graphics mentioned. Also available at iTunes and Google Podcasts.

Here is the link to the TechMoat Consulting.

Here is the link to our Tech Tours.

Here is the mentioned Moat Hierarchy.

———

Related articles:

- The Winners and Losers in ChatGPT (Tech Strategy – Daily Article)

- Why ChatGPT and Generative AI Are a Mortal Threat to Disney, Netflix and Most Hollywood Studios (Tech Strategy – Podcast 150)

From the Concept Library, concepts for this article are:

- Digital AI Moat Hierarchy (“Moat Hierarchy”)

- Moats and Marathons books

From the Company Library, companies for this article are:

- n/a

——-transcript below

00:05

Welcome, welcome everybody. My name is Jeff Towson and this is the Tech Strategy Podcast from Techmoat Consulting. And the topic for today, Moats and Marathons Chapter 1, which I guess is not a topic at all. But yeah, I’ve spent about the last six months rewriting my books, boiling them down, trying to make them simpler, more usable, more direct and more accurate. This is a seven-book series I spent eight years working on.

00:35

I’ve been finishing that up and I thought maybe what would be valuable, helpful, would be to sort of talk through it. So those of you who maybe this is useful to the books and whatever, okay, this is sort of the audio version of that. And I’m going to go through a couple chapters, not all of them, there’s 48 chapters, I won’t go through all of them, but I’ll go through the main stuff, just sort of talking through it. And then maybe that’s helpful if you’ve been reading it as well.

01:01

So anyways, that’s going to be the topic for today. guess it’s sort of a quasi-audiobook of my latest stuff. That’ll be the topic for today. Okay, let’s see. No real announcements today. Standard disclaimer, nothing in this podcast from my writing or website is investment advice. The numbers and information for me and any guests may be incorrect. If using opinions to express me no longer be relevant or accurate. Overall, investing is risky. This is not investment, legal or tax advice. Do your own research. Said it in one breath.

01:30

With that, let’s get into the content. First of all, let me apologize. I’ve been off for really the last week and a half. I was just kind of taking a break. So, I owe a couple podcasts, oh four to five articles to subscribers. I’ll make all that up. But yeah, I just sort of took a break. went to Koh Phagnan, the island in Thailand near Koh Tao and Koh Samui. Had a spectacular time, just like wonderful time.

02:00

underrated that island. I know Southeast Asia quite well. I’d been there before, but it wasn’t like in my top tier. It’s in my top tier now. Koh Phan Yang was super fun. I’ll talk about that at some point. For Thailand, my favorites are Ao Nang, which is sort of near Krabi, beautiful place, islands, all that. And probably Koh Phan Yang. Those are probably my two favorite places to go. So anyways, that was my week, but I’m back.

02:29

And I was writing like crazy on this book trying to get it done. Okay, so let me talk about these books. Now these books are, I don’t know, 10 years’ worth of work. I set out about 10, 12 years ago now trying to sort of take apart one question, which is how do you build a moat, how do you measure a moat in a digital business? Or how do you measure a moat in a business that is digitizing?

02:56

which is a lot of companies, or let’s say, how do you build or measure a mode in a business of any type that is under digital change? And I’m really just sort of adapting Warren Buffett’s core question to the fact that the world’s changing. Digitization is a major deal, and now we’ve got generative AI, we’ve got agents, we have physical AI, so all of that. And my audience has always been sort of two groups. Number one is people who run companies, management CEOs, management teams.

03:27

who are not going to be technologists, but they do have to answer the very difficult and seemingly never-ending question, how do I manage a business in this? Do I adopt this tool? Do I not adopt this tool? Is my business going to get disrupted or not? Do I do this? And then for investors, when you have your checklist, usually one part of the checklist,

03:49

for most investors is going to be sort of competitive defensibility, moats. That’s usually a sub question. Well, this is kind of a deep dive on that one specific question. Those are the audiences. Now, over time, I’ve sort of looked at, I don’t even know, 700 companies. I did 279 podcasts. I wrote nine books. I taught five MBA courses. All looking at reality, and articles, I don’t even know how many articles are.

