Everyone talks about marketplaces, but I like audience-builder platforms. They have lots of interesting quirks.

- Some can be very powerful (i.e., YouTube, TikTok, Instagram). Others are kind of messy and strange (BiliBili with bullet chat). Others aren’t really platforms at all (Spotify for music).

- They tend to bleed into social networks and communications services. Yes, YouTube is a big video library connecting content creators with viewers. But the Twitter and Facebook newsfeeds mix communication networks with platforms for content creators.

- Advertisers play an interesting role as an additional user group. Also, influencers.

- Viewers can play different roles. They can be viewers. Or active in discussions. Or amateur content creator. Or active sharers on social media. These platforms can be highly effective at activating consumer networks through content and community.

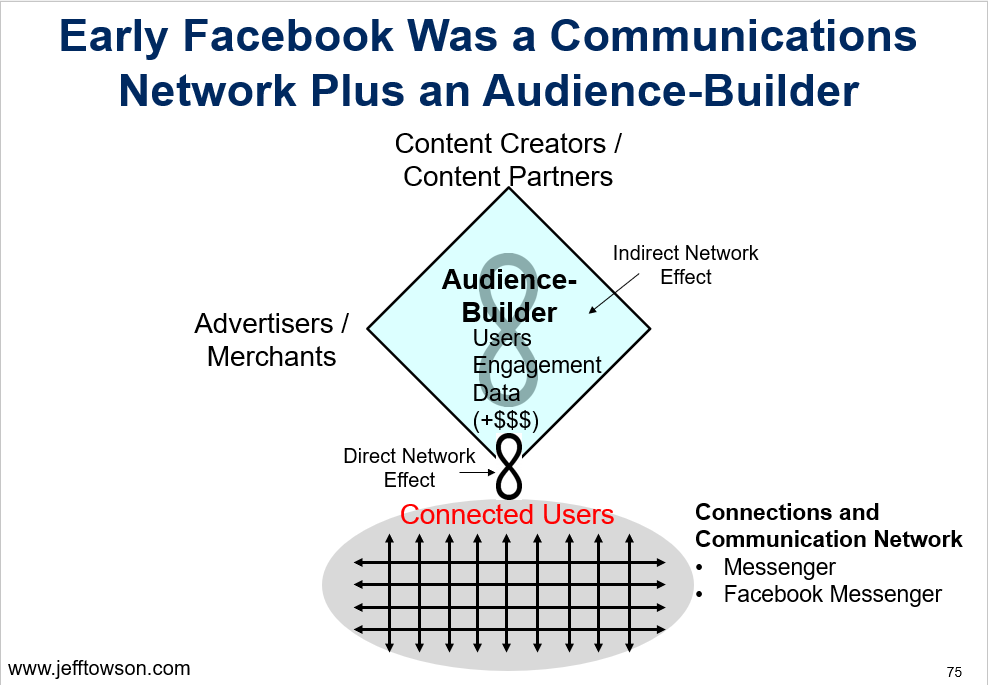

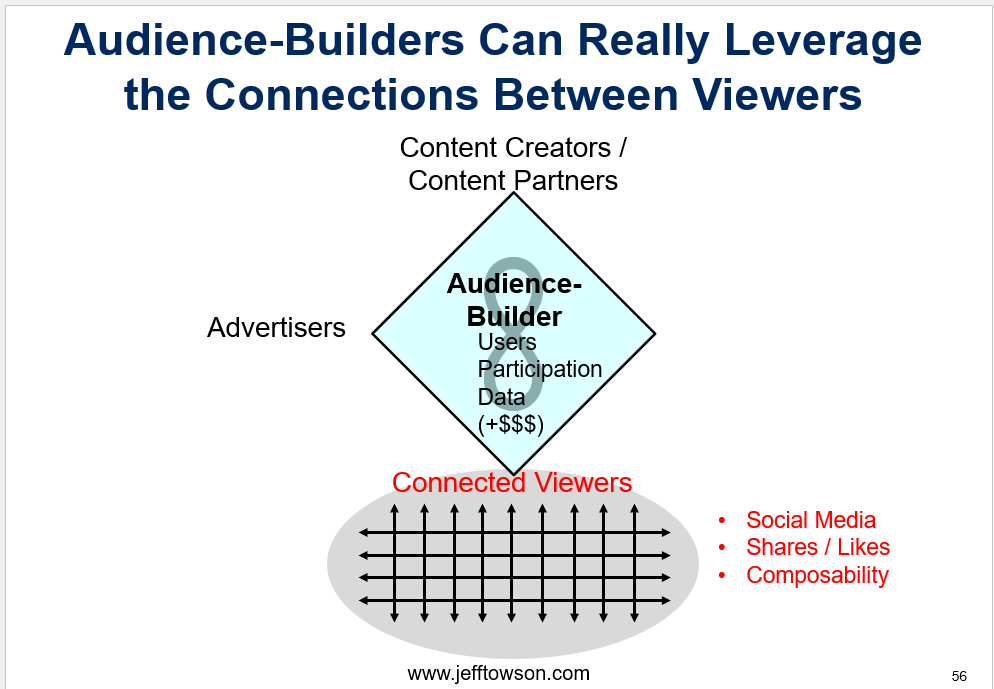

Here’s a simple image for it:

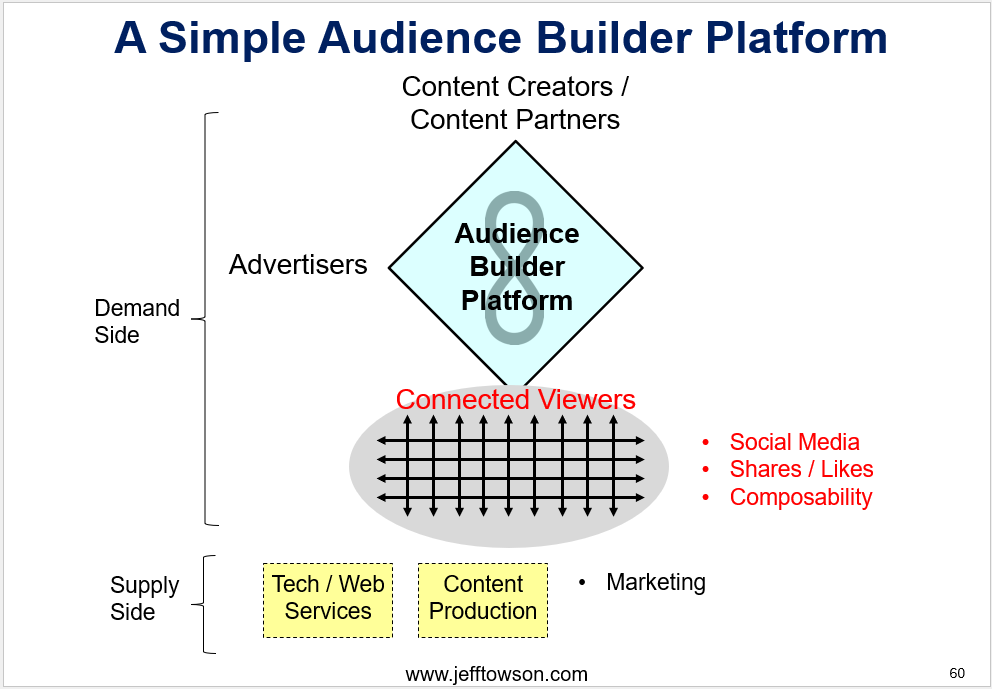

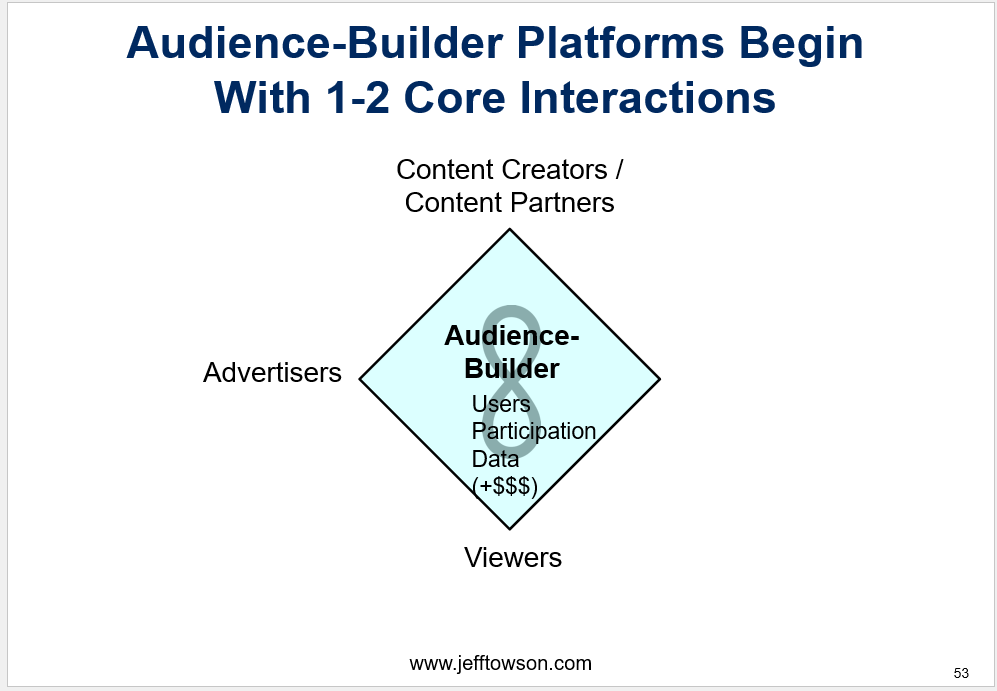

Here’s my standard explanation for audience builders.

I’ve gone through this many times (see the Concept Library). So here I thought I would just list 5 common misunderstandings about audience builder platforms.

Misconception 1: Audience Builder Platforms Are Just Content Hubs with Libraries

Audience builder platforms are not just digital spaces where creators upload content and viewers consume it. That’s certainly where it starts. Connecting content creators with viewers is the core interaction. As shown.

But these platforms are far more complex and varied than simple content hubs. And even more than other platform types like marketplaces or payment platforms.

Audience builders are about enabling lots of interactions around audience building.

That means serving multiple user groups, including:

- Viewers (often referred to as connected viewers because they like to share and comment)

- Content creators

- Influencers

- Advertisers

- Merchants and brands

Balancing the services and interests of these different user groups can be complicated. Plus, the users and their interactions evolve over time, requiring the platforms to adapt. These platforms are much more fluid and human than product marketplaces.

The nature of the content can increase complexity.

Content can range from professionally generated content (PGC) created by media companies to simple user generated content (UGC) like photos and short videos made with smartphones. And in between we can find high quality user generated content (hUGC) which can approaches professional levels.

Platforms like iQiyi, Youku Tudou, and Tencent Video in China are particularly complex in their content type. They combine elements of Netflix (licensed/in-house professional content) with YouTube (user-generated content). This mix of content types, along with the necessary capabilities like marketing spend, content moderation and web services makes them pretty complicated operations. Some can be highly profitable (Instagram, TikTok) while others can struggle with significant ongoing costs (Rumble, YouTube).

The format of the content can change the nature of the interactions.