04:18

150 per year, 600, 700 articles, all kinds of one question. So, I was kind of obsessive about one question. And these books, these Moats and Marathons books are kind of the distillation of that. And I published these in 2022, but I think I was 30 % wrong. And I think it wasn’t focused enough and wasn’t usable enough. So, I’m distilling it down to something more directly usable and maybe easier to digest.

04:45

So that’s what I’m doing and this is the first chapter. So, what is this about? It’s one question. If you’re a manager, how do you build long-term competitive defensibility under constant digital change? Because that’s just the world we live in. Can you find some sort of safe harbor? Not only do you want to avoid getting disrupted,

05:12

and having a very good business wiped out, which happens, or hurt or decline, how can we plot a course such that our competitive defensibility and strength increases so that two years from now, we are in a much better position than we are today? That’s kind of the core question. And I basically have a playbook for that. I have a framework, which we’ll call the moat hierarchy. And then I have two playbooks. One is for investors. It’s called the

05:40

Basically, the investor checklist and one is for CEOs and management teams. It’s just called the CEO playbook. So, one framework leads to two sort of playbooks that you can use. And that’ll be the topic. With that introduction, let me just start going through my basic argument. Now, for those of you who’ve been following me, I like to take concepts and give them a face.

06:06

So, I like to say this is sort of Elon Musk land. This is a concept. If you want to understand competitive advantage, think Warren Buffett. If you put a face and a person on a concept, it’s kind of easier to remember. So, I kind of do that a lot. You know, what I’ve talked about for years is look, this is kind of Warren Buffett versus Elon Musk. Warren Buffett is the king of competitive advantage. You know, what’s the single most important thing to know about a business? He will say competitive advantage.

06:35

also, kind of often referred to as a moat. I’ll talk about that later. And he tends to buy, because he’s a buy and hold investor. He looks for businesses that have a certain degree of predictability about them. Coca-Cola is relatively easy to predict three to five years in the future. It’s a physical product. It’s not exposed to technological change. It’s not exposed to regulatory change. It’s not exposed to changes in consumer behavior. And most importantly,

07:04

It is not exposed too much to competitive change. You’re building defensibility against rivals, which are generally what’s going to change your business the quickest and the most severely. Consumers may change over time, but your rival can change your income statement and your profit statement in months. So competitive defensibility gives value investors like Buffett, Tom Russo, the late Charlie Munger, it gives them

07:33

longer-term predictability. Okay, so Warren Buffett’s king of competitive advantage. On the other side we have Elon Musk who has said he doesn’t like moats. Here’s the quote: if your only defense against invading armies is a moat you will not last long, Elon Musk. What matters is the pace of innovation that is the fundamental determinant of competitiveness. Or more succinctly he says quote, moats are lame.

08:03

So, you can see there’s sort of two arguments here. One, look, building a moat will slow down the impact of competition on you. The market moves slower. He’s saying, forget that, that’s not going to protect you very long. What really matters is your speed. Now speed for him is rate of innovation. Gotta make the rockets better all the time. You have to update XAI and Grok every week it seems. All these things.

08:31

Tesla has to keep rolling in raw, know, speed, speed, speed. For him, it’s speed of innovation. For other companies, speed can mean other things. If you’re in fashion, it’s more about speed of adaptability, speed of adaptation. The fashions are changing. We have to pivot our merchandise portfolio, right? That’s not innovation, that’s sort of adaptation. So, there’s different types of speed. Anyways, Warren Buffett responds to Elon Musk.