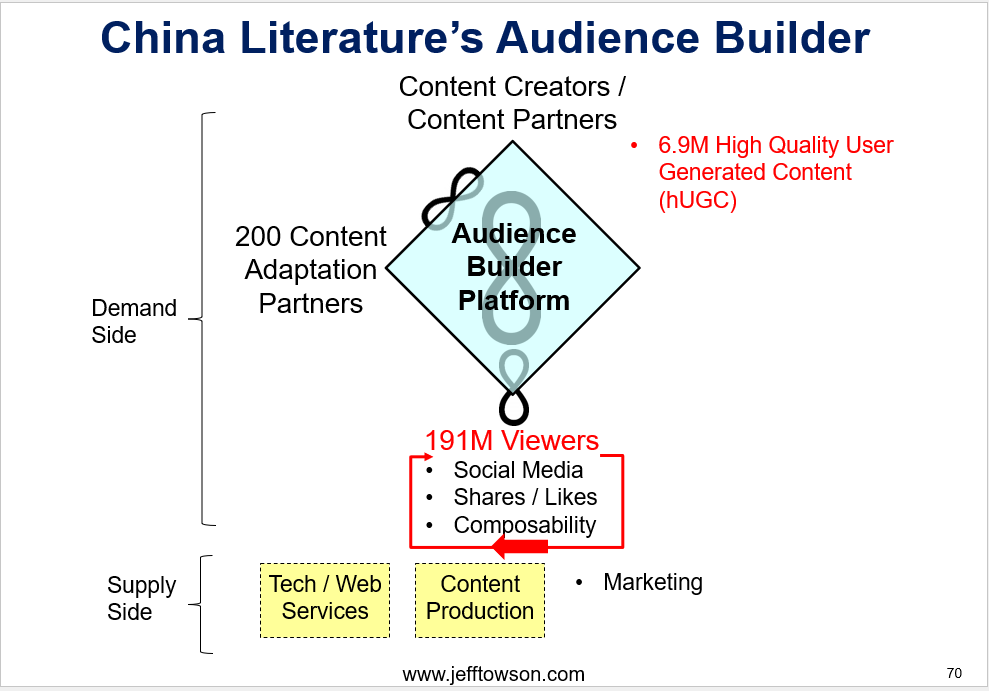

Spotify (music), TikTok (short video), and China Literature (literature) are all audience builders that connect creators with viewers, but they are wildly different. And they can create different types of interactions.

For example, China Literature connects professional and amateur writers with readers, using a freemium model. They also monetize by leveraging IP. But the author to reader interactions are central to the platform. There is a personal relationship between readers and their favorite author. And their favorite characters. That is completely different from the short-form video focus of TikTok or the music focus of Spotify. Neither of which have lots of creator/viewer interactions.

Therefore, seeing these platforms as simple content hubs and libraries misses the complexities of their business models and the specific interactions they can have.

Misconception 2: Audience Builder Platforms Are Highly Profitable

You would really think this would be true.

These platforms can be very powerful in terms of user attention. It’s easy to assume they are financial goldmines. However, while the platform business model itself can often be powerful with consumers and dominant with rivals, the economics are often problematic.