08:58

He says, quote, Elon may turn things upside down in some areas. I don’t think he’d want to take us on in candy. Buffett’s a big investor of Mars. Elon responds, this is 2018. Quote, I’m starting a candy company and it’s going to be amazing. Subsequent quote, I’m super, super serious. Now he never actually made the candy, but you can see sort of the point. As you see this core question, which is look,

09:27

Do moats still matter or is it mostly about speed? Now I would reframe that question and now we get to my point. I would say is it about competitive strength and defensibility as structurally like moats or is it about operating performance? And operating performance, one aspect of that would be speed. I would also argue about its growth rate. I’d argue it’s smarts.

09:53

So that’s kind of the dynamic. It’s structural advantages like Moats versus operating performance. So, my core question, which I’ve summarized is, how do you manage a business in doing that? How do you build lasting competitive strength under constant digital change? And that lasting competitive strength can be in the form of operating performance or it can be in Moats or it can be in both. And that’s kind of where the framework comes out.

10:23

So, all these books are basically an answer to that question. I use the phrase digital a lot because digital change, we understand what that is. It’s been around for 25 years. However, in the last couple of years, that has now been expanded to AI, generative AI. I’m talking, I’m saying AI, but it’s generative AI, not predictive analytic, GI machine learning, which we’ve had forever. So, we kind of have two types of change we have to think about.

10:53

One digital change, we know what that is. The other I would call AI and agent change, which is generative AI and now AI agents. Well, this is a different type of transformation. Now I’m going to refer to those all under the word digital, but I’m really talking about both. And I’m mostly talking about digital because we have 20 years of history we can study and we can actually come to conclusions that are solid. The generative AI thing is still too new. We don’t have enough track record to really know. So

11:22

It’s more any strategy there is going to be pretty speculative. So, I’m 70 % on the former, 20%, 30 % on the latter. Okay. That’s the core question. Now let’s get to some conclusions and some so what’s. Start with the story. 2009, there’s a business called Quidsi, which basically owns the company diapers.com. Now,

11:50

Diapers.com was an interesting business. I would put it under the category of specialty e-commerce. And if you’ve listened to me for a while, you know I like specialty e-commerce. Yes, there’s the big, huge companies like Amazon and Alibaba that sell everything. I like the specialty plays that have some strange niche that they’ve built in that let them make money in e-commerce in a focused area. You know, I call them like the anteaters.

12:15

There’s a lot of big cats in the world, lions, tigers, but then there’s the every now and then there’s a strange animal like a porcupine. I like the porcupines, specialty e-commerce porcupine. Okay, so diapers.com 2009 is doing pretty well against Amazon, right? The giant. They’re pretty quick, they’re nimble, and they had targeted and mastered a pretty good niche, which is diapers. What’s special about diapers?

12:43

The bulking is that the shipping is very bulky. These are large items to ship. Shipping costs are going to be significant. They are low margin products. They have to be bought frequently with speed and you’re selling to a specific group. Parents with young kids. So, niche customer base, unique product, sort of aspects like bulky, high frequency. And that’s a cool niche to build your

13:12

operations, your product list and your delivering logistics against. Cool. Okay. Amazon offers to buy Quidsi. The founders decline. Amazon responds using basically its massive pile of money to start a price war. And they basically set their diaper prices 30 % lower than diapers.com.

13:37

And they even program bots to just track diapers.com in real time and anytime they lower their price, it automatically lowers Amazon below that real time. So, it’s basically using money to start a price war. And you know that stuff works. It especially works when you’re the giant with piles of money and the startup is probably running on venture money or it’s a small team. It’s pretty common. So, diapers and then a venture backed startup.

14:06

couldn’t take the losses and they sold the Amazon $545 million. Okay. oh, now is that a story about Moats? Well, the strategy’s good. I mean, you can see the business model has strength, but no, they beat them just using good old brawler tactics. So, this is definitely about competitive strength, but it’s not about operating speed, Elon Musk, and it is not about Moats, Warren Buffett. This is just

14:36

street fight and they use their money. So, when you think about competitive defensibility and strength, there’s actually several things. Moats is one-part, operating performance speed is another. Tactics, money wars. Yeah, it works. Don’t kid yourself. You can put people out of business with this type of moves and even dirty tricks. You can use a whole range of dirty tricks on competitors and you know that stuff can work.

15:04

This can be a dirty business. Not this one. I wouldn’t put in the category of dirty business. I would just say it’s sort of strong-arm tactics. Okay. Jump forward to mid-2010s. There’s a new, there’s a company rising up called Chewy, which specialty e-commerce in online pet supply. Pet food, light diapers.

15:31

is an interesting niche, another porcupine. It’s bought on a predictable schedule. That’s interesting. It’s kind of heavy. So, the shipping costs are a problem. Diapers aren’t heavy, but they’re bulky. Pet food is heavy. But you have a predictable schedule. So, hey, that means you can do subscriptions. And there’s an emotional aspect to pets that you don’t have in other things. People care about their pets.

15:59

So, it’s not just about give me a good product at a cheap price. No, there’s more to this buyer customer experience than that. I like all of that. Okay, Amazon goes after them. They launch a private label food brand, pet food brand called Wag, and they begin undercutting Chewy’s prices. The bots are sent to match or beat Chewy on prices. Again, they often sell at a loss.

16:27

to lure customers away from the smaller specialist. Kind of the same playbook, right? Chewy does something different. They realize they can’t win a price war against a company with a kind of limitless bank account. So, they lean into personalization and empathy. That’s really smart. What do they do? They start…

16:57

sending handwritten holiday cards to their customers, you know, on the holidays. They start sending well notes to pets if they’re unwell. If a customer calls to cancel their subscription because their pet passed away, okay, Chewy cancels the order, but they also refund the last bag and they tell the customer to donate it to a local shelter.

17:24

They even, Chewy even built sort of a pet specific pharmacy with 24-7 access to veterinarians. So, personalization, empathy, complementary services. That’s great. And you know, it’s not just about price. Fast forward 2017, Chewy’s market share in online pet supplies goes from 8 % to 26%.

17:52

Basically, Amazon’s price war fails. Chewy eventually gets acquired by PetSmart for $3.35 billion. So, like, both are both good stories in competitive strength and defensibility in digital businesses. And you can see there’s a lot going on. You can win big if you’re clever and you know what you’re doing. You can get taken down pretty fast. The marketplace can be uh brutal.

18:20

And that’s really point number one here, is, yeah, digital competition is brutal, but it’s totally winnable. In fact, you can win bigger than ever before. If you do it right, you can win faster and bigger than businesses ever have been able to. But you can also lose pretty quick, even if you do nothing wrong. You can be a very good average performing business and the world’s changing too fast. So average companies…

18:47

getting in trouble pretty frequently, not necessarily because they did anything wrong. It’s just average is more difficult than it used to be. So that’s kind of point number one. Now, why? Like what’s going on? I’ll give you my diagnosis of what’s going on and then I’ll give you my solution. You’ll see that my strategy sort of falls out of the diagnosis. What’s my diagnosis? My assessment is, look, being average as a business is now high risk.

19:15

You do not want to be just average in the middle anymore. It used to be for hundreds of years, you could be an okay average business, not terrible, but not rock star. And you could survive for decades, retailers, department stores in Midwestern cities, gas stations, being average is now a risky place to be, unfortunately. Why? Well, because technology and especially software.

19:41

is just changing things at an increasing rate. Everything’s moving faster. Products and services are emerging faster than ever before, and they’re becoming obsolete and fading. It used to be you had a good product like ketchup or something. You could live for decades on that. Not anymore. Things become obsolete much faster. Everyone thinks it’s about being disrupted. This tech is going to… Most of the time it’s just obsolescence.