Some audience builder platforms are famous for how much money they lose. This is particularly true for platforms that rely heavily on purchasing or producing expensive professional generated content (PGC). Think about the economics of:

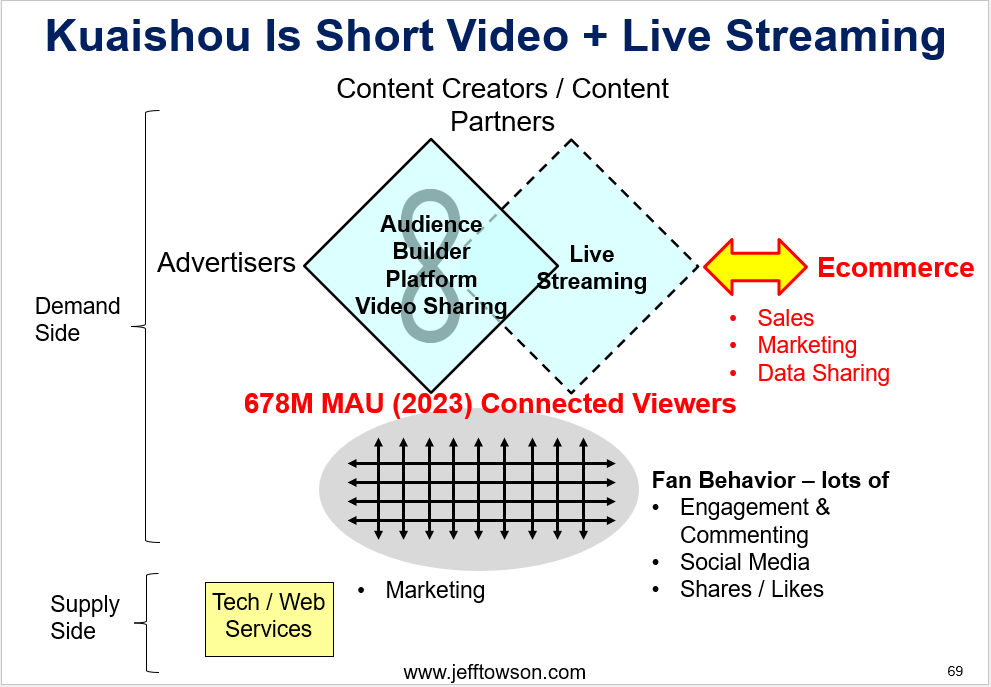

- Live streaming. Influencers are expensive. The gross margins for live streaming are much lower than short video. Businesses like Kuaishou pair live streaming (good for attention but low profits) with short video.

- Music streaming. Where a few studios control most of the popular music rights. And nobody likes to listen to amateur music.

- Gaming sites. Here you can be very dependent on a few blockbuster games, which are usually controlled by smart companies.

In China, video streaming platforms iQiyi, Youku Tudou, and Tencent Video have long been engaged in a costly content spending war. They each attempt to differentiate themselves (and justify their subscription services) by having unique tv shows and movies. This is expensive and these platforms have struggled to get to profitability.

Content moderation / curation costs can be a big problem.

Audience builder platforms benefit from scale (more videos, more viewers). That’s their strength. But content moderation (removing profane or unwanted content) does not scale. That’s their weakness.

Content moderation usually takes humans and can require armies of people. In China (where content moderation can be very political), this can be a major cost. ByteDance’s first big hit was Toutiao, a news audience builder. But they ended up having to hire an army of content moderators to police the content.

That said, there are definitely cash machines in this space.

Instagram and TikTok are huge cash generators. Although both are now flooding money into generative AI due to its disruptive threat to content sites. It turns out staying on the constantly changing frontier of content creation and consumption requires substantial resources and investment, which can also impact profitability.

Misconception 3: Audience Builder Platforms Get You “Winner Take All” Dynamics

Another common assumption is that audience builder platforms, like other platforms with network effects, inevitably lead to “winner take all” scenarios where one dominant player captures most of the market.

That can certainly happen. Think YouTube.

But short video has proven to be quite easy to break into. TikTok is still the biggest player. But not like they were 5 years ago. There are lots of other short video services growing rapidly. Think YouTube Shorts, Instagram Reels, WeChat Channels, and Kuaishou.

In commodity services like making phone calls and sending texts, there is little room for differentiation. This makes it difficult for smaller players to compete against a large established network. This often results in one dominant player based on network effects. Social networks and communications tend to consolidate in this way.

However, audience builder platforms usually have some room to differentiate. We see interesting variations all over the place. Think TikTok vs. YouTube vs. XiaoHongShu vs. Bilibili vs. WeChat channels and so on.

Differentiation can occur in several ways.

- Platforms can focus on different user groups. While platforms like Threads and Twitter might have similar user groups in theory (consumers, content creators, advertisers), the mix and behavior of these groups can vary. Threads was founded as a political alternative to Twitter. And it is doing better and better.

- Content moderation and the algorithms can curate and personalize content to be inherently differentiated. The way an algorithm selects and presents content is akin to the decisions of an editor-in-chief of a newspaper. Different editors get you different user experiences. And since nobody has yet solved the content curation at scale problem, different platforms will inevitably have different approaches, creating differentiation.

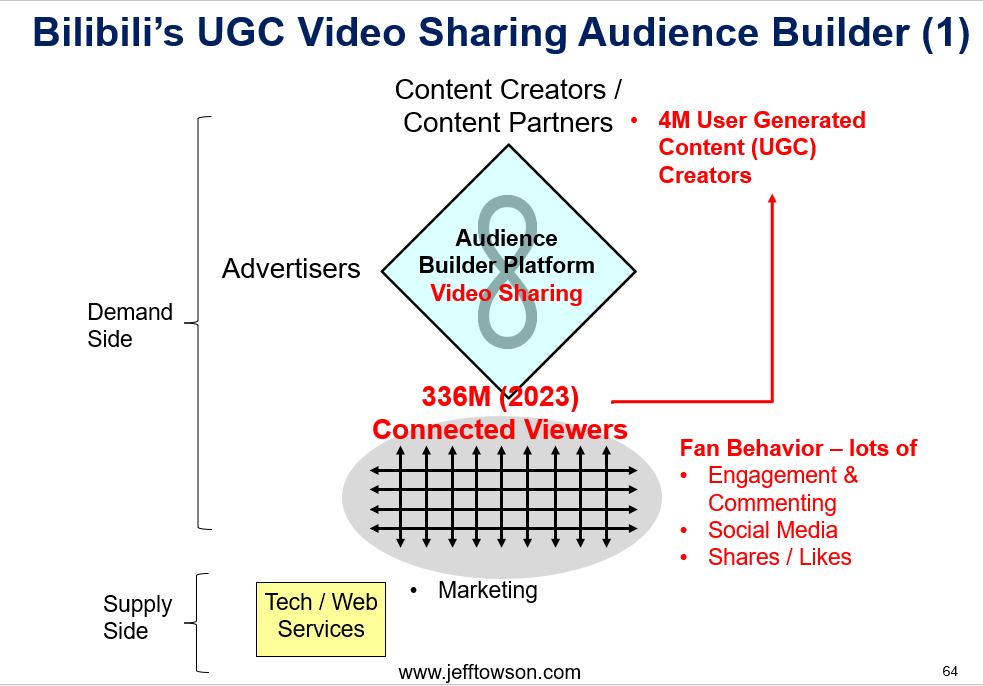

I’ve written quite a bit about specialty audience builders like Kuaishou and Bilibili. Bilibili has historically focused on ACG (Anime, Comics, Gaming) and the more enthusiastic fan behavior we see in this area.. it did quite well as a specialized audience builder against the video giants like TikTok. However, they are now pivoting to focus on GenZ+ with all types of content.