20:09

You had a good product, now a better one’s coming along and you you’re just kind of obsolete. So, products and services, then you say competitors are emerging, rising and falling than ever before. There’s a lot more competitors than there used to be. Used to be if you were in television, there were three stations, right? CBS, ABC, NBC. Now there’s millions of people on YouTube. Like just the pure scale of your competitors has gone through the roof and the sort of intensity has gone way up. And then

20:38

On the other hand, kind of have look markets, customers, behaviors, they’re changing as well. Now customers don’t tend to change as fast actually. They do in China and they do in Asia, but in most of the world, like, you know, my parents still watch Fox News every day on the TV and they’ve been doing this their whole lives. I can’t even think of the last time I haven’t had a cable package ever in my whole life. Like, but

21:05

people get set in their ways. Okay, customer behavior can change slowly in some areas, but fast in others. Okay, so speed, competitive ferocity of business, just increasing. That’s just the way of the world. It’s the way it’s going to be. Now, it’s actually worse than that because not only is the pace of business accelerating, the distribution of winners and losers is becoming

21:34

much more extreme. This is the average problem. Being average, the profits are going to sort of a smaller and smaller group of companies. So yeah, you can win. There are winners and then there are losers and the distribution is a lot more severe than it used to be. So, one of the studies I always point to, which I actually really like, is a McKinsey and Company study from like 2000.

22:02

10 to 2015. They keep doing this study, so it’s pretty good. And they just looked at economic profits, which are operating profits after capital costs. And they just look at them industry by industry and say, it’s a smaller and smaller number of companies that are getting the profits. So, they call it a power curve of economic profits. And yeah, the majority, the middle, don’t make much economic profit. The top quartile,

22:30

The top performers, yeah, they make a ton of money. And the bottom quartile, they fall much faster. So, the middle ground, one, it’s harder to survive there. There’s more competition. And two, the profits aren’t really there anymore. You know, the distribution of winning and losing is much harsher than it used to be. So, everyone likes to talk about sort of famous companies that got disrupted, Nokia, Kodak.

22:59

Blackberry, Barnes & Noble, Blockbuster, we always share these stories. Those aren’t really the ones to think about. The ones to think about are average medium-sized companies that are just doing fine. They’re average performing companies. They’re not doing anything wrong and they’re not falling dramatically like in those cases. They just slowly sort of decline over time and they just slowly sort of disappear. The gap, remember the retailer, The Gap?

23:29

They were a big deal in 2000, 2005. They were kind of a major in it. Nobody even hears about them anymore. They slow and you can look at their numbers. They’ve shrunk pretty good. yeah, that’s kind of my diagnosis is a look being average. And on average, I’m talking about competitive strength and defensibility is much less safe than it used to be. So, you have got to try to move up in your operating performance to the top level.