Misconception 4: Audience Builders Have Two Main User Groups – Creators and Viewers

A fourth misconception is that audience builder platforms are like marketplaces connecting content creators with viewers. That’s not exactly correct.

The difference between creator and viewer is fluid and often blurred. I don’t really think of them as user groups. I think of them as separate roles (creation vs. consumption) that can be done by the same people. Sort of like express delivery. The same person can be a sender or receiver of a package.

The strongest audience builder platforms are built upon user-generated content. That gets you the most long tail content (and is the cheapest content). For articles, short videos, and photos, it is pretty easy for viewers to transition to creators. Platforms like TikTok and Instagram are built on this type of transition. Viewers becoming content creators is a big source of their growth.

This blurring of roles also enables you to tap into “composability, something seen on platforms like TikTok and YouTube. This is when people making videos encourage others to create their own versions or reaction videos. TikTok is always getting people to do their own version of a trending dance. Composability is powerful for creating trends. And getting engagement. And it is based on encouraging the transition from viewer to creator.

Finally, user generated content and influencer generated content are pretty much the best tools for activating consumer networks. You want to get everyday users (viewers) participating in content creation. And you really want them sharing it with their connections on social media.

Misconception 5: A Content Library Is a Barrier to Entry

Final point.

There are at least two big moats in audience builders.

- The first is a network effect (two sided), which protects you against rivals.

- The second is the library as a barrier to entry, which protects you against new entrants. Sometimes.

YouTube definitely has a big barrier to entry. Its digital content library (now going back decades) is impossible to replicate. So new entrants have to come up with a differentiated play like focusing on anime and gaming.

However, TikTok’s library doesn’t really create a huge barrier. People just don’t want to watch short videos from 5 years ago. The utility and value of short videos degrades pretty quickly. It’s a much easier space to jump into. It is one of the reasons we have seen so many businesses successfully jump into short video recently.

This creates an interesting strategy question.

- Are you mostly in the business of building a large digital content library that retains value? Like YouTube. If so, you want to think about personalizing your long tail of content. Like YouTube.

- Or are you mostly in the business of enabling interactions between user groups? Because the content degrades in value very quickly? If so, it’s more about getting user interactions and engagement. Think about switching costs. And maybe reaction videos (like TikTok).

I like when the value for viewers is beyond just having a big content library. I like when it is about interacting directly with their favorite creators or with other viewers. This community aspect and the ability to engage socially with content and other users is powerful.

It’s important to remember that the value of an audience builder to viewers can be a combination of:

- The content.

- The interactions it enables.

- The community it fosters.

- The personalization it provides in all three of these.

That’s a lot more than just a passive library.

***

Ok. That’s it. Thanks for reading.

Jeff

—-—–

Related articles:

- Lessons from My Visit to Alibaba Cloud (Tech Strategy – Podcast 244)

- AutoGPT: The Rise of Digital Agents and Non-Human Platforms & Business Models (Tech Strategy – Podcast 163)

- Why ChatGPT and Generative AI Are a Mortal Threat to Disney, Netflix and Most Hollywood Studios (Tech Strategy – Podcast 150)

From the Concept Library, concepts for this article are:

- Audience Builder

From the Company Library, companies for this article are:

- n/a

———

I am a consultant and keynote speaker on how to increase digital growth and strengthen digital AI moats.

I am the founder of TechMoat Consulting, a consulting firm specialized in how to increase digital growth and strengthen digital AI moats. Get in touch here.

I write about digital growth and digital AI strategy. With 3 best selling books and +2.9M followers on LinkedIn. You can read my writing at the free email below.

Or read my Moats and Marathons book series, a framework for building and measuring competitive advantages in digital businesses.

This content (articles, podcasts, website info) is not investment, legal or tax advice. The information and opinions from me and any guests may be incorrect. The numbers and information may be wrong. The views expressed may no longer be relevant or accurate. This is not investment advice. Investing is risky. Do your own research.