23:56

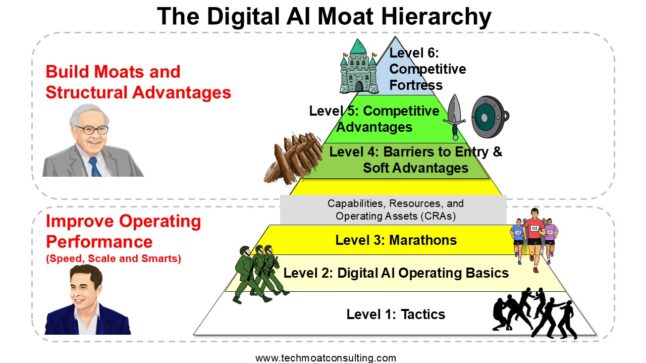

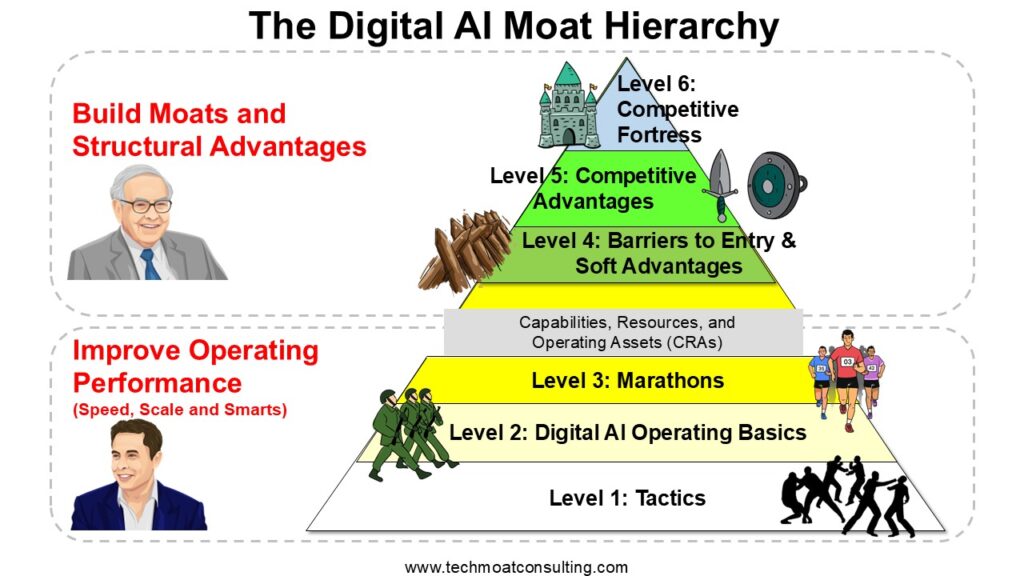

That’s offense and you have got to play defense. You have got to be building your moats and competitive defenses to prevent yourself from sliding down into the bottom quartile. So, you want to play offense and defense. Fierce operator trying to climb your way up, build your moat and your defenses so you don’t slip down. That’s basically my diagnosis for how to manage a business in the digital age and now the generative AI agent age. Okay, that’s my diagnosis. What’s my solution?

24:26

What should you do? As I kind of said, all right, you’ve got to become a fierce operator, a fierce digital operator. That’s Elon Musk land. And you got to become a good mope builder. That’s Warren Buffett land. You have got to do both. And I’m not just dodging the question by saying, oh, instead of A or B, let’s just do A or B. No, I think when you look case by case, which is what I’ve been doing for a decade.

24:51

That’s what you see. You see companies with good moats that are weak at operations get taken down. You see very good operators without moats can also fail. You have got to have both. You have got to have the horse and the jockey, basically. That’s basically how do you do that? How do you build your competitive strength? That’s the hierarchy. That’s kind of my core framework, which I’ll put in the show notes. That’s the digital AI mote.

25:20

hierarchy and it’s a hierarchy. There’s six levels. You have got to play on all the levels, but you really want to move up the hierarchy as much as possible because that’s where the real strength is. And when you assess a company, if you’re an investor and you see that everything you’re doing is on level one or number two, you should hit the panic button because you have got to move up. That is not a good place to be. So, I think in the bottom way, I sort of break this out is the bottom three levels.

25:49

They’re all about operating performance. That’s Elon Musk land. The three levels I map out, tactics, the digital operating basics, which are now called the digital AI operating basics, and then marathons. That’s level one, level two, level three going up. That’s Elon Musk land. What are we looking for? We are looking for speed, scale, and smarts. Those are the KPIs. When we’re looking at operating performance of a business, speed, how fast can it adapt?

26:19

How fast can it innovate? That’s the speed question. Scale, how fast is it growing? You can be sort of, growth is funny. Growth solves almost all problems. Now the problem is growth doesn’t go on forever. But if you’re weak competitively, if your management isn’t that good, if you’re growing, everything in life gets better. I like the phrase that growth is like oxygen for a business.

26:47

It makes it easier to hire people. You get better people. You have extra money to spend. You’re not having to cut costs so much. I growth just plays out across the board. So being fast and growing, those are just default high priority KPIs for operating performance. That’s like literally every business I talk to. Number one thing, how fast are you? I need to see how fast you are.

27:15

Show me how many decisions you make a week. Show me how many experiments you do. How often do you launch products? And you measure it and you improve it. Speed makes everything better. Growth is another thing that makes everything better. Growth is like oxygen. The speed analogy I use is, I don’t know who said this, someone said it and I’ve copied it. Speed is like playing chess. If you get to move twice every time your opponent moves once, you’re going to win every chess match you play.

27:42

So, speed, scale, and smarts, we’ll talk about smarts later. That’s operating performance, three levels. You want to be just a fierce digital operator. Top three levels, that’s Warren Buffett land, that’s Moats structural advantages. This is not about people and operations and getting your team to move faster and quicker and getting everyone, know, it’s not about people and processes. This is about structures.

28:09

This is about we have a tremendous barrier to entry and nobody can get into our business without spending $5 billion upfront. That’s a structural advantage. We have a tremendous cost advantages as a purchaser, like Walmart. The vast majority of companies can’t match the cost of goods sold. That’s a structural advantage. So, the first three levels, Elon Musk land, that’s about people, operations, operating systems, marathons.

28:37

The top three levels, that’s about barriers to entry, competitive advantages. I always talk about the bottom levels like people fighting in the street. The top levels are like having a castle. You’re competing with both of those analogies. The bottom one is like we’re competing in a street fight. We got to be good at punching and kicking. That’s tactics. The other one is like, look, we want a castle. That’s a structural advantage. You want both. So.

29:04

I’ll break those down and I’ve talked about those a lot, but yeah, so, okay. You need to be a fierce digital operator and you need to be good at building digital moats. Now, moats are kind of a, moats aren’t really digital. Oftentimes when we’re talking about moats in a business, they’re a mix of physical and intangible assets. I’ll go into that in Ridiculous Deal. That’s like 70 % of my books is taking apart the moat question.

29:32

in digital businesses. The other stuff I’m going to talk about, other people have talked about that a lot. That’s kind of my own core thing. But yeah, so you’re going to basically have to learn to channel Elon Musk and you’re to have to learn to channel Warren Buffett. And that’s going to be traditional businesses. It’s going to be traditional businesses going digital or incorporating generative AI in AI. And it’s going to be digital natives who are always sort of born digital.

30:01

and you’ll Google in these. It’s kind of those three groups and you can play all of that. And the answers aren’t as obvious as you think. Starbucks is doing good. All this generative AI stuff, all this digital stuff, all these network effects that everyone talks about, they don’t have to worry about any of that. Neither does Coca-Cola. They’re doing great. Google, which arguably had the most powerful moat ever seen in a business,

30:29

90 % of global search, nobody’s ever had that, ever. It’s arguably the most valuable moat ever built. It was unbelievable, impregnable and impregnable. I’m saying that wrong. And then generative AI comes on. Now they didn’t take down the moat, know, chat GBT, but it did create a very good substitute. Search is still there and

30:58

You know, Google still dominates search, but we have a substitute. So, when we think about competitive defenses and strength, we’re really talking about three to four different groups. Defending against who? Well, your rivals. Okay, fine. There’s people in your business. There are new entrants, people who can jump in your business. Maybe they’re in a complimentary service. Maybe they’re going to vertically integrate into you. But we also want to think about substitutes.

31:26

One of the reasons DD has difficulty with profitability, so does Grab, is because yeah, you dominate in ride sharing, but there’s a substitute which we call buses and subways. And it’s a low-cost substitute. If you have a low-cost substitute, that’s really going to hurt your business, even though you’re dominating in your business. So, you want to think about competitive strength and defensibility against rivals, new entrants, and among those, they can be small or they can be dominant.

31:57

Maybe you’re the startup and your rival is much bigger than you. And then you have got to think about substitutes as well, because that can really shape the economics of what you’re doing, even though you’re dominating. know, there was a company when automobiles were invented, there was still a company that was probably the dominant carriage builder that you put behind horses and they probably had a very good competitive moat and they didn’t do anything wrong.

32:24

They just kind of got replaced by a, in this case it was a direct disruption, but it could just be a substitute that’s near enough that people can choose it. Anyways, that’s the end of chapter one. And I’ll put the graphic, the moat hierarchy, which is kind of the key framework, really at the center of all these books. I’ll put that in there. And then the next one I’ll do chapter two. I’m not sure when I’ll do that. Probably not right away. That one we’ll talk about the CEO playbook and the investor checklist. So, we’ll…

32:53

take it from theory which I’ve laid out to be something much more directly usable. Anyways, that’s what it is. I hope that is helpful. As for me, it’s pretty spectacular but things are going really well. I’m having a good time um at the beach. I’m heading out to China to go visit iQiyi Land, their new theme park, which is exciting. The date keeps getting moved.

33:18

I’m going to meet with Tencent Cloud in a couple months. We’re doing something in Jakarta. That’s awesome. I mean, I just have a great time. I love flying around, you know, meeting with these companies. It was Spain a couple months ago or weeks ago. So, yeah, things are going really well. What else? Watching a lot of Netflix, which really funny is my girlfriend is not from Asia, but she has become like the biggest super fan of Chinese and Korean dramas.

33:49

So of course I have to watch them then, right? Because that’s what’s on the TV. And man, we are watching Chinese and Korean dramas like crazy. And I have got to admit, they’re great. We’re watching one on Netflix right now called Pursuit of Jade. And these are all sort of a bit romantic. They’re not made for me, for guys generally, and not for me at all. And it’s these old period dramas where everyone’s got the outfits and the scenes.

34:19

The sets are amazing. there’s a lead character named Zhang Linghe, who some Chinese actor who apparently is like the prettiest man ever born in China. He’s six foot four. Like people stop, like women stop talking when this guy comes on the screen. I don’t know what this guy has but look up Linghe Zhang. You tell me, but I do notice that he seems to dazzle.

34:47

the opposite sex. I don’t know what that’s about. Anyways, we’re watching those which are great. Anyways, I looked up where they’re filming this because I like the movie and TV industry as a subject. I think it’s interesting. I don’t really think it’s a good place to invest. uh Business is pretty hard, but… And there’s the, you know, these massive movie sets outside of Shanghai, which I’ve never visited, but I’m definitely going to go where they film this show. HengDian, HengDian World Studios.

35:15

It’s basically like the world’s largest movie TV studio. And it’s like 7,000 acres where they’ve recreated the Forbidden City and they film all these shows. are a lot of them. Pursuit of Jade, they film it there and it’s stunning. Like I’m definitely going to visit next time in Shanghai. I’m going to go out and take a tour and look around. I’ve actually got a couple of these. I got ICHI land. I’m going to go to Hongdae and check out the massive movie studio. And then I want to go to Pop Mart.

35:45

I was chatting with Pop Mart the other day. I want to go visit Pop Mart, their theme park in sort of Chaoyang of Beijing. So, I’m going to go do a tour with them, I think. So awesome. like this. I like the side of the consumer experience where you get interesting psychology, like entertainment. So, Pop Mart’s interesting in many ways. iQiyi is interesting movies. So, I kind of like it in that regard. Plus, it’s a lot of fun.

36:13

So anyways, yeah, that’s kind of my thing, but take a look at them. They’re pretty amazing. With the Pursuit of Jade, take a look at it and just, even if you don’t like the story, because it’s not really a story I like, just the sets and the appearance is pretty impressive. Anyways, that’s a quasi-recommendation. I’m not sure if it’s a full recommendation. Anyways, that’s it for me. I hope that’s helpful. And for those of you who are subscribers, I’m going to be hitting you with a lot of content because I got a decent amount to make up.

36:43

So yeah, there’s going to be a lot of that on the way. That’s it for me. Hope everyone is doing well. Talk to you next week. Bye bye.

——–

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

Note: This content (articles, podcasts, website info) is not investment advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. Investing is risky. Do your own research.